Maryland 4A PDF Template

Understanding the Maryland 4A form is essential for businesses operating within the state. This document, overseen by the Department of Assessments and Taxation Personal Property Division, plays a critical role in the financial reporting and assessment of a business's property and assets. Structured to capture both the beginning and end of period financial positions, it requires detailed information on various assets, ranging from cash and securities to tangible property and equipment. Notably, it breaks down assets into categories such as current assets, property, plant and equipment, and intangible and other assets, providing a comprehensive overview of a company's financial status. Equally important, the form accounts for liabilities and equity, including accounts payable, long-term liabilities, and stockholder equity details, to give a rounded view of the business's financial health. Accurate completion of this form is not only a compliance issue but also a reflection of the company's financial wellbeing, making it a crucial document for business owners in Maryland. It's noteworthy that the form advises omitting the total columns when all assets are located within Maryland, emphasizing the form's focus on in-state business operations. This document's importance cannot be overstated, as it influences taxation and offers a snapshot of the company’s financial viability to both the state and potential investors.

Maryland 4A Sample

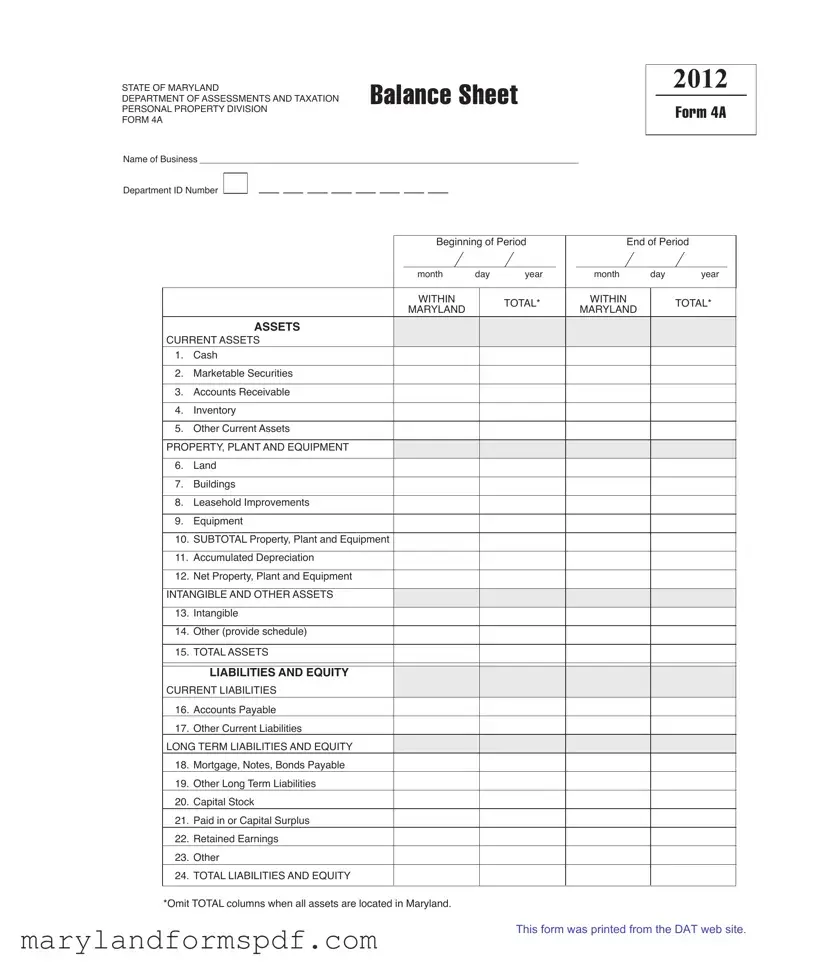

STATE OF MARYLAND |

BALANCE SHEET |

DEPARTMENT OF ASSESSMENTS AND TAXATION |

|

PERSONAL PROPERTY DIVISION |

|

FORM 4A |

|

Name of Business __________________________________________________________________________

