4A Maryland PDF Template

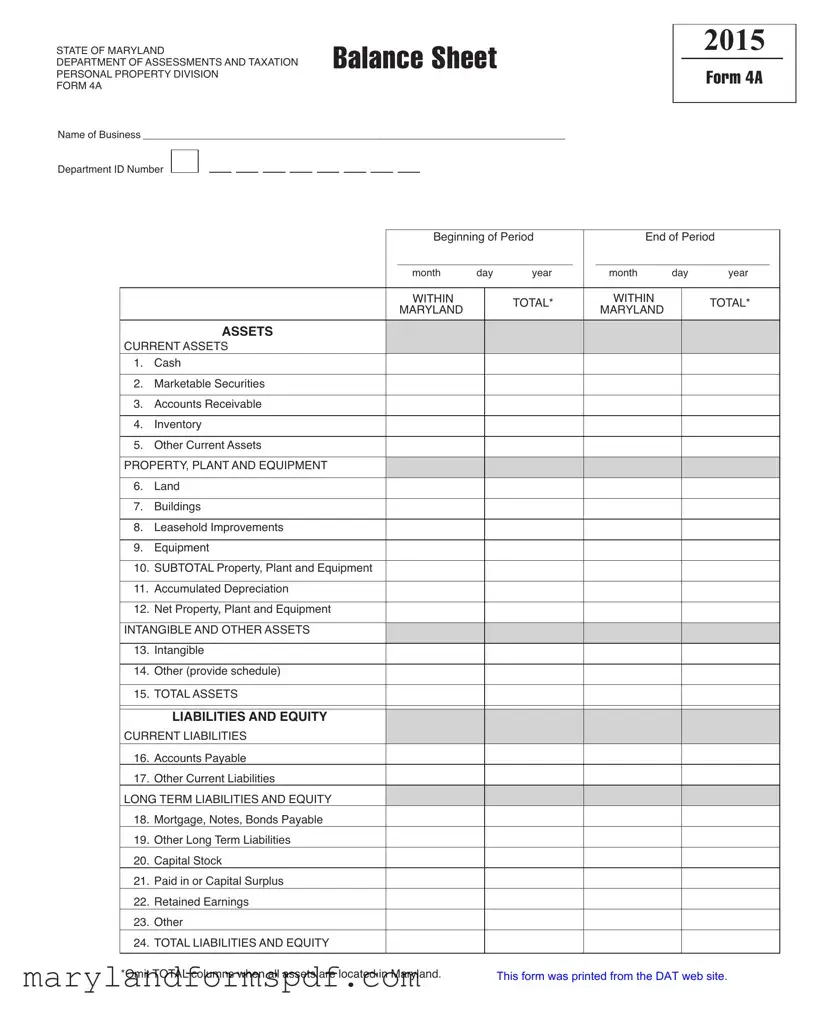

The State of Maryland's Department of Assessments and Taxation Personal Property Division requires businesses to submit the Form 4A, a comprehensive balance sheet for the year 2015. This crucial document captures a detailed snapshot of a business's financial health by listing assets, liabilities, and equity within a specified reporting period. The form demands precision in reporting current assets such as cash, marketable securities, accounts receivable, inventory, and other short-term assets critical for day-to-day operations. Moreover, it requires an exhaustive account of long-term investments including property, plant, and equipment, alongside accumulated depreciation to ascertain net property value. Additionally, Form 4A explores intangible assets and other miscellaneous assets that contribute to the total asset value. On the flip side of the balance sheet, the form delineates between short-term obligations—accounts payable and other current liabilities—and more entrenched financial commitments like mortgages, notes, bonds payable, and other long-term liabilities. Equity, captured through capital stock, paid-in or capital surplus, retained earnings, and other equity items, offers insights into the financial resilience and funding structure of a business. Designed to provide a holistic view of a business's financial standing, Form 4A plays a pivotal role in the regulatory and tax assessment framework, ensuring businesses are evaluated fairly and accurately within Maryland.

