Maryland 4B PDF Template

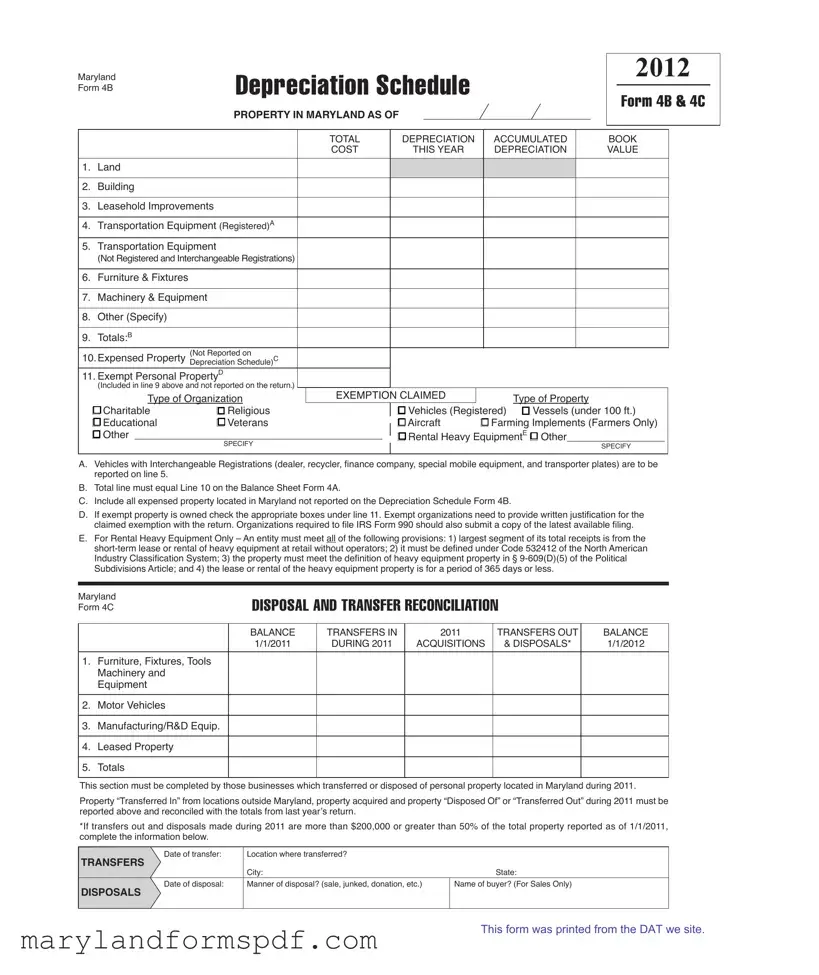

In the realm of business property management within Maryland, the Maryland Depreciation Schedule Form 4B functions as an essential document for reporting the current value of a company's assets. It meticulously categorizes property into various groups like land, buildings, leasehold improvements, vehicles, and more, requiring detailed information on their accumulated depreciation, book cost, and this year's depreciation value. Businesses use the form to present a clear picture of their tangible assets' worth over time. Besides factoring depreciation, the form accommodates exempt personal property, specifically delineating types of organizations and properties eligible for exemption — ranging from charitable to educational purposes and including specific items such as veterans' aircraft and farming implements. Moreover, companies dealing with changes such as disposals or transfers of personal property in Maryland must also complete the Maryland Form 4C to reconcile these activities. This form's structured approach not only aids in tax preparation and financial analysis but also ensures compliance with local regulations, making it imperative for Maryland businesses to understand and accurately complete this documentation annually.