Department ID Number

2012

FORM 4A

Beginning of Period |

|

End of Period |

|

||

month |

day |

year |

month |

day |

year |

WITHIN |

|

|

|

WITHIN |

|

|

|

TOTAL* |

|

TOTAL* |

|||

MARYLAND |

|

|

MARYLAND |

|

||

|

|

|

|

|

||

|

|

|

|

ASSETS

CURRENT ASSETS

1.Cash

2.Marketable Securities

3.Accounts Receivable

4.Inventory

5.Other Current Assets

PROPERTY, PLANT AND EQUIPMENT

6.Land

7.Buildings

8.Leasehold Improvements

9.Equipment

10.SUBTOTAL Property, Plant and Equipment

11.Accumulated Depreciation

12.Net Property, Plant and Equipment

INTANGIBLE AND OTHER ASSETS

13.Intangible

14.Other (provide schedule)

15.TOTAL ASSETS

lIABIlITIES AND EQUITY

CURRENT LIABILITIES

16.Accounts Payable

17.Other Current Liabilities

LONG TERM LIABILITIES AND EQUITY

18.Mortgage, Notes, Bonds Payable

19.Other Long Term Liabilities

20.Capital Stock

21.Paid in or Capital Surplus

22.Retained Earnings

23.Other

24.TOTAL LIABILITIES AND EQUITY

*Omit TOTAL columns when all assets are located in Maryland.

This form was printed from the DAT web site.

File Breakdown

| Fact Name | Description |

|---|---|

| Purpose | The Maryland Form 4A serves as a balance sheet for businesses to report their personal property to the Department of Assessments and Taxation (DAT). |

| Sections Included | Form 4A includes sections for reporting current assets, property, plant and equipment, intangible and other assets, liabilities, and equity. |

| Requirement | All businesses operating in Maryland are required to submit Form 4A annually to the Department of Assessments and Taxation. |

| Importance of Accuracy | Accurate reporting on Form 4A ensures correct assessment of personal property taxes, which supports local services such as schools and public safety. |

| Governing Law | Form 4A is governed by Maryland law, specifically the regulations stipulated by the Maryland Department of Assessments and Taxation. |

| Accessibility | The form is accessible online through the Maryland Department of Assessments and Taxation website, making it easy for businesses to comply with reporting requirements. |

Steps to Filling Out Maryland 4A

Filling out the Maryland 4A form is a straightforward process once you understand its parts and what information is required. This form serves as a detailed balance sheet for businesses, outlining their assets, liabilities, and equity positions over a specific period. Keeping this form accurate and up-to-date is crucial for compliance with the Maryland Department of Assessments and Taxation requirements. Let's go through the steps to fill it out correctly, ensuring that your business's financial position is accurately reported.

- Start by entering the Name of Business at the top of the form, ensuring it matches the name registered with the State of Maryland.

- Fill in the Department ID Number next to the business name, which is a unique identifier assigned to your business by the Maryland Department of Assessments and Taxation.

- Specify the reporting period by entering the Beginning and End dates under "month day year" for both the start and end of the fiscal period being reported.

- Under CURRENT ASSETS, list the amounts for:

- Cash

- Marketable Securities

- Accounts Receivable

- Inventory

- Other Current Assets

- In the PROPERTY, PLANT AND EQUIPMENT section, document the values for Land, Buildings, Leasehold Improvements, and Equipment. Add these figures to calculate the SUBTOTAL Property, Plant and Equipment, then subtract the Accumulated Depreciation to find the Net Property, Plant and Equipment.

- For INTANGIBLE AND OTHER ASSETS, note the values of Intangible and Other assets (providing a schedule for the other assets), and sum these to derive the TOTAL ASSETS.

- Under CURRENT LIABILITIES, fill in amounts for Accounts Payable and Other Current Liabilities.

- In the section for LONG TERM LIABILITIES AND EQUITY, complete the fields for:

- Mortgage, Notes, Bonds Payable

- Other Long Term Liabilities

- Capital Stock

- Paid in or Capital Surpetrol Surplus

- Retained Earnings

- Other

- If all assets are located in Maryland, omit the TOTAL columns as per the form's instruction.

- Review the completed form for accuracy, as it's essential that the reported figures accurately reflect your business's financial position for the specified period. Mistakes could lead to issues with the Maryland Department of Assessments and Taxation.

- After reviewing, sign and date the form as required and follow the submission instructions provided by the Maryland Department of Assessments and Taxation to complete the process.