4A Maryland Sample

STATE OF MARYLAND |

BALANCE SHEET |

2015 |

|

|

|

|

|

||

DEPARTMENT OFASSESSMENTSAND TAXATION |

|

|

|

|

PERSONAL PROPERTY DIVISION |

|

|

FORM 4A |

|

FORM 4A |

|

|

|

|

|

|

|

|

|

Name of Business__________________________________________________________________________

Department ID Number

|

|

Beginning of Period |

|

|

End of Period |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

month |

day |

year |

|

|

month |

day |

year |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

WITHIN |

|

|

|

|

|

WITHIN |

|

|

|

|

|

|

|

TOTAL* |

|

|

|

TOTAL* |

|

|

|||

|

|

MARYLAND |

|

|

|

|

MARYLAND |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||

ASSETS

CURRENTASSETS

1.Cash

2.Marketable Securities

3.Accounts Receivable

4.Inventory

5.Other CurrentAssets

PROPERTY, PLANTAND EQUIPMENT

6.Land

7.Buildings

8.Leasehold Improvements

9.Equipment

10.SUBTOTAL Property, Plant and Equipment

11.Accumulated Depreciation

12.Net Property, Plant and Equipment

INTANGIBLEANDOTHERASSETS

13.Intangible

14.Other(provideschedule)

15.TOTALASSETS

LIABILITIESANDEQUITY

CURRENTLIABILITIES

16.AccountsPayable

17.OtherCurrentLiabilities

LONGTERMLIABILITIESANDEQUITY

18.Mortgage,Notes,BondsPayable

19.OtherLongTermLiabilities

20.CapitalStock

21.PaidinorCapitalSurplus

22.RetainedEarnings

23.Other

24.TOTALLIABILITIESANDEQUITY

*Omit TOTAL columns when all assets are located in Maryland.

This form was printed from the DAT web site.

File Breakdown

| Fact Name | Description |

|---|---|

| Form Title | STATE OF MARYLAND BALANCE SHEET |

| Form Number | 4A |

| Issuing Department | Department of Assessments and Taxation, Personal Property Division |

| Purpose | For businesses to report their balance sheet information, including assets, liabilities, and equity for the year 2015. |

| Components of Assets | Current assets, property, plant, and equipment, and intangible and other assets. |

| Components of Liabilities and Equity | Current liabilities, long-term liabilities and equity, which includes capital stock, paid-in or capital surplus, retained earnings, and others. |

| Governing Law | This form is governed by the laws of the State of Maryland and is regulated by the Maryland Department of Assessments and Taxation. |

| Special Instruction | Omit TOTAL columns when all assets are located within Maryland. |

Steps to Filling Out 4A Maryland

Filling out the Form 4A for the State of Maryland requires careful attention to detail and accuracy. This document, used by the Department of Assessments and Taxation, serves an important purpose in recording the balance sheet of a business for a specific fiscal year. To ensure completeness and correctness, follow these step-by-step instructions meticulously. Remember, the key to navigating this form is to provide precise information regarding your business's financial status as it respects both assets and liabilities.

- Start by writing the Name of the Business at the designated space at the top of the form.

- Enter the Department ID Number next to the name of the business.

- Fill in the Beginning of Period and End of Period dates for the fiscal year being reported, including month, day, and year for both.

- Under CURRENT ASSETS, input the values for:

- Cash

- Marketable Securities

- Accounts Receivable

- Inventory

- Other Current Assets

- For PROPERTY, PLANT, AND EQUIPMENT, detail the following:

- Land

- Buildings

- Leasehold Improvements

- Equipment

- Add these values to calculate the SUBTOTAL for Property, Plant, and Equipment

- Enter the amount for Accumulated Depreciation and subtract it from the Subtotal to find the Net Property, Plant, and Equipment.

- Under INTANGIBLE AND OTHER ASSETS, list:

- Intangible Assets

- Other Assets (provide schedule if necessary)

- Add up the totals for Current Assets, Net Property, Plant, and Equipment, and Intangible and Other Assets to find the TOTAL ASSETS.

- In the LIABILITIES AND EQUITY section, fill in the amounts for:

- Accounts Payable

- Other Current Liabilities

- Mortgage, Notes, Bonds Payable

- Other Long Term Liabilities

- Capital Stock

- Paid in or Capital Surplus

- Retained Earnings

- Other

- Sum the above to calculate the TOTAL LIABILITIES AND EQUITY.

- If all assets are located within Maryland, omit the TOTAL columns.

After completing the form, review all entries to ensure they accurately represent the financial position of your business. This detailed snapshot of your company's financial health not only fulfills a regulatory requirement but also provides valuable insights for decision-making. When satisfied with the accuracy of the information provided, submit the form to the Maryland Department of Assessments and Taxation as directed.

More About 4A Maryland

What is Form 4A in Maryland and who needs to file it?

Form 4A is a Balance Sheet required by the State of Maryland Department of Assessments and Taxation (DAT) Personal Property Division. It's designed for businesses to report their assets, liabilities, and equity as of a specific reporting period. Any business that owns, leases, or uses personal property in Maryland, or maintains a trader's license with a local unit of government in the state, is required to file this form.

What information is required on Form 4A?

