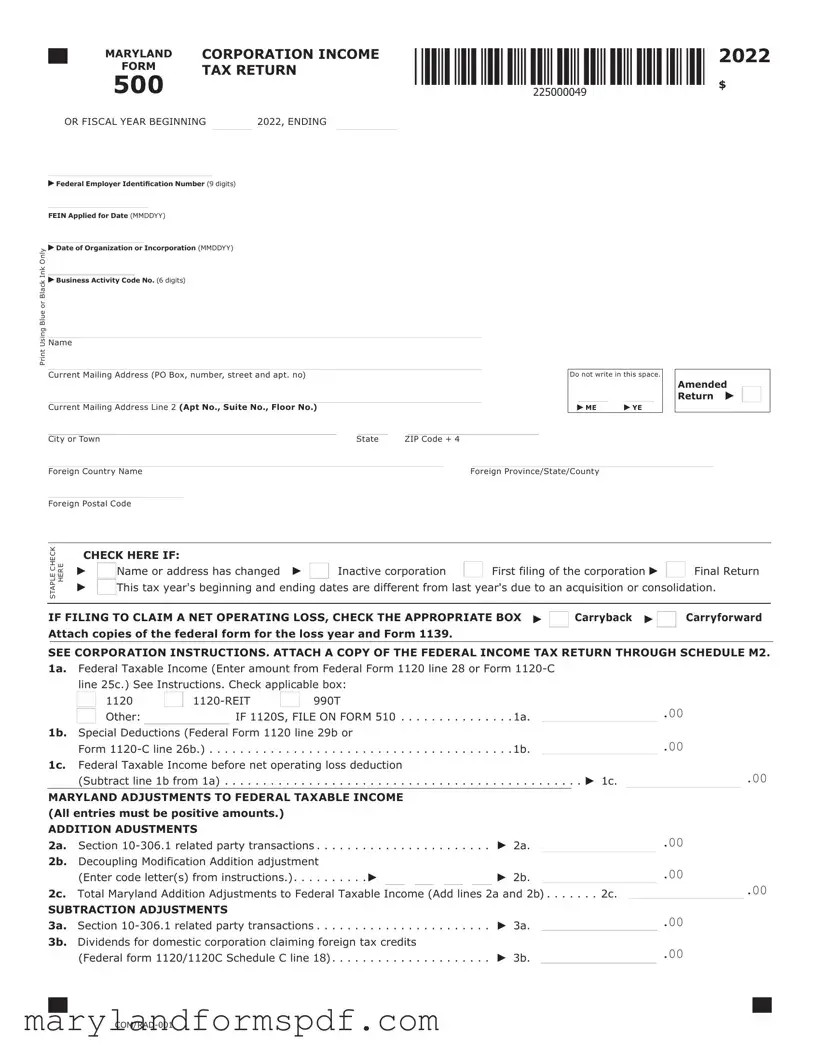

Maryland 500 PDF Template

Navigating the intricacies of corporate tax requirements can be a daunting task for any business operating within Maryland. The Maryland Corporation Income Tax Return, commonly known as Form 500, stands as a comprehensive document designed to streamline the tax filing process for corporations. Encompassing the fiscal year of 2020 or any other applicable fiscal period, this form mandates detailed information ranging from the Federal Employer Identification Number (FEIN) and the date of the corporation's organization or incorporation, to an exhaustive record of the corporation's income, deductions, and taxes due. The form also caters to specific scenarios such as amended returns, claiming net operating losses, and providing details for direct deposits of refunds. Importantly, it instructs corporations on adjusting their federal taxable income for Maryland-specific additions and subtractions, emphasizing the state's unique tax considerations. Aimed at ensuring accuracy and compliance, Form 500 includes sections for Maryland modifications, apportionment of income for multistate corporations, and details of any business tax credits claimed. As a filing requirement, the form encompasses a broad spectrum of data collection and computation essential for accurately determining a corporation's tax liability to Maryland, reflecting both the complexity and the importance of thorough preparation in the corporate tax filing process.

Maryland 500 Sample

|

MARYLAND |

CORPORATION INCOME |

2022 |

|||

|

|

|

|

|

|

|

|

FORM |

TAX RETURN |

|

|||

|

|

|||||

500 |

|

|||||

|

|

|

|

$ |

||

|

|

|

|

|

|

|

OR FISCAL YEAR BEGINNING |

|

2022, ENDING |

|

|

||

Print Using Blue or Black Ink Only

Federal Employer Identification Number (9 digits)

Federal Employer Identification Number (9 digits)

FEIN Applied for Date (MMDDYY)

Date of Organization or Incorporation (MMDDYY)

Date of Organization or Incorporation (MMDDYY)

Business Activity Code No. (6 digits)

Business Activity Code No. (6 digits)

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Current Mailing Address (PO Box, number, street and apt. no) |

|

|

|

|

|

|

|

|

Do not write in this space. |

|

Amended |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return |

|

|

|

Current Mailing Address Line 2 (Apt No., Suite No., Floor No.) |

|

|

|

|

|

|

|

|

|

ME |

YE |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

City or Town |

State |

ZIP Code + 4 |

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Foreign Country Name |

|

|

|

|

Foreign Province/State/County |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign Postal Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

STAPLE CHECK HERE

CHECK HERE IF: |

|

|

|

Name or address has changed |

Inactive corporation |

First filing of the corporation |

Final Return |

This tax year's beginning and ending dates are different from last year's due to an acquisition or consolidation.