Maryland 4B Sample

Maryland |

Depreciation Schedule |

|

Form 4B |

||

|

||

|

PROPERTY IN MARYlAND AS OF _____________________________ |

2012

Form 4B & 4C

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL |

|

|

DEPRECIATION |

|

|

ACCUMULATED |

|

BOOK |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

COST |

|

|

|

|

THIS YEAR |

|

|

DEPRECIATION |

|

VALUE |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

|

|

Land |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

|

|

Building |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

|

|

Leasehold Improvements |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

4. |

|

|

Transportation Equipment (Registered)A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

|

|

Transportation Equipment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

(Not Registered and Interchangeable Registrations) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

|

|

Furniture & Fixtures |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7. |

|

|

Machinery & Equipment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8. |

|

|

Other (Specify) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

|

|

Totals:B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

10.Expensed Property |

(Not Reported on |

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

Depreciation Schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

11. Exempt Personal PropertyD |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

(Included in line 9 above and not reported on the return.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

Type of Organization |

|

|

EXEMPTION CLAIMED |

|

|

Type of Property |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

n |

Charitable |

|

n |

Religious |

|

|

|

|

|

n |

|

Vehicles (Registered) |

n |

Vessels (under 100 ft.) |

||||||||||

|

|

|

|

Veterans |

|

|

|

|

|

|

|

Aircraft |

|

|

|

|

|

|

||||||||

|

|

|

n |

|

Educational |

|

n |

|

|

|

|

|

n |

|

|

n |

Farming Implements (Farmers Only) |

|||||||||

|

|

n |

Other ___________________________________________ |

|

|

n |

Rental Heavy EquipmentE |

n |

Other_________________ |

|||||||||||||||||

|

|

|||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

SPECIFY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SPECIFY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A.Vehicles with Interchangeable Registrations (dealer, recycler, finance company, special mobile equipment, and transporter plates) are to be reported on line 5.

B.Total line must equal Line 10 on the Balance Sheet Form 4A.

C.Include all expensed property located in Maryland not reported on the Depreciation Schedule Form 4B.

D.If exempt property is owned check the appropriate boxes under line 11. Exempt organizations need to provide written justification for the claimed exemption with the return. Organizations required to file IRS Form 990 should also submit a copy of the latest available filing.

E.For Rental Heavy Equipment Only – An entity must meet all of the following provisions: 1) largest segment of its total receipts is from the

Maryland Form 4C

DISPOSAL AND TRANSFER RECONCILIATION

|

|

BALANCE |

TRANSFERS IN |

2011 |

TRANSFERS OUT |

BALANCE |

|

|

1/1/2011 |

DURING 2011 |

ACQUISITIONS |

& DISPOSALS* |

1/1/2012 |

|

|

|

|

|

|

|

1. |

Furniture, Fixtures, Tools |

|

|

|

|

|

|

Machinery and |

|

|

|

|

|

|

Equipment |

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Motor Vehicles |

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Manufacturing/R&D Equip. |

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Leased Property |

|

|

|

|

|

|

|

|

|

|

|

|

5. |

Totals |

|

|

|

|

|

|

|

|

|

|

|

|

This section must be completed by those businesses which transferred or disposed of personal property located in Maryland during 2011.

Property “Transferred In” from locations outside Maryland, property acquired and property “Disposed Of” or “Transferred Out” during 2011 must be reported above and reconciled with the totals from last year’s return.

*If transfers out and disposals made during 2011 are more than $200,000 or greater than 50% of the total property reported as of 1/1/2011, complete the information below.

Date of transfer: |

Location where transferred? |

|

TRANSFERS |

|

|

|

City: |

State: |

Date of disposal: |

Manner of disposal? (sale, junked, donation, etc.) |

Name of buyer? (For Sales Only) |

DISPOSAlS

This form was printed from the DAT we site.