The form requires detailed information about a business's finances, including:

- Current assets like cash, marketable securities, accounts receivable, inventory, and other current assets.

- Property, plant, and equipment details, including land, buildings, leasehold improvements, equipment, and accumulated depreciation.

- Intangible assets and other assets.

- A rundown of liabilities and equity, such as accounts payable, mortgages, notes, bonds payable, capital stock, and retained earnings.

When is Form 4A due?

Form 4A must be filed annually with the Maryland Department of Assessments and Taxation. The specific due date can vary, so businesses should check with the DAT or consult their legal advisor to ensure compliance with current filing deadlines.

Are there penalties for not filing Form 4A on time?

Yes, failing to file Form 4A by the due date can result in late fees, penalties, and interest. Additionally, businesses could face sanctions such as having their right to do business in Maryland revoked. It's critical to file on time to avoid these negative repercussions.

Can Form 4A be filed electronically?

Yes, the State of Maryland encourages businesses to file Form 4A electronically for faster processing and convenience. The DAT’s website provides resources and instructions on how to submit the form online.

How can a business get help with filling out Form 4A?

Businesses seeking assistance with Form 4A can reach out to the Department of Assessments and Taxation via their website or by phone. Additionally, consulting with a legal or tax professional familiar with Maryland's specific requirements is advisable for comprehensive assistance.

What happens if a business makes an error on Form 4A?

If a business discovers an error on their submitted Form 4A, they should promptly contact the Maryland Department of Assessments and Taxation to correct the mistake. Timely correction of errors can help prevent penalties or additional scrutiny from the state.

Are any businesses exempt from filing Form 4A in Maryland?

Some businesses may be exempt from filing Form 4A, such as certain non-profit organizations. However, exemptions are specific, and it's crucial for each business to verify their filing obligations directly with the Maryland Department of Assessments and Taxation or a legal advisor.

Common mistakes

Filling out the Form 4A for the State of Maryland, specifically for the Department of Assessments and Taxation Personal Property Division, requires attention to detail and understanding of accounting principles. However, mistakes can occur, leading to potentially significant errors in reporting. Here are four common mistakes people make when completing the Form 4A:

Inaccurate allocation between 'Within Maryland' and 'Total': Often, individuals mistakenly report assets, failing to accurately differentiate those located within Maryland from their total assets. This discrepancy is fundamental since the form mandates differentiated reporting for those assets located within the state versus all assets owned.

Errors in calculating depreciation: Another common error is the miscalculation of accumulated depreciation for Property, Plant, and Equipment. Accurate calculation is crucial because it affects the 'Net Property, Plant, and Equipment' figure, influencing the overall balance sheet's portrayal of asset value.

Omission of intangible assets: Intangible assets, such as patents, trademarks, and goodwill, are frequently overlooked or improperly valued. Despite their non-physical nature, these assets can significantly impact the 'TOTAL ASSETS' section of the form, thereby misrepresenting the company's financial position.

Misunderstandings related to current assets and liabilities: Often, there's confusion about what constitutes a current asset or liability, leading to inaccuracies in these sections. Current assets are those expected to be converted into cash within one year, and current liabilities are due within the same timeframe. Misclassifying assets or liabilities can result in a skewed financial overview.

To avoid these errors, individuals completing the Form 4A should:

Clearly understand the distinctions between 'Within Maryland' and 'Total' assets and report them accurately.

Use proper methods to calculate depreciation, reflecting the current value of physical assets accurately.

Ensure that intangible assets are properly identified and included in the form to capture the business's full value accurately.

Review the definitions of current assets and liabilities to ensure correct classification, providing an accurate snapshot of the business's liquidity and obligations.

By proactively addressing these common mistakes, individuals can provide a more accurate representation of the business's financial standings to the Maryland Department of Assessments and Taxation, ensuring compliance and contributing to a clearer economic picture of their operations within the state.

Documents used along the form

In the landscape of business documentation within the state of Maryland, the Form 4A, detailing a company's balance sheet for a given period, represents a crucial snapshot of financial health and asset management for both internal assessment and regulatory compliance. Alongside the Form 4A, several other documents frequently form part of the compliance and reporting framework, each serving a unique purpose in the business's financial and regulatory ecosystem.

- Form 1 - Personal Property Return: This form is essential for businesses operating in Maryland, as it provides a comprehensive declaration of personal property owned by the business, which is a requirement for tax assessment purposes.

- Form CRA - Combined Registration Application: Critical for new businesses, the CRA facilitates the registration with several state agencies, enabling the business to legally operate within Maryland.

