Fillable Loan Agreement Template for Maryland State

When individuals or entities in Maryland decide to lend or borrow money, the transaction's success and smoothness often hinge on the clarity and comprehensiveness of the documentation governing it. Here, the Maryland Loan Agreement form becomes an essential tool, serving as a detailed record of the terms agreed upon by the lender and the borrower. This form meticulously outlines the loan amount, interest rates, repayment schedule, collateral details (if any), and the parties' obligations and rights. It acts as a legally binding contract that underscores the seriousness of the financial commitment and the consequences of default. Moreover, the form offers protections to both parties, ensuring that the lender can recoup their investment under agreed terms and providing the borrower with a clear understanding of their repayment obligations. Its importance cannot be understressed, as it not only minimizes the potential for misunderstandings but also provides a solid legal foundation should disputes arise. Therefore, for anyone navigating the process of lending or borrowing money in Maryland, understanding the nuances of the Maryland Loan Agreement form is a crucial step toward a successful financial transaction.

Maryland Loan Agreement Sample

Maryland Loan Agreement Template

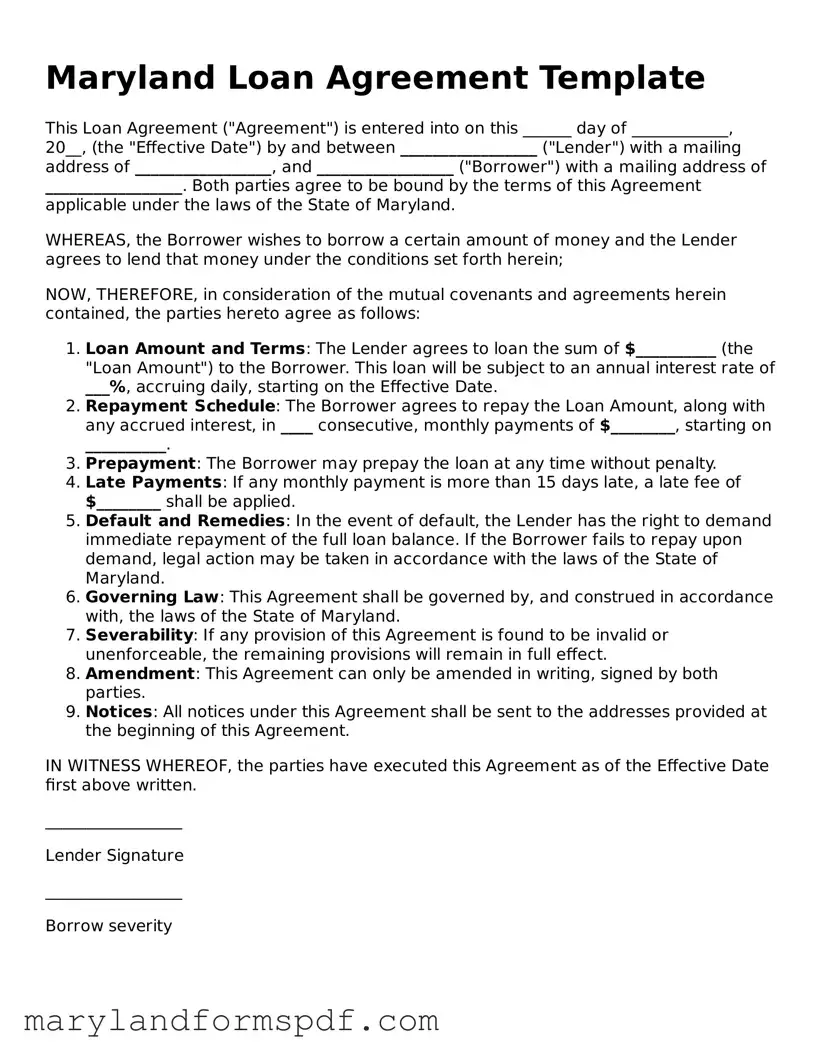

This Loan Agreement ("Agreement") is entered into on this ______ day of ____________, 20__, (the "Effective Date") by and between _________________ ("Lender") with a mailing address of _________________, and _________________ ("Borrower") with a mailing address of _________________. Both parties agree to be bound by the terms of this Agreement applicable under the laws of the State of Maryland.