Filling out the Maryland Form 4A might seem complex at first glance, but by following these steps, you can ensure that every section is accurately completed. This meticulous approach not only helps maintain compliance with state regulations but also offers a comprehensive overview of your business’s financial health over the reporting period. Should you encounter any difficulties or have specific questions regarding certain sections of the form, seeking professional advice might be beneficial to ensure all information is correct and up to date.

More About Maryland 4A

What is the Maryland 4A Form?

The Maryland 4A Form is a document used by the State of Maryland's Department of Assessments and Taxation Personal Property Division. It serves as a balance sheet for businesses to report the value of their personal property, both within the state of Maryland and in total. This form is essential for the calculation of personal property tax obligations in Maryland.

Who needs to file the Maryland 4A Form?

All businesses that have personal property in Maryland must file the Maryland 4A Form. This includes, but is not limited to, corporations, partnerships, sole proprietors, and limited liability companies. The requirement applies whether or not a business owns real estate in the state.

What information is required on the Maryland 4A Form?

The Maryland 4A Form requires detailed information about a business's assets, liabilities, and equity at the beginning and end of a reporting period. Specific sections include:

- Current Assets (e.g., Cash, Accounts Receivable, Inventory)

- Property, Plant, and Equipment (e.g., Land, Buildings, Equipment)

- Intangible and Other Assets (e.g., Intangible Assets, Other with a schedule)

- Liabilities and Equity (e.g., Current Liabilities, Long Term Liabilities, Equity)

Note: Total columns should be omitted when all assets are located within Maryland.

When is the Maryland 4A Form due?

The due date for filing the Maryland 4A Form is April 15th of each year. If this date falls on a weekend or holiday, the next business day becomes the due date. It is important to file on time to avoid penalties and interest.

How can a business file the Maryland 4A Form?

The form can be downloaded from the Department of Assessments and Taxation (DAT) website. Once completed, it must be submitted either electronically through the DAT's online filing system or mailed to the department. It is crucial to ensure that all information is accurate and complete to avoid issues with the state.

What happens if a business fails to file the Maryland 4A Form?

Failing to file the Maryland 4A Form can result in penalties, interest charges, and potential legal action. The state may estimate the value of a business's personal property and issue a tax bill based on that estimate. Moreover, continued failure to comply with filing requirements can lead to more serious consequences, including the revocation of the business's right to operate in Maryland.

Common mistakes

When filling out the Maryland 4A form, a crucial document for the Department of Assessments and Taxation, individuals often encounter a variety of pitfalls. This form, integral for accurately reporting a business's balance sheet, demands attentiveness to detail and a thorough understanding of the business's financial standing. Highlighted below are seven common mistakes to avoid to ensure the form is completed accurately and comprehensively.

Not Providing Complete Business Information: Many people forget to fill out the business name or Department ID Number at the beginning of the form. This basic yet critical information is essential for identifying your business within the state's system.

Incorrect Dates: It's common to see inaccuracies in the 'Beginning of Period' and 'End of Period' dates. These dates should reflect the fiscal year being reported, as they play a pivotal role in understanding the financial activities within that specific timeframe.

Omitting 'Within Maryland' Asset Values: The section meant to distinguish assets located within Maryland from those elsewhere is often overlooked. This distinction is crucial for accurate state tax assessment.

Miscalculating Totals: Errors in the 'TOTAL' columns, especially if all assets are located in Maryland and these columns are mistakenly filled, can lead to inaccuracies. Remember, if all assets are in Maryland, these columns should be omitted.

Forgetting to List Current Liabilities: The liabilities section, specifically current liabilities like accounts payable or other short-term financial obligations, is sometimes inaccurately reported or left blank. This oversight can significantly affect the financial picture presented to the department.

Incomplete Details on Property, Plant, and Equipment: The form requires; breakdowns of land, buildings, improvements, and equipment. A generic figure lumped together misses the opportunity to accurately report the value and state of the company's tangible assets.

Ignoring or Misreporting Intangible Assets: Intangible assets, often overlooked or undervalued, need accurate reflection on the form. Whether it's intellectual property or other non-physical assets, their inclusion is necessary for a complete assets report.

Avoiding these mistakes not only streamlines the reporting process but also ensures that the financial health of the business is accurately depicted in state records. The Maryland 4A form is a key component in maintaining transparency and compliance with the state's regulatory requirements, thereby necessitating careful attention and thoroughness when completing it.