Annnual Report: This submission is necessary for all entities doing business in Maryland. It reviews and updates the company's information on the public record, ensuring accuracies such as business address and principal officers.- Form BPT – Business Personal Property Tax Return: Similar to Form 1, but more detailed, it aids in determining the tax responsibilities of the business based on the value of its personal property.

Articles of Incorporation or Organization: Depending on the structure of the business (corporation or LLC), these documents legally establish the company in Maryland and outline its basic structure and operational scope.- Employer Identification Number (EIN) Confirmation Letter: Issued by the IRS, this document confirms the unique EIN assigned to the business, which is necessary for tax filing and employment purposes.

Trade Name Application: This document is vital for businesses operating under a name different from their legal entity name, registering the trade name with the state of Maryland.- Form 202 - Sales and Use Tax Return: Required for businesses engaged in the sale of goods and services, this form reports taxable sales and calculates the sales tax owed to the state.

Franchise Tax Report: Applicable to entities like corporations and LLCs, this report determines the franchise tax based on assets or income, contributing to the state's revenue from businesses operating within its jurisdiction.

The collective utilization of these documents, in conjunction with the Form 4A, enables businesses to not only comply with Maryland's regulatory requirements but also ensures a comprehensive approach to financial management and planning. While the Form 4A provides a snapshot of the company's financial standing at a point in time, the additional documents serve various functions from establishing legality, ensuring tax compliance, to facilitating detailed financial reporting. Together, they offer a multidimensional view of the business's operational, financial, and compliance status.

Similar forms

The 4A Maryland form is similar to other financial documentation required by various state and federal agencies. These documents serve for reporting the financial status, including assets, liabilities, and equity, of a business at a given point in time. Their purposes range from tax assessments to providing stakeholders with a clear picture of a business's financial health. Below are documents that share common ground with the Form 4A, highlighting what makes each document comparable and distinctive.

IRS Form 1120: The IRS Form 1120, U.S. Corporation Income Tax Return, is notably similar to the Maryland Form 4A in that both require detailed financial information regarding a business’s operations. Form 1120 focuses on the income, gains, losses, deductions, and credits of corporations, which aids in the calculation of their income tax liability. Similar to Form 4A, it includes sections on assets, liabilities, and equity, though it places a stronger emphasis on taxable income and tax computations. Both forms are integral for financial reporting and tax assessment at their respective levels – one at the state and the other at the federal level.

Uniform Commercial Code (UCC) Filings: Specifically, the UCC-1 Financing Statement, while not a direct financial statement, shares a connection with the Form 4A through the documentation of assets. The UCC-1 is used to declare a secured party's interest in the debtor's collateral, which may include items listed as assets on Form 4A like equipment or inventory. This form helps establish priority for the creditor in case of debtor default. The similarity lies in the emphasis on assets, but the purposes diverge significantly, with the UCC-1 focusing on securing interests and the Form 4A on assessing valuation for taxation.

Balance Sheet Statements: While not a specific form, balance sheet statements prepared for internal or external analysis closely resemble the Form 4A in content and purpose. A balance sheet showcases a company’s assets, liabilities, and shareholders’ equity at a specific point in time, much like the Form 4A. This similarity extends to the detailed breakdown of categories under assets, liabilities, and equity. However, traditional balance sheets are utilized more broadly for financial analysis, investment considerations, and internal management decisions rather than for specific state tax reporting purposes.

Dos and Don'ts

When completing the Form 4A for the State of Maryland, it's important to ensure accuracy and compliance with the Department of Assessments and Taxation. Below are some essential do's and don'ts to consider:

Do:

- Ensure all information is accurate and complete, reflecting the financial status of your business for the specified period.

- Double-check the Department ID Number to make sure it matches the number registered with the State of Maryland.

- Provide detailed listings for each category of current assets, property, plant, and equipment, as well as intangible and other assets.

- Correctly calculate depreciation for assets listed and properly report it under "Accumulated Depreciation."

- List all liabilities and equity accurately, including current liabilities and long-term liabilities and equity.

- If applicable, omit the TOTAL columns when all assets are located within Maryland, as per instructions.

- Review the form for any errors or omissions before submitting it.

- Utilize the schedule option for "Other" assets and liabilities to provide additional details as required.

- Maintain records of the submission, including a copy of the completed form and any correspondences with the Department of Assessments and Taxation.

- Submit the form by the deadline to avoid any late fees or penalties.

Don't:

- Overlook the "beginning of period" and "end of period" dates, ensuring they accurately reflect the financial year being reported.

- Forget to list both within and outside Maryland assets separately if your business holds assets in multiple locations.