WHEREAS, the Borrower wishes to borrow a certain amount of money and the Lender agrees to lend that money under the conditions set forth herein;

NOW, THEREFORE, in consideration of the mutual covenants and agreements herein contained, the parties hereto agree as follows:

- Loan Amount and Terms: The Lender agrees to loan the sum of $__________ (the "Loan Amount") to the Borrower. This loan will be subject to an annual interest rate of ___%, accruing daily, starting on the Effective Date.

- Repayment Schedule: The Borrower agrees to repay the Loan Amount, along with any accrued interest, in ____ consecutive, monthly payments of $________, starting on __________.

- Prepayment: The Borrower may prepay the loan at any time without penalty.

- Late Payments: If any monthly payment is more than 15 days late, a late fee of $________ shall be applied.

- Default and Remedies: In the event of default, the Lender has the right to demand immediate repayment of the full loan balance. If the Borrower fails to repay upon demand, legal action may be taken in accordance with the laws of the State of Maryland.

- Governing Law: This Agreement shall be governed by, and construed in accordance with, the laws of the State of Maryland.

- Severability: If any provision of this Agreement is found to be invalid or unenforceable, the remaining provisions will remain in full effect.

- Amendment: This Agreement can only be amended in writing, signed by both parties.

- Notices: All notices under this Agreement shall be sent to the addresses provided at the beginning of this Agreement.

IN WITNESS WHEREOF, the parties have executed this Agreement as of the Effective Date first above written.

_________________

Lender Signature

_________________

Borrow severity

File Properties

| Fact Number | Fact Detail |

|---|---|

| 1 | The Maryland Loan Agreement form is governed primarily by Maryland's Commercial Law. |

| 2 | It outlines the terms and conditions under which a loan is provided to a borrower in the state of Maryland. |

| 3 | The agreement details interest rates, repayment schedule, and the consequences of default, adhering to Maryland state laws. |

| 4 | Valid execution of the form may require notarization depending on the loan amount and involved parties. |

| 5 | Secured transactions within the loan may be subject to the Uniform Commercial Code as adopted by Maryland. |

| 6 | Changes or amendments to the loan agreement must be made in writing and signed by both parties, in compliance with Maryland legal standards. |

Steps to Filling Out Maryland Loan Agreement

Filling out a Maryland Loan Agreement form is an essential step in formalizing the terms between a lender and a borrower within the state. This document is crucial as it legally binds both parties to the agreed-upon conditions, ensuring clarity and protection throughout the duration of the loan. Ensuring accuracy and completeness when completing this form is vital to prevent any misunderstandings or legal issues in the future. Below is a step-by-step guide designed to help you fill out the Maryland Loan Agreement form accurately and efficiently.

- Gather all necessary information: Before you start, make sure you have all the required details, including the full names and addresses of the lender and borrower, the loan amount, interest rate, repayment schedule, and any collateral involved.

- Fill in the lender and borrower information: At the top of the form, specify the full legal names and addresses of both the lender and the borrower.

- Detail the loan amount and terms: Clearly state the total amount being lent, the interest rate applied, and the terms of repayment. This includes how the loan will be repaid (e.g., in installments, a lump sum) and over what period.

- Outline any collateral: If the loan is secured against collateral, describe the asset in detail, including any identification numbers or documentation that can verify ownership and value.

- Specify the governing law: Indicate that the agreement will be governed by the laws of the State of Maryland. This is crucial for legal enforceability.

- Include clauses for default and remedies: Describe what constitutes a default under the agreement (e.g., missed payments) and the remedies available to the lender if the borrower fails to meet their obligations.

- Signatures: Both the lender and the borrower must sign and date the form. It is also advisable to have the signatures witnessed or notarized for additional legal validity.

Once you have completed the form, review all sections carefully to ensure accuracy and completeness. Both parties should retain a copy of the fully executed agreement for their records. Remember, this document is not only a reflection of your agreement but also serves as a legal tool to resolve any disputes that may arise. Should you have any doubts or require clarification on any part of the process, consulting with a legal professional is recommended to ensure that your interests are fully protected.

More About Maryland Loan Agreement

What is a Maryland Loan Agreement form?

A Maryland Loan Agreement form is a legal document prepared and used in the state of Maryland. It outlines the terms and conditions under which a loan is provided from one party (the lender) to another (the borrower). This document is crucial as it legally binds both parties to the agreement, detailing the loan amount, repayment schedule, interest rates, and any other conditions agreed upon.