Documents used along the form

When filing the Maryland Form 4A, which is a detailed Balance Sheet required by the Department of Assessments and Taxation Personal Property Division, businesses might need to include several other forms and documents to provide a complete view of their financial status. These additional documents play a crucial role in ensuring accurate and comprehensive financial reporting.

- Form 1 Personal Property Return: This form is essential for all businesses operating in Maryland. It provides a comprehensive overview of the business's personal property, including equipment, furnishings, and inventory. Submission of this form is crucial for accurate property tax assessment.

- Form BCA: Also known as the Business Corporation Assessment, this document is specifically for corporations. It details the corporation's assets, liabilities, and equity. It's often required along with the 4A form for a more in-depth analysis of a corporation's financial situation.

- Annual Report: This is a mandatory report for all businesses that outlines the company's activities throughout the previous year. It includes changes in ownership, address updates, and other pertinent information that might affect the assessment and taxation of the business.

- Personal Property Tax Exemption Application: For businesses that qualify for personal property tax exemptions, this form is critical. It outlines the criteria for exemption and, if applicable, must be filed along with the 4A to justify not paying personal property taxes on certain items.

Together, these documents provide a holistic view of a business's financial health and legal standing. It's important for businesses to keep these documents updated and accurate, as they significantly impact the assessment of taxes and the overall legal compliance of the business in Maryland.

Similar forms

The Maryland 4A form, primarily a comprehensive balance sheet for businesses, bears a resemblance to several other foundational financial and reporting documents used within the business and accounting worlds. Here, we'll explore its similarities with two such documents: the IRS Form 1120 and the Uniform Commercial Code-1 (UCC-1) Financing Statement.

First and foremost, the Maryland 4A form shows parallels with the IRS Form 1120, which is the U.S. Corporation Income Tax Return. Both documents require detailed financial information about a business, including assets, liabilities, and equity. The 4A form, much like the IRS Form 1120, is structured to present an overview of the company's financial standing, specifically targeting current assets, property, plant, and equipment, along with liabilities and equity. Where they particularly converge is in their demand for specificity regarding the company's financial status - albeit for different purposes: the 4A form for state-level personal property assessment and the 1120 for federal income taxation. Despite their different end-uses, the level of detail and structure provided in both forms underscores their objective of painting a comprehensive financial portrait of a business.

On another front, the Maryland 4A form shares attributes with the Uniform Commercial Code-1 (UCC-1) Financing Statement. The connection here is more about the role they play in the declaration and recording of assets, though for distinct reasons. The UCC-1 is instrumental in the process of securing a lender's interest in the borrower's personal property (which can range from fixtures to intangible assets) used as collateral for a loan. Similarly, the 4A form tracks the assets of a business within Maryland, including intangible assets and property, plant, and equipment. Both documents, therefore, serve as official records that identify and delineate assets, albeit one is for the security of creditor rights and the other for property tax assessment purposes. Though their objectives may diverge, the underlying principle of documenting assets provides a common ground.

Dos and Don'ts

When filling out the Maryland 4A form, there are specific actions individuals should take to ensure the process is completed correctly and efficiently. Likewise, there are actions that should be avoided to prevent common mistakes that could lead to inaccurate reporting or delays. Here are some of the dos and don'ts:

Things you should do:

- Verify your information: Ensure the Name of Business and Department ID Number are correctly entered. Double-check the dates marked for the Beginning and End of Period to ensure they accurately reflect the reporting period.

- Complete all relevant sections: Only omit the TOTAL columns if all assets are located within Maryland. For assets outside of Maryland, provide complete information in both the WITHIN MARYLAND and TOTAL columns.

- Provide detailed schedules: For line items such as "Other Current Assets" and "Other (provide schedule)" under the INTANGIBLE AND OTHER ASSETS section, attach detailed schedules as necessary. This enables a clear understanding of what comprises these totals.

- Calculate depreciation accurately: When listing Accumulated Depreciation, ensure the calculations are accurate to derive the correct Net Property, Plant, and Equipment value. This is crucial for an accurate representation of the business's financial position.

Things you shouldn't do:

- Ignore instructions: Do not skip reading the form's instructions, as they contain essential details for correctly filling out the form and ensuring that all required information is accurately reported.

- Omit totals where required: Do not omit the TOTAL columns unless it is confirmed that all assets are located within Maryland. Forgetting to include total values where necessary can lead to incomplete reporting.