File Breakdown

| Fact | Detail |

|---|---|

| Purpose | The Maryland Form 4B is intended for reporting depreciation schedules of property within Maryland. |

| Components | It includes categories such as Land, Buildings, Leasehold Improvements, Various Types of Equipment, Furniture & Fixtures, and more. |

| Exemptions | Exemptions can be claimed for certain types of property and organizations, such as charitable, religious, educational, among others. |

| Special Conditions | The form specifies conditions for rental heavy equipment to be eligible for exemptions, including being classified under NAICS Code 532412 and meeting certain operational benchmarks. |

| Governing Law | The form is governed by Maryland law, specifically mentioning requirements under § 9-609(D)(5) of the Political Subdivisions Article for certain property types. |

Steps to Filling Out Maryland 4B

Once it's time to tackle the Maryland Depreciation Schedule Form 4B, it's crucial to approach it with all the necessary information in hand. This form plays an indispensable part in accurately reporting your business's tangible personal property and its depreciation within Maryland. Getting the details right not only ensures compliance with Maryland tax regulations but also helps in accurately reflecting the financial health of your business. Below, find a simple guide to completing the form step by step.

- At the top of the form, fill in the date to indicate the current year. This documents the year for which you are reporting the property and depreciation values.

- Under the section titled PROPERTY IN MARYLAND AS OF, list each type of property owned by the business. This includes land, buildings, leasehold improvements, registered and non-registered transportation equipment, furniture and fixtures, and machinery and equipment. If there are other types of properties not listed, specify these under "Other."

- Next to each property type, enter the ACQUIRED BOOK COST. This is the original cost of the property to your business before depreciation.

- In the ACCOMULATED DEPRECIATION column, enter the total depreciation that has been claimed on each asset since it was acquired up to the beginning of the current year.

- Determine the THIS YEAR DEPRECIATION value for each asset type and list it. This is the amount of depreciation you're claiming for the current year.

- Calculate and fill in the VALUE column, which represents the current book value of each asset type after accounting for this year's depreciation.

- In the section for Totals:B, ensure that your total values match those on Line 10 of the Balance Sheet Form 4A to maintain consistency across your financial reporting.

- If you have any expensed property not reported on the Depreciation Schedule Form 4B but located in Maryland, include it under Expensed Property (Not Reported on C Depreciation Schedule).

- Review line 11 for Exempt Personal Property. If applicable, check the boxes that correspond to your property's exemption status, such as charitable, religious, or educational, and provide the necessary documentation as described in the instructions.

- For businesses with property that falls under special categories, such as rental heavy equipment, ensure you meet the listed criteria and specify the type of exemption claimed.

- Finally, if your business transferred or disposed of personal property during the previous year, complete the Maryland Form 4C provided at the bottom of the form to reconcile balance transfers, acquisitions, and disposals.

After completing the Maryland Depreciation Schedule Form 4B, review all entries for accuracy before submission. Ensuring that every piece of information is correct and properly recorded is essential for remaining in good standing with Maryland tax obligations. Keep a copy of the completed form for your records and be prepared to provide supporting documents if requested.

More About Maryland 4B

What is the purpose of the Maryland Depreciation Schedule Form 4B?

The Maryland Depreciation Schedule Form 4B serves to report the depreciation of a business's personal property located within Maryland. The form meticulously tracks the change in value of the business's assets over time, taking into account the wear and tear, age, and usage that reduces the value of these assets. It includes various categories of property such as land, buildings, leasehold improvements, transportation equipment, and more. By filling out this form, businesses provide necessary information that influences their personal property tax liabilities in Maryland.

How do I determine the total depreciation to report on Maryland Form 4B?

To accurately determine the total depreciation to report on the Maryland Form 4B, follow these steps:

- Review each category of property listed on the form, including land, buildings, transportation equipment, furniture & fixtures, and machinery & equipment, among others.

- For each category, calculate the annual depreciation based on the acquisition cost, applicable depreciation rate, and age of the property. This might require consultation with accounting standards or a professional accountant.

- Add the depreciation calculated for each category to find the total depreciation for the current year. This figure should be entered in the "TOTAL DEPRECIATION ACCUMULATED" section of the form.

- Update the "BOOK COST" and "THIS YEAR DEPRECIATION" columns accordingly for each category to reflect the correct depreciated value of each asset.

Remember, the total line must equal the line 10 on the Balance Sheet Form 4A, ensuring consistency across financial documents.

What is the significance of exempt personal property on Maryland Form 4B?