IF FILING TO CLAIM A NET OPERATING LOSS, CHECK THE APPROPRIATE BOX

Carryback Attach copies of the federal form for the loss year and Form 1139.

Carryback Attach copies of the federal form for the loss year and Form 1139.

Carryforward

SEE CORPORATION INSTRUCTIONS. ATTACH A COPY OF THE FEDERAL INCOME TAX RETURN THROUGH SCHEDULE M2.

1a. |

Federal Taxable Income (Enter amount from Federal Form 1120 line 28 or Form |

|

|

|

|

|

|

|

|||||||||||||

|

line 25c.) See Instructions. Check applicable box: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

1120 |

990T |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Other: |

|

IF 1120S, FILE ON FORM 510 |

|

|

|

|

. . .1a. |

|

|

|

|

.00 |

|

|

||||||

|

|

. . . . . . |

|

|

|

|

|

|

|

||||||||||||

1b. |

Special Deductions (Federal Form 1120 line 29b or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Form |

|

|

|

|

|

|

|

|

. . .1b. |

|

|

|

.00 |

|

|

|||||

|

. . . . . . . . . . . . |

. |

. . . . |

. . . . . . |

|

|

|

|

|

|

|

||||||||||

1c. |

Federal Taxable Income before net operating loss deduction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

(Subtract line 1b from 1a) |

|

|

|

|

|

|

|

|

|

|

. |

. 1c. |

.00 |

|||||||

|

. . . . . . . . . . . . |

. |

. . . . |

. . . . . . |

. . . . . . . |

|

. . . |

|

|

|

|

||||||||||

MARYLAND ADJUSTMENTS TO FEDERAL TAXABLE INCOME |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

(All entries must be positive amounts.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

ADDITION ADUSTMENTS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

2a. |

Section |

|

|

|

|

2a. |

|

|

|

.00 |

|

|

|||||||||

|

|

|

|

|

|

|

|||||||||||||||

2b. |

Decoupling Modification Addition adjustment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

(Enter code letter(s) from instructions.) |

|

|

|

|

|

|

|

|

2b. |

|

|

|

.00 |

|

|

|||||

|

. . . . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2c. Total Maryland Addition Adjustments to Federal Taxable Income (Add lines 2a and 2b) . |

. . . 2c. |

.00 |

|||||||||||||||||||

|

|

|

|

||||||||||||||||||

SUBTRACTION ADJUSTMENTS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

3a. |

Section |

|

|

|

|

3a. |

|

|

|

.00 |

|

|

|||||||||

|

|

|

|

|

|

|

|||||||||||||||

3b. |

Dividends for domestic corporation claiming foreign tax credits |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