- Estimate without documentation: Avoid making estimations for items like Inventory or Intangible Assets without having documentation to back up these figures. Estimates should be as accurate as possible and based on available data.

- Leave sections incomplete: Do not leave any sections that apply to your business incomplete. If a section does not apply, it's better to mark it as "Not Applicable" or "N/A" rather than leaving it blank, to show that it was reviewed but found to be irrelevant.

Misconceptions

There are several misconceptions about the Maryland 4A form that people often have. Clarifying these can help in understanding its purpose and how to properly complete it.

- It's only for large businesses: This is a common misconception. The Maryland 4A form is actually required for all businesses that have personal property assessed by the State of Maryland, regardless of size. This includes small businesses and sole proprietorships as well.

- It's a tax return: While related to taxes, the Maryland 4A form is technically not a tax return. It is a balance sheet that the Department of Assessments and Taxation uses to assess personal property taxes. The form provides a snapshot of the assets a business owns.

- Only tangible assets are reported: Another misconception is that only tangible assets like equipment and inventory need to be reported. However, the form also requires information on intangible assets and other types of property.

- All assets must be reported in total columns: The instructions specify to omit total columns when all assets are located within Maryland. This often leads to confusion, with the misconception being that totals are always required. This is not the case.

- The form is only for in-state businesses: Though it focuses on property within Maryland, out-of-state businesses with property in Maryland are also required to fill it out. The misconception arises from the emphasis on "within Maryland" in the asset categories.

- No schedule is required for "Other" assets: The form requests a schedule for "Other" assets under Intangible and Other Assets. Some believe a description in the form itself is sufficient, overlooking the need for a detailed schedule.

- Submitting Form 4A is the final step: After submitting Form 4A, businesses often think they have completed their filing obligations. In reality, they may need to complete additional steps, like filing annual reports or other forms, depending on their situation.

- It doesn't need to be filed annually: There's a belief that once the form is filed, it doesn't need to be updated or resubmitted annually. On the contrary, businesses must file a new Form 4A each year to accurately reflect changes in their assets.

Correcting these misconceptions is crucial for businesses to ensure compliance with Maryland's personal property tax regulations and to avoid potential penalties.

Key takeaways

The Maryland Form 4A, known as the Balance Sheet form, is crucial for businesses in the state as it provides the Department of Assessments and Taxation (DAT) with essential financial information. Understanding and correctly completing this form is vital for compliance and accurate reporting of a business's financial status. Here are 10 key takeaways for completing and using the Maryland 4A form:

- The form requires the business's name and Department ID Number at the top, which are essential for identifying the filing entity.

- It's important to accurately report the financial state at the beginning and end of the period, including month, day, and year, to show financial progression or regression over time.

- Businesses must report their current assets comprehensively, breaking them down into categories such as cash, marketable securities, accounts receivable, inventory, and other current assets, ensuring a complete snapshot of its liquidity.

- The section on property, plant, and equipment requires details like land, buildings, leasehold improvements, and equipment, which are critical for understanding the company's long-term assets.

- Reporting the accumulated depreciation separately allows the state to ascertain the net value of the physical assets after wear and tear.

- In the liabilities section, distinguishing between current liabilities, like accounts payable and other current liabilities, and long-term liabilities and equity, is crucial for assessing the company's immediate and future financial obligations.

- Details on long-term financial commitments such as mortgages, notes, bonds payable, and other long-term liabilities provide insight into the longevity and sustainability of the business's financial planning.

- Equity reporting, including capital stock, paid-in or capital surplus, and retained earnings, offers a picture of the company's financial health and stability from an ownership and investment perspective.

- If all assets are located within Maryland, the instruction to omit total columns simplifies reporting requirements, streamlining the process for businesses fully operational within the state.

- Lastly, additional details and schedules may be required for intangible and other assets, emphasizing the need for thorough documentation and transparency in financial reporting.

Understanding each component of the Maryland 4A form and its purpose aids businesses in accurate financial disclosure, fostering a transparent and compliant operational environment within the state.

Common PDF Templates

Maryland Retirement Tax Calculator - The form's design reflects the importance of accurate and clear communication between all parties involved in the rollover.

Maryland 502 - Always sign and date the form at the bottom to validate your withholding request.