Who needs to sign the Maryland Loan Agreement form?

The Maryland Loan Agreement form must be signed by both the lender and the borrower. In some cases, if a guarantor is part of the agreement, to ensure the loan is paid back, the guarantor must also sign the form. Witnesses or a notary public may also be required to sign, adding an extra layer of legal validation.

What should be included in a Maryland Loan Agreement form?

A comprehensive Maryland Loan Agreement form should include the following information:

- The full names and contact details of the lender and the borrower.

- The amount of money being loaned.

- The interest rate, if applicable, and how it is calculated.

- Repayment terms, including the schedule and any potential penalties for late payments.

- Any collateral securing the loan.

- Signatures of all parties involved, including any witnesses or a notary public.

Are there any specific requirements for a Maryland Loan Agreement form to be valid?

For a Maryland Loan Agreement form to be considered valid, it must be in writing and include the signatures of all parties involved. The document should clearly detail the loan's terms and conditions, including the loan amount, interest rate, and repayment schedule. It's also recommended to have the agreement witnessed or notarized to prevent any future disputes.

Can the terms of a Maryland Loan Agreement form be modified after signing?

Yes, the terms of a Maryland Loan Agreement form can be modified after it has been signed, but only if all parties involved agree to the changes. Any amendments should be made in writing and attached to the original agreement. Both the lender and borrower should sign the amendments to ensure they are legally binding.

What happens if the borrower fails to repay the loan as agreed in the Maryland Loan Agreement form?

If the borrower fails to repay the loan according to the terms outlined in the Maryland Loan Agreement form, several actions can be taken by the lender. These may include initiating legal proceedings to recover the loan amount, claiming any collateral that was put up against the loan, or reporting the borrower to credit reporting agencies, which could negatively impact the borrower's credit score. It's important for borrowers to communicate with lenders if they are unable to meet their repayment obligations, as solutions such as modifying the repayment terms may be possible.

Common mistakes

When filling out the Maryland Loan Agreement form, individuals often make mistakes that can significantly impact the validity and enforcement of the document. Paying attention to common errors and taking steps to avoid them can streamline the loan process and protect the interests of all parties involved. Here are ten mistakes to watch for:

- Not specifying the loan amount clearly - Failure to clearly state the exact loan amount can lead to disputes and confusion.

- Omitting the interest rate - Neglecting to include the interest rate or incorrectly stating it can affect the repayment terms and the overall cost of the loan.

- Forgetting to define repayment terms - It's crucial to detail the repayment schedule, including due dates and any grace periods, to ensure timely payments.

- Ignoring late payment penalties - Without specifying penalties for late payments, enforcing these fees can become problematic.

- Overlooking collateral agreements - If the loan is secured, failing to describe the collateral can jeopardize the lender's ability to claim it in case of default.

- Inadequate description of default terms - Clearly outlining what constitutes a default is essential for taking appropriate actions if the borrower fails to meet the agreement's terms.

- Leaving out governing law provisions - Specifying which state's law governs the agreement is important for resolving any legal disputes.

- Forgetting to include signatures - The agreement must be signed by all parties to be legally binding. Missing signatures can invalidate the document.

- Failing to print names and titles - Alongside signatures, printed names and titles clarify who exactly has agreed to the terms.

- Not having the document witnessed or notarized - Depending on the nature of the loan and the amount, having the agreement witnessed or notarized can add an extra layer of legal protection.

By avoiding these common mistakes, individuals can ensure that the Maryland Loan Agreement form is completed accurately, providing security and clarity for both lenders and borrowers.

Documents used along the form

In today's lending landscape, the Maryland Loan Agreement form is a crucial document for delineating the terms of a loan between a borrower and a lender. However, to ensure the legal enforceability and clarity of the entire agreement, several other documents are often used in tandem with this form. Each of these complements the Loan Agreement by covering aspects not fully detailed within the agreement itself, offering a comprehensive legal framework that protects all parties involved.

- Promissory Note: This document acts as a promise by the borrower to pay back the loan amount under agreed-upon terms. It's a crucial document that outlines the repayment structure.

- Guarantee Agreement: Sometimes, a third party will guarantee the loan, promising to repay the debt if the original borrower fails to do so. This agreement outlines the guarantor’s responsibilities.