(Federal form 1120/1120C Schedule C line 18) |

|

|

|

|

3b. |

|

|

|

|

.00 |

|

|

||||||||

|

|

|

|

|

|

|

|

||||||||||||||

|

CORPORATION INCOME |

|

2022 |

MARYLAND |

|

|

|

FORM |

|

|

|

500 |

TAX RETURN |

|

page 2 |

NAME |

FEIN |

|

|

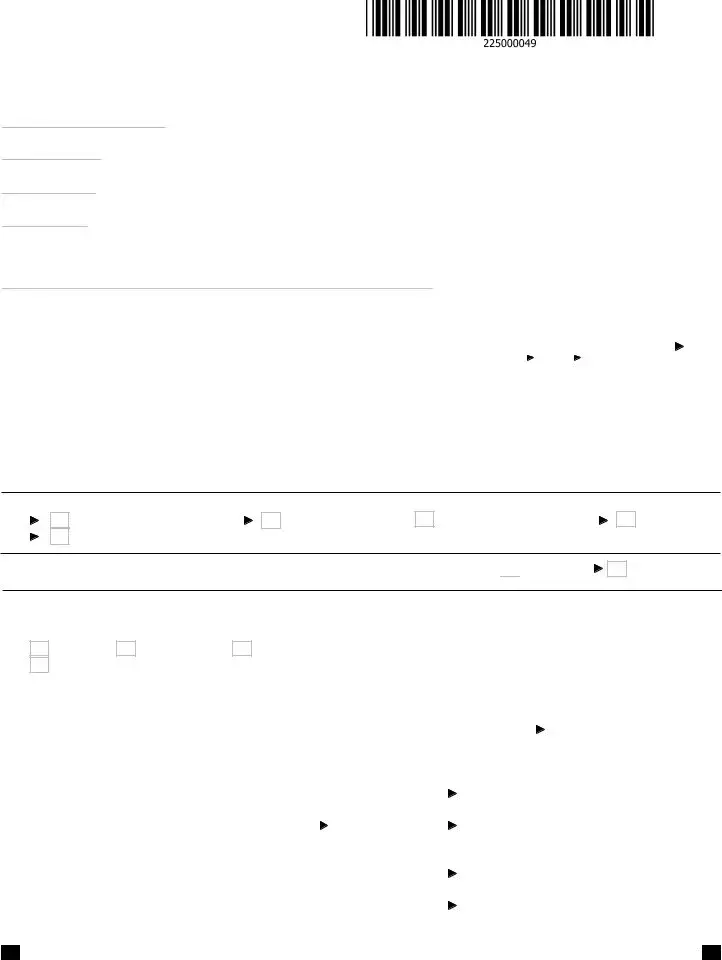

3c. Dividends from related foreign corporations |

|

|

|

(Federal form 1120/1120C Schedule C line 14, 16b and 16c) |

3c. |

.00 |

|

3d. Decoupling Modification Subtraction adjustment |

|

|

|

(Enter code letter(s) from instructions.) |

3d. |

.00 |

|

3e. Total Maryland Subtraction Adjustments to Federal Taxable Income |

|

|

|

(Add lines 3a through 3d.) |

. . . . . . . . . . . 3e. |

.00 |

|

4.Maryland Adjusted Federal Taxable Income before NOL deduction is applied

(Add lines 1c and 2c, and subtract line 3e.) |

4. |

.00 |

5.Enter Adjusted Federal NOL

FDSC |

5. |

.00 |

6.Maryland Adjusted Federal Taxable Income (If line 4 is less than or equal to zero, enter amount from line 4.) (If line 4 is greater than zero, subtract line 5 from line 4 and

|

enter result. If result is less than zero, enter zero.) |

. .6 |

|

|

|

|

.00 |

||||||||||||||

MARYLAND ADDITION MODIFICATIONS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

(All entries must be positive amounts.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

7a. |

State and local income tax |

. 7a. |

.00 |

|

|

|

|||||||||||||||

7b. |

Dividends and interest from another state, local or federal tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

exempt obligation |

. 7b. |

.00 |

|

|

|

|||||||||||||||

7c. |

Net operating loss modification recapture (Do not enter NOL carryover. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

See instructions.) |

. 7c. |

|

.00 |

|

|

|

||||||||||||||

7d. |

Domestic Production Activities Deduction |

. 7d. |

|

.00 |

|

|

|

||||||||||||||

7e. |

Deduction for Dividends paid by captive REIT |

. 7e. |

.00 |

|

|

|

|||||||||||||||

7f. |

Other additions (Enter code letter(s) from |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

instructions and attach schedules) |

|

|

|

|

|

|

|

7f. |

|

.00 |

|

|

|

|||||||

7g. |

Total Addition Modifications (Add lines 7a through 7f) |

. . . . . . 7g. |

.00 |

||||||||||||||||||

MARYLAND SUBTRACTION MODIFICATIONS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

(All entries must be positive amounts.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

8a. |

Income from US Obligations |

. 8a. |

.00 |

|

|

|

|||||||||||||||

8b. |

Other subtractions (Enter code letter(s) from |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

instructions and attach schedule) |

|

|

|

|

|

|

|

8b. |

|

|

.00 |

|

|

|

||||||

|

If you are claiming subtraction H, enter your state medical cannabis business license number: |

|

|

|

|

|

|

||||||||||||||

8c. |

|

|

|

|

|

|

|

|

|

|

|

||||||||||

Total Subtraction Modifications (Add lines 8a and 8b) |

. . . . . . 8c. |

.00 |

|||||||||||||||||||

NET MARYLAND MODIFICATIONS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

9.Total Maryland Modifications (Subtract line 8c from 7g. If less than zero,

enter negative amount.) |

. 9. |

|

.00 |

10. Maryland Modified Income (Add lines 6 and 9.) |

10. |

.00 |

|

|

|

||

APPORTIONMENT OF INCOME

(To be completed by multistate corporations whose apportionment factor is less than 1, otherwise skip to line 13.)

11.Maryland apportionment factor (from page 4 of this form)

|

(If factor is zero, enter .000000.) |

. . . . . . . . . |

11. |

|

|

. |

|

|

|

|

||||

12. |

Maryland apportionment income (Multiply line 10 by line 11.) |

|

. |

12. |

.00 |

|

||||||||

. . . . . . . . . . |

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13. |

Maryland taxable income (from line 10 or line 12, whichever is applicable.) |

|

. |

13. |

.00 |

|

||||||||

. . . . . . . . . . |

|

|

|

|

|

|

|

|

||||||

14. |

Tax (Multiply line 13 by 8.25%.) |

|

. |

14. |

.00 |

|

||||||||

. . . . . . . . . . |

|

|

|

|

|

|

|

|

||||||

15a. |

Estimated tax paid with Form 500D, Form MW506NRS and/or credited |

|

|

|

|

|

|

|

|

|

|

|

||

|

from 2021 overpayment |

15a. |

|

|

.00 |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||||

15b. |

Tax paid with an extension request (Form 500E) |

15b. |

|

|

.00 |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

||||||

15c. |

Nonrefundable business income tax credits from Part AAA. (See instructions for Form 500CR.) |

You must file this form electronically to |

|

|||||||||||

15d. |

Refundable business income tax credits from Part DDD. (See instructions for Form 500CR.) |

claim business tax credits from Form 500CR. |

|

|||||||||||

15e. |

The Heritage Structure Rehabilitation Tax Credit is claimed on line 1 of Part DDD on Form 500CR. |