Exempt personal property plays a crucial role in the Maryland Form 4B as it affects the taxable value of a business's assets. Exempt personal property includes assets that are not subject to personal property tax due to their qualification for certain exemptions. These exemptions might be based on the nature of the organization (such as charitable, religious, or educational) or the type of property (such as registered vehicles, farming implements, and rental heavy equipment under specific conditions). Identifying and properly listing exempt personal property ensures an accurate calculation of property taxes, potentially reducing the tax liabilities for businesses. It is essential for organizations to provide written justification for the exemption claimed and, if applicable, submit a copy of their IRS Form 990 to support their exemption status.

How should transfers and disposals of property reported on Form 4C relate to Form 4B?

Form 4C, titled "DISPOSAL AND TRANSFER RECONCILIATION," complements the information provided in Form 4B by detailing the acquisition, disposal, and transfer activities concerning business's personal property within a specific timeframe. Here’s the relationship:

- Properties that have been transferred into, acquired, or disposed of in Maryland during the specified period must be reported on Form 4C. This includes providing details on the method and particulars of these transactions.

- These recorded activities on Form 4C must then be reconciled with the totals from last year’s return, impacting the overall reported values and depreciation calculations in Form 4B.

- Significantly, if the value or volume of disposals and transfers out during the specified period exceeds the thresholds provided, detailed information must be furnished below the main table on Form 4C, affecting the property's book value and depreciation reported in Form 4B.

Together, Forms 4B and 4C provide a comprehensive view of a business’s personal property status, ensuring accurate tax reporting and compliance.

Common mistakes

When businesses and organizations fill out the Maryland Depreciation Schedule Form 4B, errors can hinder accurate reporting and compliance with state requirements. Here are five common mistakes to avoid:

-

Not accurately distinguishing between categories of property. Each type of asset must be reported under the correct category (e.g., "Land," "Building," "Leasehold Improvements"). Misclassification can lead to incorrect depreciation calculations and potential issues with compliance.

-

Omitting the cost and depreciation information for each property type. It's crucial to detail the original cost, the accumulated depreciation, and the depreciation expense for the current year for each property listed to ensure accurate valuation and depreciation accounting.

-

Failing to report all expensed property located in Maryland not reported on another schedule (Designated as "Expensed Property" in the Form 4B). Overlooking or excluding these details can lead to discrepancies in the total asset value reported to the state.

-

Incorrectly claiming exemptions without providing the necessary documentation or justification. For any exemptions under "Exempt Personal Property," organizations must provide a written justification for the claimed exemption, and, if applicable, include a copy of the latest IRS Form 990 filing.

-

Not completing the Disposal and Transfer Reconciliation section accurately when applicable. For businesses that have transferred or disposed of personal property within the specified time frame, all details of the transactions, including dates, locations, and manner of disposal, need to be thoroughly documented to reconcile with previous year's totals.

Avoiding these mistakes not only ensures compliance with Maryland's reporting requirements but also aids in the accurate reflection of an organization's financial health through its reported assets and depreciation schedules.

Documents used along the form

When dealing with the Maryland Depreciation Schedule Form 4B, understanding the other forms and documents often used in conjunction can simplify the process. These supplemental materials ensure accurate reporting and compliance with Maryland's tax regulations. From the initiation of declaring assets through to their disposal, each document plays a crucial role in the effective management of personal property taxes within the state.

- Form 4A: Balance Sheet Form – This document complements the Form 4B by providing a detailed overview of a business's financial situation, including assets, liabilities, and equity. It's vital for reconciling the total depreciation reported.

- Form 4C: Disposal and Transfer Reconciliation – Necessary for businesses that have transferred or disposed of personal property in Maryland. It details acquisitions, disposals, and the balances of personal property at the beginning and end of the reporting period.

- Annual Report: Filed with the Maryland Department of Assessments and Taxation, this report updates the business information and ownership details, crucial for keeping the business in good standing.

- Personal Property Tax Return: Required by all businesses owning personal property in Maryland, this return includes detailed information on owned property, its cost, and accumulated depreciation.