- Misclassify assets or liabilities, as this can lead to inaccuracies in the balance sheet.

- Leave any field blank; enter "N/A" if a particular section does not apply to your business.

- Estimate values; use exact figures to ensure the integrity of the balance sheet.

- Ignore the need for additional schedules for certain assets or liabilities; these provide clarity and are required for proper assessment.

- Attempt to file an outdated form; always verify that you're using the latest version by checking the Department of Assessments and Taxation website.

- Underestimate the importance of the form's accuracy on your business's tax obligations and potential audits.

- Submit the form without reviewing it for completeness and accuracy.

- Disregard the instruction to omit TOTAL columns if your business assets are solely in Maryland, as this simplifies the filing process.

By following these guidelines, the process of filing Form 4A for your business will be more efficient and compliant with Maryland state regulations. Remember, this form plays a crucial role in the assessment and taxation of personal property for businesses operating within Maryland.

Misconceptions

When it comes to understanding and filling out the Form 4A for Maryland businesses, there are several misconceptions that can complicate the process. This form, required by the Department of Assessments and Taxation (DAT), plays a crucial role in the state's assessment of personal property and business assets. Here's a closer look at some of the common myths surrounding Form 4A and the realities behind them.

- Misconception #1: Form 4A is only for large businesses.

In reality, Form 4A must be completed by most businesses operating in Maryland, regardless of their size. This includes small and medium-sized enterprises, which are also subject to personal property assessments by the DAT. - Misconception #2: All sections of the form must be filled out by all businesses.

The truth is that not all sections of Form 4A apply to every business. For example, companies without physical property in Maryland may not need to detail assets within the state, but they must still submit the form with the applicable sections completed. - Misconception #3: Form 4A is an annual report on business profits.

Contrary to this belief, Form 4A focuses on a business's assets and liabilities, rather than its operational profits or losses. It's a balance sheet, not an income statement. - Misconception #4: Digital assets do not need to be reported on Form 4A.

Digital or intangible assets, such as intellectual property, should indeed be reported on Form 4A under the "Intangible Assets" section. This is a common oversight by businesses transitioning to digital models. - Misconception #5: The "Beginning" and "End" of the period dates are interchangeable.

The form requires specific dates for the beginning and end of the assessed period, which correspond to the fiscal year for most businesses. These dates are critical for accurate assessment and are not interchangeable. - Misconception #6: Only assets physically located in Maryland need to be reported.

While the form does have sections specifically for assets within Maryland, businesses are required to report all assets, regardless of location, to provide a comprehensive overview of their financial state. - Misconception #7: The "TOTAL columns" are mandatory for all businesses.

If a business's assets are all located in Maryland, the "TOTAL columns" can be omitted. This is a specific provision that simplifies filing for businesses operating entirely within the state.

Correctly understanding and filling out Form 4A is crucial for businesses to comply with Maryland's tax and assessment laws. Dispelling these misconceptions is the first step towards ensuring that businesses can accurately report their assets and liabilities, an essential aspect of operating in the state of Maryland.

Key takeaways

When preparing and utilizing the Form 4A for the State of Maryland, it is important to understand several key aspects that will ensure the accurate and efficient handling of this document. The Form 4A is a comprehensive tool used by the Maryland Department of Assessments and Taxation to analyze a business's balance sheet for the fiscal year.

The Name of Business and Department ID Number fields are critical for identification purposes. They must be filled accurately to match the business’s official records with the state.

Indicate the Beginning and End of the reporting period with specific months, days, and years, to define the accounting timeframe under review.

Under the Assets section, distinguish between assets located Within Maryland and those elsewhere to comply with state-specific valuation requirements. If all assets are located within Maryland, the TOTAL columns can be omitted, simplifying the reporting process.

The form categorizes assets into Current Assets, Property, Plant, and Equipment, and Intangible and Other Assets, requiring a detailed listing and valuation of each type.

For Liabilities and Equity, list all current and long-term financial obligations, including loans and equity details, to provide a comprehensive overview of the business’s financial health.

The final section compiles Total liabilities and equity, capturing the complete financial snapshot of the business for the assessed period.

Completing the Form 4A accurately is essential for businesses to ensure compliance with Maryland's Department of Assessments and Taxation requirements. It offers a structured format for presenting a business’s financial status, pivotal for both state assessments and the strategic planning of the business itself.

Common PDF Templates

Motion for Reconsideration Maryland - The Maryland DC CR 044 form warns that the issuance of a charging document leads to unavoidable legal processes, possibly culminating in a trial.

Maryland W-4 - Outlines specific exemptions available for charitable, religious, educational, and other organizations.