|

|

|

|

|

|

|

|

|||||

|

Check here |

|

if you are a |

|

|

|

|

|

|

|

|

|

|

|

|

|

MARYLAND |

CORPORATION INCOME |

2022 |

|||

|

|

|

|

|

|

|

|

|

|

FORM |

TAX RETURN |

page 3 |

|||

|

|||||||

500 |

|||||||

NAME |

|

|

FEIN |

|

|

|

|

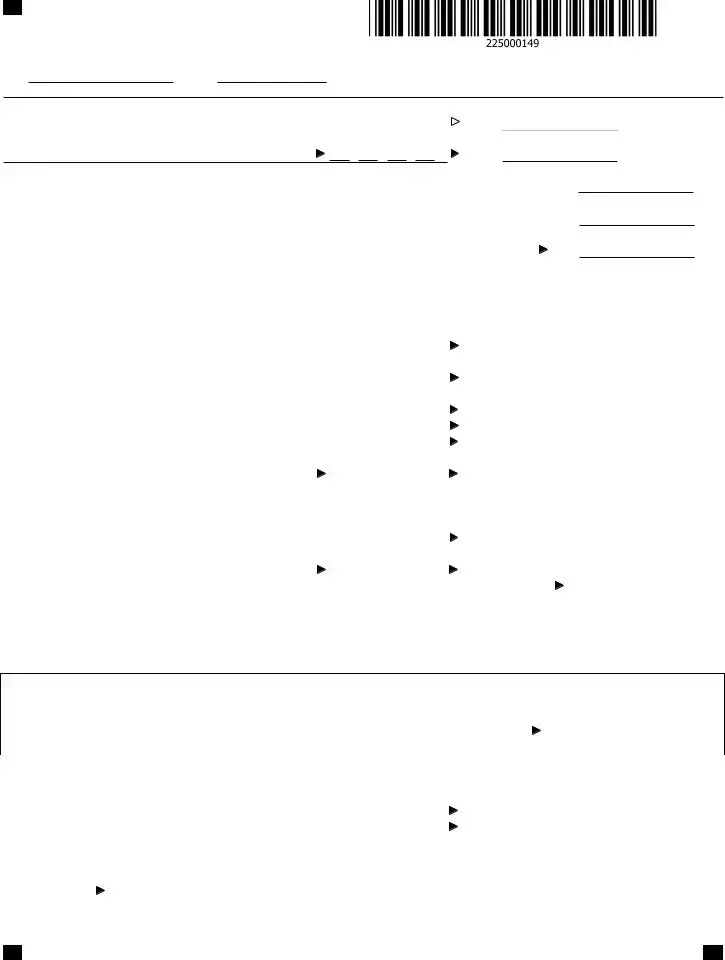

15f. |

Nonresident tax paid on behalf of the corporation by |

|

|

|||||

|

(Attach Maryland Schedule 510/511 |

. . . . . . . . . . . . . . . . . . . . . |

15f. |

|||||

15g. |

If amending, total payments made with original plus additional tax paid |

|

|

|||||

|

after original was filed |

15g. |

||||||

15h. |

Total payments and credits (add lines 15a through 15g) |

. . . . . .15h. |

||||||

16. |

Balance of tax due (If line 14 exceeds line 15h enter the difference.) |

. . . . . 16 |

||||||

17. |

Overpayment (If line 15h exceeds line 14, enter the difference.) |

17. |

||||||

17a. If amending prior overpayment (Total all refunds previously issued.) |

. . . . . |

. . . . . . 17a. |

||||||

18. |

Interest and/or penalty from Form 500UP |

|

|

or late payment interest |

||||

19. |

|

|

for original return. . . . |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . . . 18 |

|||

Total balance due (Add lines 14, 17a and 18. |

Subtract line 15h.) |

. . . . . 19 |

||||||

20.Amount of overpayment from original return to be applied to estimated tax for 2023

(not to exceed the net of lines 17 minus 17a and 18.) . . . . . . . . . . . . . . . . . . . . . . . . . . . .  20.

20.

21.Amount of overpayment TO BE REFUNDED

(Add lines 18 and 20, and subtract the total from line 17.)

(If amending subtract lines 17a and 18 from line 17.). . . . . . . . . . . . . . . . . . . . . . . . . . .  21.

21.

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

DIRECT DEPOSIT OF REFUND (See Instructions.) Verify that all account information is correct and clearly legible. If you are requesting direct deposit of your refund, complete the following.

Check here if you authorize the State of Maryland to issue your refund by direct deposit.

Check here if this refund will go to an account outside of the United States.

22a. Type of account: |

|

Checking |

|

Savings |

22b. Routing Number

22c. Account number:

22d. Name as it appears on the bank account:

INFORMATIONAL PURPOSES ONLY (LINES 23 & 24)

23.NOL generated in Current Year - Carryforward 20 years and carry back 2 years (farming loss ONLY).

(If line 6 is less than zero, enter on line 23.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23.

24.NAM generated in Current Year - Carried Forward/Back with Loss on Line 23 per Section

amount from line 9 on line 24.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24.

FOR USE IF AMENDING THE RETURN

.00

.00

Explanation of Changes to Income, Modifications, Apportionment Factor and Credits. Show the computation in detail and attach schedules as necessary. Check the box or boxes that reflect the reason for filing this amended return and explain in the space

provided below the checkboxes. If more space is needed, you may attach additional pages.

1. Amended to claim a Net Operating Loss Deduction

2. Amended to report a federal adjustment or an RAR (Revenue Agent Report)

3.Amended to claim Business Tax Credit.