- Mortgage or Deed of Trust: For loans secured against property, this document provides the legal framework that allows the lender to take title of the property if the borrower defaults on the loan.

- Security Agreement: If personal property is used to secure the loan, this agreement gives the lender a security interest in the specified assets.

- Disclosure Statement: Required by federal law, this document provides the borrower with information about the costs of the loan, including the annual interest rate, fees, and other charges.

- Insurance Documents: If insurance is required as a condition of the loan, such as property or life insurance, these documents provide proof that the borrower has secured the necessary coverage.

- Title Documents: For loans secured by vehicles or other titled property, these documents verify the lender's lien on the property as collateral for the loan.

- Amortization Schedule: This provides a detailed payment plan for the loan, including interest and principal amounts, helping both borrower and lender track the balance over time.

- Modification Agreement: Should the terms of the original loan agreement change, this document outlines the modifications agreed upon by both parties, ensuring that the loan remains in good standing.

Correctly utilizing these documents alongside the Maryland Loan Agreement form not only strengthens the legal validity of the loan arrangement but also ensures clarity and fairness for all parties involved. By covering every angle, from repayment terms to security interests, borrowers and lenders can enter into agreements with confidence, knowing their interests are protected.

Similar forms

The Maryland Loan Agreement form is similar to other financial documents used in lending and borrowing transactions. These documents ensure that all the terms and conditions of a financial agreement are legally documented and agreed upon by both parties. Among these, the Promissory Note and the Personal Loan Agreement stand out as particularly comparable.

Promissory Note: This is a straightforward document in which a borrower agrees to repay a certain amount of money to a lender within a specified timeline. The Maryland Loan Agreement form shares its basic structure with a Promissory Note, as both outline the loan amount, interest rate, repayment schedule, and the consequences of default. However, the Loan Agreement form provides a more detailed framework by also covering legal remedies and specifying the obligations and rights of both the lender and the borrower comprehensively.

Personal Loan Agreement: Much like the Maryland Loan Agreement form, a Personal Loan Agreement encompasses the particulars of a loan between individuals. It includes detailed information about the loan amount, interest rate, repayment terms, and what happens if the loan isn’t repaid as agreed. The key similarity lies in their thoroughness in documenting the responsibilities and protections for both parties involved, ensuring that personal relationships do not hinder the enforcement of the agreement. Yet, the Maryland Loan Agreement form often incorporates more specific legal clauses tailored to the state's legal guidelines, enhancing its enforceability within Maryland.

Dos and Don'ts

When filling out the Maryland Loan Agreement form, attention to detail and thoroughness are crucial for ensuring the validity and enforceability of the agreement. Below are essential guidelines to follow, categorized into things you should and shouldn't do, to assist in completing the form accurately.

Things You Should Do

- Ensure all parties' names and contact information are correct and complete. This establishes the clear identity of those involved in the agreement.

- Specify the loan amount in words and figures to avoid any ambiguity regarding the financial obligations.

- Include a detailed repayment plan, specifying dates, amounts, and any interest applied. This clarifies the schedule and terms of repayment for all parties.

- State the purpose of the loan clearly. Defining how the loaned funds will be used ensures mutual understanding and agreement on the use of funds.

- Sign and date the form in the presence of a witness or notary, if required. This step adds a level of formality and legal reinforcement to the agreement.

- Keep a copy of the signed agreement for your records. Having a record is crucial for reference in case of disputes or clarifications needed later.

Things You Shouldn't Do

- Leave any sections blank. Unfilled sections can lead to misunderstandings or exploitation. If a section doesn't apply, mark it as "N/A."

- Omit specifying any collateral, if applicable. Failure to do so could affect the enforceability of securing the loan.

- Forget to include any agreed-upon penalties for late payments or default. Such terms are essential for protecting the interests of the lender.

- Sign the agreement without thoroughly reading and understanding every term. This could lead to agreeing to terms that are not in your favour.

- Overlook obtaining legal advice if there are any uncertainties. Consulting a professional can prevent future legal complications.

- Assume verbal agreements are sufficient. Without written and signed documentation, enforcing agreement terms becomes significantly more challenging.

By diligently adhering to these guidelines, individuals can ensure that their Maryland Loan Agreement form is filled out accurately and effectively, paving the way for a clear and enforceable agreement.