- IRS Form 990: For tax-exempt organizations, this form provides the IRS with information on the organization's activities, governance, and detailed financial information. Its submission supports exemption claims on the Maryland Form 4B.

- Schedule A: Real Property Information – This form details all real property owned by a business in Maryland, necessary for accurate property tax assessment and calculation.

- Exemption Application: Used by businesses to apply for tax exemption on certain types of property, such as that used for religious, charitable, or educational purposes, this application must be documented and justified.

- Proof of Ownership: Documents such as titles, bills of sale, or purchase agreements verify the ownership of the listed items on Form 4B, critical for supporting depreciation and valuation claims.

- NAICS Classification Proof: For businesses like rental heavy equipment entities, documentation proving their classification under the North American Industry Classification System (NAICS) is necessary for certain exemptions or categories in the Form 4B.

Properly managing and submitting these documents alongside the Maryland Form 4B ensures a smoother process for tax reporting and compliance. Whether you're declaring new acquisitions, transferring assets, or claiming exemptions, each document has its specific role in painting a complete picture of your business's personal property status. Keeping them in order and up to-date can significantly ease the administrative burden and assist in precise tax preparation.

Similar forms

The Maryland 4B form is similar to various other state and federal forms used for financial and tax reporting purposes, particularly those relating to the depreciation of assets. These documents share common objectives and structures but are tailored to meet specific regulatory requirements or jurisdictions. Below are a couple of examples illustrating these similarities:

IRS Form 4562 - Depreciation and Amortization: The resemblance between the Maryland 4B form and IRS Form 4562 is quite pronounced. Both forms are designed to track the depreciation of property and equipment over time. They require the taxpayer to list assets, their cost, accumulated depreciation, and the depreciation expense for the current year. While the Maryland 4B form specifically targets property located in Maryland, IRS Form 4562 applies to the depreciation and amortization for assets on a nationwide basis, serving federal tax purposes. This broad similarity underscores their role in ensuring that businesses accurately account for the diminishing value of their assets.

Uniform Capitalization Rules under IRC §263A: Although not a form, the Uniform Capitalization Rules share a thematic connection with the Maryland 4B form, focusing on how expenses related to tangible property are accounted for. The Maryland 4B form's requirements for reporting depreciation on assets like machinery, equipment, and buildings align with the broader accounting principles mandated by §263A, which governs the capitalization and inclusion of certain costs in the basis of produced property or property acquired for resale. Both the Maryland 4B form and the Uniform Capitalization Rules aim to standardize the way businesses report the costs and value of their physical assets, impacting the financial and tax treatment of these assets over time.

Dos and Don'ts

Filling out the Maryland 4B form, an essential document for reporting personal property depreciation for tax purposes, requires careful attention to detail. Here are nine guidelines to ensure both accuracy and compliance:

- Do carefully review all items listed on the form to ensure that you are including all property subject to depreciation. This includes buildings, leasehold improvements, furniture, and more.

- Don't overlook the specifics required under each category. For example, transportation equipment must be distinguished between registered and not registered. Reporting inaccurately can lead to compliance issues.

- Do calculate depreciation accurately for each item. This calculation must reflect the current year's depreciation and the accumulated depreciation to date.

- Don't guess or estimate figures. Use actual costs and depreciation schedules to report the book cost and depreciation values. Accuracy is crucial for compliance and audit purposes.

- Do specify any items listed under "Other." Vague or incomplete descriptions may raise questions during reviews or audits.

- Don't include expensed property already reported on another depreciation schedule or form. This prevents duplicating entries and ensures the total reported value is accurate.

- Do check and claim exemptions accurately. If you qualify for exemptions, whether for charitable, educational, or other qualifying organizations, ensure you provide the necessary documentation and justification as required.

- Don't forget to report all property disposed of or transferred within the reported year. This section requires detailed information about the manner of disposal, dates, and recipient details if applicable.