4.Amended to claim nonresident PTE Tax Credit

5.Amended to report income omitted on previous filing

6.Amended to change apportionment factor

7.Amended for another reason

Explanation of Changes: ___________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

|

|

MARYLAND |

CORPORATION INCOME |

2022 |

|||

|

|

|

|

|

|

|

|

|

|

FORM |

TAX RETURN |

page 4 |

|||

|

|||||||

500 |

|||||||

NAME |

|

|

FEIN |

|

|

|

|

Schedule A - COMPUTATION OF APPORTIONMENT FACTOR (Applies only to multistate corporations. See instructions.)

|

|

Column 1 |

Column 2 |

|

|

Column 3 |

||

|

NOTE: Rental/leasing companies, financial institutions, |

TOTALS WITHIN |

TOTALS WITHIN |

DECIMAL FACTOR |

||||

|

transportation companies, and worldwide headquartered |

MARYLAND |

AND WITHOUT |

(Column 1 ÷ Column 2 |

||||

|

companies see instructions on Special Apportionment. |

|

MARYLAND |

rounded to six places) |

||||

|

|

|

|

|

|

|

|

|

|

1. Receipts a.Gross receipts or sales less returns and |

|

|

|

|

|

|

|

|

allowances |

.00 |

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b.Dividends |

.00 |

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

c. Interest |

.00 |

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d.Gross rents |

.00 |

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e.Gross royalties |

.00 |

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

f. Capital gain net income |

.00 |

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

g.Other income (Attach schedule.) |

.00 |

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

h.Total receipts (Add lines 1(a) through 1(g), |

|

|

|

|

|

|

|

|

for Columns 1 and 2.) |

.00 |

.00 |

|

|

. |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

Report this factor on line 4 unless you use a special apportionment formula or alternative apportionment formula.

2. Property a.Inventory . . . . . . . . . . . . . . . . . . . . . . .

b.Machinery and equipment . . . . . . . . . . .

c. Buildings . . . . . . . . . . . . . . . . . . . . . . .

d.Land . . . . . . . . . . . . . . . . . . . . . . . . . .

e.Other tangible assets (Attach schedule.) . f. Rent expense capitalized

(multiply by eight) . . . . . . . . . . . . . . . . .

g.Total property (Add lines 2a through 2f, for Columns 1 and 2) . . . . . . . . . . . . . .

3. Payroll a. Compensation of officers . . . . . . . . . . . .

b.Other salaries and wages . . . . . . . . . . . .

c. Total payroll (Add lines 3a and 3b, for Columns 1 and 2.) . . . . . . . . . . . . . . . .

.00 |

.00 |

|

|

.00 |

.00 |

|

|

.00 |

.00 |

|

|

.00 |

.00 |

|

|

.00 |

.00 |

|

|

.00 |

.00 |

|

|

.00 |

.00 |

|

|

.00 |

.00 |

|

|

.00 |

.00 |

|

|

.00 |

.00 |

|

|

.

.

4.Maryland apportionment factor Enter amount from Line 1 Column 3. If an alternative apportionment formula or a special apportionment formula is used, enter the alternative or special apportionment factor here. (If factor is zero, enter .000000 on line 11, page 2.). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

.

Check here if special apportionment or alternative apportionment formula is used.

|

|

MARYLAND |

CORPORATION INCOME |

2022 |

|||

|

|

|

|

|

|

|

|

|

|

FORM |

TAX RETURN |

page 5 |

|||

|

|||||||

500 |

|||||||

NAME |

|

|

FEIN |

|

|

|

|

SCHEDULE B - ADDITIONAL INFORMATION REQUIRED (Attach a separate schedule if more space is necessary.)

1.Telephone number of corporation tax department:

2.Address of principal place of business in Maryland (if other than indicated on page 1):

3.Brief description of operations in Maryland:

4.Has the Internal Revenue Service made adjustments (for a tax year in which a Maryland return

was required) that were not previously reported to the Maryland Revenue Administration Division? . . . . |

|

Yes |

|

No |

||

|

|

|||||

If "yes", indicate tax year(s) here: |

|

and submit an amended return(s) together with a copy of the IRS |

|

|||

adjustment report(s) under separate cover. |

|

|

|

|

|

|

5.Did the corporation file employer withholding tax returns/forms with the Maryland Revenue

6. |

Administration Division for the last calendar year? |

|

Yes |

|

No |

||

Is this entity part of the federal consolidated filing? |

|

Yes |

|

No |

|||

|

If a multistate operation, provide the following: |

|

|

|

|

|

|

7. |

Is this entity a multistate corporation that is a member of a unitary group? |

|

Yes |

|

No |

||

8. |

|

|

|

|

|

|

|

Is this entity a multistate manufacturer with more than 25 employees? |

|

|

Yes |

|

|

No |

|

|

|

|

|

||||

SCHEDULE C - ADDITIONAL INFORMATION REQUIRED (Attach a separate schedule if more space is necessary.)

1.Subtraction for donations of certain disposable diapers, certain hygiene products, and certain monetary gifts. List the name(s) of the qualified charitable entity on the lines below.

MARYLAND |

CORPORATION INCOME |

2022 |

|

|

|

FORM |

TAX RETURN |

page 6 |

500 |

SIGNATURE AND VERIFICATION

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements and to the best of my knowledge and belief it is true, correct and complete. If prepared by a person other than taxpayer, the declaration is based on all information of which the preparer has any knowledge.

Check here

if you authorize your preparer to discuss this return with us.