Misconceptions

When dealing with loan agreements, specifically within the context of Maryland, individuals often encounter a variety of misconceptions. These misunderstandings can lead to confusion, mismanagement of agreements, and sometimes even legal issues. It’s vital to dispel these myths for a clearer and more accurate handling of loan agreements in Maryland.

Only Banks Can Issue Loan Agreements: A common misconception is that loan agreements in Maryland can only be issued by banks or financial institutions. However, private entities and individuals are also legally allowed to enter into loan agreements, as long as they comply with federal and state regulations.

Oral Agreements Are Just as Binding as Written Ones: While oral agreements can be legally binding, Maryland's Statute of Frauds requires certain agreements to be in writing to be enforceable. This typically includes loan agreements, especially those involving substantial amounts of money, to prevent misunderstandings and provide clear terms.

All Loan Agreements Are the Same: Each loan agreement is unique and can be tailored to the specific terms negotiated between the lender and the borrower. Elements such as the interest rate, repayment schedule, and collateral (if any) can vary significantly from one loan agreement to another.

There's No Need for Witnesses or Notarization: While not always a legal requirement for loan agreements in Maryland, having the document witnessed or notarized can add a layer of validation and protection for both parties involved. It can also help in the enforceability of the agreement.

Signing a Loan Agreement Means You Are Immediately in Debt: The actual incurring of debt occurs not upon signing the agreement, but when the funds are dispersed by the lender to the borrower. The agreement simply sets the legal framework for the loan to be provided and repaid.

Prepayment Penalties Are Illegal: Many believe that lenders cannot charge prepayment penalties if a borrower decides to pay off a loan early in Maryland. This is not entirely true. The legality of prepayment penalties depends on the specific terms of the loan agreement and applicable state laws. Some loan agreements legitimately include penalties for early repayment.

Understanding these misconceptions is crucial for anyone involved in the lending process in Maryland. Clearing up these myths enhances transparency and ensures that both lenders and borrowers enter into agreements with a full understanding of their rights and obligations.

Key takeaways

When preparing and utilizing the Maryland Loan Agreement form, it is essential to handle the document with accuracy and a keen attention to detail. This agreement is a binding document that outlines the loan specifics between a borrower and a lender, often used to ensure clarity and protect both parties' interests. Here are nine key takeaways to consider:

- Ensure all parties involved have a clear understanding of the loan's terms, including the loan amount, interest rate, repayment schedule, and any collateral involved. Clear communication can prevent misunderstandings down the line.

- Accurately fill out the borrower's and lender's information, including full legal names, addresses, and contact information. This information is crucial for the legal enforceability of the document.

- Determine the type of interest rate to be applied to the loan, whether fixed or variable. This influences the loan's cost over time and affects the borrower's repayment amount.

- Clearly specify the loan repayment schedule, including the start date, frequency of payments (monthly, quarterly, etc.), and the duration of the loan. This ensures both parties agree on when and how the loan will be repaid.

- Include a clause about prepayment, specifying whether the borrower is allowed to pay off the loan early and if any penalties apply. This protects the lender’s interest while providing flexibility to the borrower.

- Outline the process for handling late payments or defaults, including any fees or penalties, and steps for resolving these situations. This provides a clear course of action for managing missed payments.

- Include any collateral securing the loan, if applicable, and describe it in detail. Collateral provides security for the lender and can affect the loan terms.

- Both parties should review the entire agreement before signing to ensure all information is correct and all terms are understood. This review process can prevent future conflicts.

- Signature sections for both the borrower and the lender are essential. Ensure these sections are duly filled to confirm that both parties agree to and accept the terms of the loan. Witnesses or notarization may also be required, depending on the nature of the loan and local regulations.

By carefully addressing these key points, individuals can facilitate a smoother loan process and foster a mutual understanding and agreement between the lender and borrower. This preparation can significantly reduce potential risks and misunderstandings throughout the life of the loan.

Additional Maryland Templates

Mobile Home Bill of Sale Template - It specifies the make, model, year, and serial number of the mobile home, ensuring accurate identification.

Maryland for Sale by Owner Contract - This legal agreement can cover various types of properties, including residential, commercial, and land.

What Is a Hold Harmless Agreement - Engaging in regular reviews of these agreements is recommended, especially when the nature of the associated risk might change over time.