- Do provide complete information about the organization and the type of property for which you're claiming an exemption. This includes selecting the appropriate box and specifying the type of property, ensuring any exempt property is properly documented and justified.

Adherence to these guidelines not only facilitates compliance with Maryland's tax laws but also minimizes the risk of errors or omissions that could lead to fines, penalties, or delays. As with all tax documents, thoroughness, accuracy, and timely submission are key to a smooth process.

Misconceptions

When it comes to the Maryland Depreciation Schedule Form 4B, there are several common misconceptions that can lead to confusion and errors in filing. Understanding these misconceptions is crucial for accurately completing the form and ensuring compliance with Maryland tax laws. Here are five common misconceptions explained:

- Only tangible assets need to be reported: There's a misconception that Form 4B only requires the reporting of tangible assets like buildings and machinery. However, the form also requires the reporting of intangible assets if they are subject to depreciation. This includes items such as leased land improvements and certain types of software.

- Land is depreciable: A common mistake is assuming that land can be depreciated. The form does list 'Land' as a category, but it's important to remember that land itself is not depreciable. The value listed for land should remain constant, as it reflects the cost basis, not a depreciated value.

- All vehicles are reported the same way: Vehicles are categorized differently based on their registration and usage. Transportation Equipment (Registered) and Transportation Equipment (Not Registered and Interchangeable Registrations) are reported separately. This distinction is crucial for businesses that own a variety of vehicles, as it affects depreciation calculations and tax liability.

- Expensed Property is not relevant: Some may think that expensed property, which refers to items fully deducted in the year they were purchased, does not need to be reported on Form 4B. However, the form explicitly asks for information on expensed property located in Maryland, underscoring the need to report it even though it might not be depreciated.

- Exemptions are automatically granted: While the form provides a section for claiming exemptions for certain types of organizations and properties, these exemptions are not granted automatically. Organizations must provide adequate documentation and justification for exemptions claimed, such as a copy of the latest IRS Form 990 for exempt organizations. Simply checking a box does not guarantee exemption status.

Correctly understanding and addressing these misconceptions about the Maryland Depreciation Schedule Form 4B is essential for proper compliance and avoiding potential audits or penalties. By recognizing the requirements and nuances of the form, businesses can ensure accurate and timely filings.

Key takeaways

Understanding the Maryland Form 4B, the Depreciation Schedule, is crucial for businesses operating within the state. Here are key takeaways about how to properly fill out and use this form:

- Accurate Reporting: Form 4B requires a detailed account of a business's property depreciation over the past year. Each item, from land and buildings to furniture, must be listed with its accumulated depreciation and current book value.

- Exempt Property: It is important to identify any property that may qualify as exempt, such as vehicles registered for charitable or educational purposes. Ensure that all relevant boxes are checked under line 11 and any necessary documentation for exemption claims is provided.

- Expensed Property: Any property located in Maryland that has been expensed and not reported on the Depreciation Schedule needs to be included on this form. This ensures comprehensive reporting and can affect the accuracy of your tax obligations.

- Disposal and Transfer Reconciliation: For businesses that have disposed of or transferred personal property within the covered year, Form 4C is also pivotal. The reconciliation of balances, acquisitions, disposals, and transfers provide a clear picture of the changes in assets, affecting depreciation calculations and tax responsibilities.

Properly filling out the Maryland Form 4B and its associated documents ensures compliance with Maryland's tax laws and helps businesses maintain accurate financial records. Take the time to report each piece of property accurately, claim any applicable exemptions with the necessary proof, and do not overlook the inclusion of expensed property not previously reported on the depreciation schedule. Being diligent in these areas safeguards against potential issues and ensures that your business's reporting is as accurate and beneficial as possible.

Common PDF Templates

Mw506nrs - Transparency in the property sale process is emphasized through detailed reporting requirements.

Maryland Amended Tax Return - Form 505X allows for the correction of Maryland tax withheld for nonresidents.

How to Write a Land Purchase Agreement - Incorporates regulatory compliance with lead-based paint, ensuring buyers are fully informed about potential hazards in older homes.