Officer's signature |

Date |

Officer's Name and Title

Preparer's signature (Required by Law) |

Date |

Printed name of the Preparer / or Firm's name

Street address of preparer or Firm's address

City, State, ZIP Code + 4

Telephone number of preparer |

|

Preparer’s PTIN (Required by Law) |

CODE NUMBERS (3 digits per line)

INCLUDE ALL REQUIRED PAGES OF FORM 500

Make checks payable to and mail to:

Comptroller Of Maryland

Revenue Administration Division

110 Carroll Street

Annapolis, Maryland

(Write Your FEIN On Check Using Blue Or Black Ink.)

File Breakdown

| Fact Name | Description |

|---|---|

| Ink Requirement | The form should be completed using blue or black ink only. |

| Electronic Filing for Business Tax Credits | Business tax credits from Form 500CR must be claimed through electronic filing. |

| Governing Law | The form is governed by Maryland law, specifically the sections and modifications mentioned within its contents, including but not limited to Sections 10-306.1 and 10-205(e). |

| FEIN Requirement | A 9-digit Federal Employer Identification Number (FEIN) is required for filing. |

| Amended Return Provisions | If filing an amended return, specific boxes for reasons such as claiming a Net Operating Loss Deduction or reporting federal adjustments must be checked. |

| Apportionment Factor Calculation | For multistate corporations, income apportionment is calculated according to a specified formula, which may include special requirements for certain types of businesses. |

| Direct Deposit for Refunds | Options for direct deposit of refunds include specifying the type of account and providing routing and account numbers. |

Steps to Filling Out Maryland 500

Filling out the Maryland Form 500, the Corporation Income Tax Return, might feel like navigating through a maze, but fear not. This step-by-step guide is designed to simplify the process, making it accessible and manageable. Upon completion, you will have successfully reported your corporation's income tax details to the state of Maryland—moving one step closer to compliance and peace of mind. Let's dive into the steps:

- Grab a blue or black ink pen to ensure all information is clear and legible on the form.

- Enter your Federal Employer Identification Number (FEIN) in the designated space.

- If applicable, mark the box indicating you've applied for a FEIN and provide the date.

- Fill in the Date of Organization or Incorporation, ensuring the format is MMDDYY.

- Identify and input your Business Activity Code Number, which consists of 6 digits.

- Under the "Check Name" section, provide the current mailing address, including Line 1 for street information and Line 2 for additional details like apartment or suite number. Complete the city, state, and ZIP Code fields.

- Check the appropriate box if it’s an Amended Return, if there's a change in name or address, if you're filing for an Inactive corporation, a First filing, or a Final Return. Additionally, mark if this year's tax period beginning and ending dates are different from last year's due to an acquisition or consolidation.

- If you are Filing to Claim a Net Operating Loss, check whether it’s a Carryback or Carryforward and attach the necessary documentation.

- Enter the Federal Taxable Income on line 1a and Special Deductions on line 1b. Calculate and input your Federal Taxable Income before net operating loss deduction on line 1c.

- Proceed to the Maryland Adjustments section. For Addition and Subtraction Adjustments, fill in the respective amounts in the provided fields.

- Calculate your Maryland Adjusted Federal Taxable Income before NOL deduction and enter this on line 4.

- Report any Adjusted Federal NOL Carry-forward available on line 5.

- Move through the Maryland Addition and Subtraction Modifications sections, accurately filling in each prompted entry.

- Complete the Apportionment of Income section if applicable for multistate corporations.

- Calculate and enter your Maryland Taxable Income, Tax due, and any Estimated Tax Paid or Tax Credits on the subsequent lines as instructed.

- Complete the Direct Deposit of Refund information if you expect a refund and prefer direct deposit.

- If amending the return, provide a detailed Explanation of Changes on the designated section.

- For multistate corporations, accurately fill out Schedule A - Computation of Apportionment Factor, and answer all required questions in Schedule B - Additional Information Required.

- Sign and date the form. If a preparer completed the form on behalf of the corporation, ensure they also sign and provide their information.

- Review the entire form to ensure all information is accurate and complete. Attach a copy of the Federal Income Tax Return through Schedule M2 as instructed on the form.

- Finally, mail the completed form, along with any required payment or additional documentation, to the Comptroller Of Maryland’s address provided on the form. Make sure to write your FEIN on the check if applicable, using blue or black ink.

By following these detailed instructions, you can confidently fill out and submit the Maryland Corporation Income Tax Return, keeping your corporation in good standing with state tax obligations.

More About Maryland 500

What is the Maryland Form 500?

The Maryland Form 500 is a tax return document specifically used by corporations operating in Maryland to report their income, deductions, and taxes owed to the state. It covers various financial aspects, including federal taxable income adjustments, Maryland additions and subtractions, apportionment for multi-state corporations, and tax credits.

Who needs to file Form 500?

Corporations that are active and operating in Maryland are required to file Form 500. This includes corporations that have undergone changes like acquisition or consolidation, are claiming net operating losses, or are filing for the first time. Inactive corporations must also file if they are registered in Maryland.

Is digital submission of Form 500 required?

Yes, corporations must file this form electronically to claim business tax credits from Form 500CR. Electronic filing also ensures faster processing of the return and any associated refunds.

What should be attached with Form 500?

Along with Form 500, corporations must attach a copy of their federal income tax return up to Schedule M2. If filing to claim a net operating loss, copies of the federal form for the loss year and Form 1139 should be attached as well.

How do corporations claim net operating losses on Form 500?

To claim a net operating loss, corporations must check the appropriate box (Carryback or Carryforward) on Form 500 and attach the necessary documentation. This documents the loss year and substantiates the carryback or carryforward claim.

What are the key sections in Form 500?

- Maryland Adjustments: Alterations to federal taxable income either through addition or subtraction adjustments. This section recalibrates the federal income to reflect specific state tax codes.

- Apportionment of Income: Necessary for multi-state corporations to determine the portion of income attributable to Maryland, based on an apportionment factor.

- Tax Calculations and Credits: After adjustments and apportionment, this section computes the tax owed and subtracts any payments or credits to determine the final tax liability or refund.

Can changes in the corporation's information be reported on Form 500?

Yes, corporations should indicate any changes in name or address on Form 500. This ensures that the Maryland Revenue Administration Division has the most current information.

What if a corporation needs to amend a previously filed Form 500?

To amend a previously filed Form 500, the corporation must check the "Amended Return" box and explain the reasons for amendment in the specified section. Detailed computations and attached schedules are necessary to support the changes made.

What options are available for refunds?

Corporations can request their refunds to be directly deposited into a checking or savings account. They must provide the type of account, routing number, account number, and account name as it appears on the bank account.

Common mistakes

When filling out the Maryland Corporation Income Tax Return (Form 500), individuals often encounter a variety of common errors. These mistakes can lead to processing delays, questions from the Maryland Revenue Administration Division, and in some cases, adjustments that may affect the tax liability of the corporation. It is crucial for filers to understand and avoid these pitfalls to ensure accurate and timely processing of their tax returns. Here is a list of eight common mistakes made while filling out the Maryland 500 form:

-

Using incorrect ink: The Maryland 500 form instructions specify that the form should be filled out using blue or black ink only. Using other colors can cause issues with the scanning of the documents.

-

Not reporting the Federal Employer Identification Number (FEIN) correctly: Each corporation must provide its nine-digit FEIN. Omitting or inaccurately reporting this number can result in processing errors.

-

Failure to check applicable boxes for special filing situations such as the amended return, inactive corporation, first filing, or final return, which can lead to misclassification of the filing status.

-

Omitting the date of organization or incorporation: This date is crucial for identifying the tax period and the eligibility for certain tax treatments.

-

Incorrectly reporting the business activity code number: The six-digit business activity code helps in identifying the primary business activity of the corporation, and using an incorrect code can lead to incorrect tax assessments.

-

Not attaching a copy of the federal income tax return and Schedule M-2, which are necessary for validating the income and deductions reported on the Maryland tax return.

-

Miscalculation of Maryland adjustments to federal taxable income: Both addition and subtraction adjustments must be accurate to determine the correct tax base.

-

Forgetting to sign and date the form: An unsigned or undated tax return is considered incomplete and can lead to its rejection.

Ensuring that these common mistakes are avoided will help in the smooth processing of the Maryland 500 form. Paying careful attention to the details and double-checking the entries can prevent unnecessary delays and ensure compliance with Maryland tax laws.

Documents used along the form

When businesses engage with the tax system in Maryland, particularly for filing the Maryland Corporation Income Tax Return (Form 500), they frequently need to incorporate additional documentation to fulfill regulatory requirements or provide supplementary information about their financial status. Understanding these forms and documents is crucial for ensuring compliance and optimizing tax management.

- Form 500CR: This is often used in conjunction with Form 500 to claim various business income tax credits. Businesses can benefit from credits such as job creation, research and development, and investments in Maryland. Detailed information including the credit amount and eligibility criteria must be accurately reported.

- Form 500D: Designed for making estimated tax payments, this form is essential for corporations that expect to owe $1,000 or more in taxes for the year. Using Form 500D helps businesses manage their cash flow by spreading tax payments throughout the year, rather than paying a lump sum.

- Form 500E: When corporations cannot file their tax return by the due date, they use Form 500E to request an extension of time to file. Submitting this form helps avoid penalties related to late filings. However, it's important to note that this is an extension to file, not to pay any taxes due.

- Schedule K-1 (Form 510): This schedule is relevant for shareholders of S Corporations or partners in partnerships. It outlines the shareholder's or partner's share of income, deductions, credits, etc. Companies must provide a Schedule K-1 to ensure their shareholders or partners can accurately report individual income on their personal tax returns.

- Form 500UP: Utilized for calculating underpayment of estimated tax by corporations. If businesses did not pay enough tax throughout the year through withholding or estimated tax payments, Form 500UP helps determine any underpayment penalties owed.

Successfully navigating the complexities of corporate tax obligations in Maryland typically involves preparing and submitting a combination of these forms and documents. Corporations should carefully review each document's requirements to ensure accurate and complete submissions, thereby minimizing the risk of errors and penalties. Staying informed about both federal and state tax obligations is essential for maintaining compliance and leveraging potential tax benefits.

Similar forms

The Maryland Form 500 is designed for corporations to file their income tax returns, quite similar in purpose and structure to the federal Form 1120 and Form 1120S.

Form 1120 is the U.S. Corporation Income Tax Return, filed by C corporations to report their income, gains, losses, deductions, and credits to the Internal Revenue Service (IRS). Like the Maryland 500 form, it captures the corporation's financial status over the fiscal year and calculates the income tax payable to the federal government. Both forms include sections for reporting federal taxable income, special deductions, and tax payments. However, the Maryland 500 form also includes adjustments specific to state tax laws, including addition and subtraction modifications related to Maryland's tax code.

Form 1120S is used by S corporations for federal tax purposes. While S corporations pass their corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes, they must still file Form 1120S to report their annual financial information. This form, like the Maryland 500, includes areas for income reporting, various deductions, and tax computations. However, the purpose shifts slightly due to the flow-through nature of taxes for S corporations at the federal level, contrasted with the direct taxation on the corporate level in Maryland’s Form 500. Notably, Maryland S corporations use a different form (Form 510) for state filings, underscoring the tailored approach states can take versus federal requirements.

Dos and Don'ts

When completing the Maryland 500 form for your corporation, ensure accuracy and compliance by following these guidelines:

- Do use blue or black ink if filling out the form by hand to ensure the information is legible and scans correctly.

- Don't use any other ink colors as they may not be accepted and could lead to processing errors.

- Do provide your Federal Employer Identification Number (FEIN) accurately to avoid any mismatches with federal records.

- Don't overlook the date of organization or incorporation, as this information is crucial for identifying the tax obligations of your corporation correctly.

- Do check the appropriate box if filing an amended return, claiming a net operating loss, or if there are any changes in name or address to ensure the form is processed correctly.

- Don't guess on the business activity code; ensure you have the correct six-digit code that reflects your primary business activity.

- Do attach a copy of your federal income tax return as required, ensuring that all included schedules are complete and accurate.

- Don't fabricate or omit information regarding your income, deductions, and credits. Inaccuracies can lead to audits, penalties, or legal actions.

- Do make sure to calculate and report Maryland adjustments to your federal taxable income accurately, following the instructions for addition and subtraction adjustments.

- Don't forget to sign and date the form. An unsigned form is not valid and will not be processed, potentially leading to delays and penalties.

Adhering to these guidelines will help ensure that your Maryland 500 form is completed correctly and processed efficiently, minimizing the risk of errors or delays.

Misconceptions

When it comes to understanding the Maryland Corporation Income Tax Return (Form 500), there are several common misconceptions that can lead to confusion for businesses operating within the state. Here are six misconceptions and their clarifications:

- Only corporations need to file Form 500: While it is true that Form 500 is designed for corporations, it's also required for other entities that are treated as corporations for federal tax purposes. This includes certain business trusts and other structures that might not traditionally be considered corporations.

- Income reported is based solely on Maryland operations: Actually, Form 500 requires entities to report their total income, not just the income generated within Maryland. However, an apportionment factor is used to determine the portion of income subject to Maryland tax, which considers the entity's operations within and outside of Maryland.

- No need to file if no tax is due: This is incorrect. Even if no tax is due, corporations operating in Maryland are required to file Form 500. This is necessary to maintain accurate records with the Maryland tax authorities and avoid potential penalties for non-filing.

- Form 500 is only for income tax purposes: While income tax is a significant component, Form 500 also addresses other tax considerations, such as the need to report adjustments to federal taxable income specific to Maryland law and to claim certain state-specific tax credits.

- Electronic filing is optional: Corporations are required to file this form electronically in order to claim business tax credits from Form 500CR. This encourages faster processing and supports the state's efforts to maintain accurate and timely tax records.

- Amendments can only be made for correction of errors: Amendments to a previously filed Form 500 can be made for several reasons, including claiming a Net Operating Loss Deduction, reporting a federal adjustment, claiming additional business tax credits, or changing the apportionment factor. This allows businesses to correct or update their tax information beyond simple errors.

It's essential for entities operating in Maryland to understand these aspects of Form 500 to comply with state tax laws and avoid possible misunderstandings or penalties associated with the filing process.

Key takeaways

When approaching the Maryland Corporation Income Tax Return (Form 500) for the year 2020 or any fiscal year, attention to detail and thorough understanding of the guidelines can ensure accuracy and compliance. Here are eight key takeaways to guide you:

- Use either blue or black ink only to complete the Form 500, ensuring that all printed information is legible and adheres to the submission standards.

- If there have been any changes to your corporation's name or address, or if it's the first filing for the corporation, make sure to indicate these changes clearly on the form.

- The form requires the Federal Employer Identification Number (FEIN) for verification and tracking. If the FEIN has been applied for but not received by the filing date, note the application date in the designated space.

- It's important to attach a copy of the federal income tax return through Schedule M-2, as this provides necessary context and foundational figures required for completing Form 500.

- For corporations filing to claim a net operating loss, selection of either the 'carryback' or 'carryforward' option must be made, and relevant documentation attached, to accurately process this aspect of the return.

- Certain modifications to Federal Taxable Income specific to Maryland law must be made using the designated addition and subtraction adjustments sections. These adjustments might include related party transactions, state-specific tax credits, or deductions not recognized at the federal level.

- Ensure direct deposit information is accurate and clearly specified to expedite any potential refunds. This includes specifying the type of account, routing number, account number, and the name on the account as per banking regulations.

- If amending a previously filed return, the Form 500 requires detailed explanation of the changes being made, whether it's to claim additional credits, to report adjustments following an IRS adjustment, or to correct errors from the prior filing. Supporting schedules may be attached as needed for comprehensive documentation.

By following these key points and consulting the detailed instructions provided with the form, corporations can navigate the complexities of Maryland's Corporation Income Tax Return effectively.

Common PDF Templates

Maryland Lottery Winner Anonymous - An application form designed to assess the suitability of businesses looking to offer lottery games in Maryland.

Maryland Concealed Carry Law Change - The form includes sections to detail the type of handgun used during qualification: revolver or semi-automatic.