Maryland 500D PDF Template

In an effort to comply with tax obligations, corporations operating within Maryland are required to estimate and remit their income tax payments periodically through the year. This process is facilitated by Maryland Form 500D, a critical document introduced for the first time in its revised edition of 1996, aimed at streamlining the submission of estimated corporate income tax. This form is specifically designed for use in situations where the preprinted vouchers, which are part of the Declaration of Estimated Corporation Income Tax Packet, are not available to the corporation. It serves as a vehicle for declaring and remitting estimated taxes due at various intervals of the fiscal year, ensuring that corporations can fulfill their tax obligations even in the absence of the standard packet. Form 500D is accompanied by detailed instructions on its reverse side, guiding corporations through the process of accurately calculating and submitting their estimated taxes. It highlights the importance of making these payments on time to avoid potential penalties and interest accruals for late submissions. Additionally, the form provides a space for corporations to request replacement vouchers if needed for the remaining installments of the current tax year, emphasizing the flexibility and adaptability of Maryland's approach to corporate tax compliance. By adhering to the specific requirements outlined in Form 500D, corporations can effectively manage their estimated tax payments, contributing to the seamless operation of Maryland's tax collection system.

Maryland 500D Sample

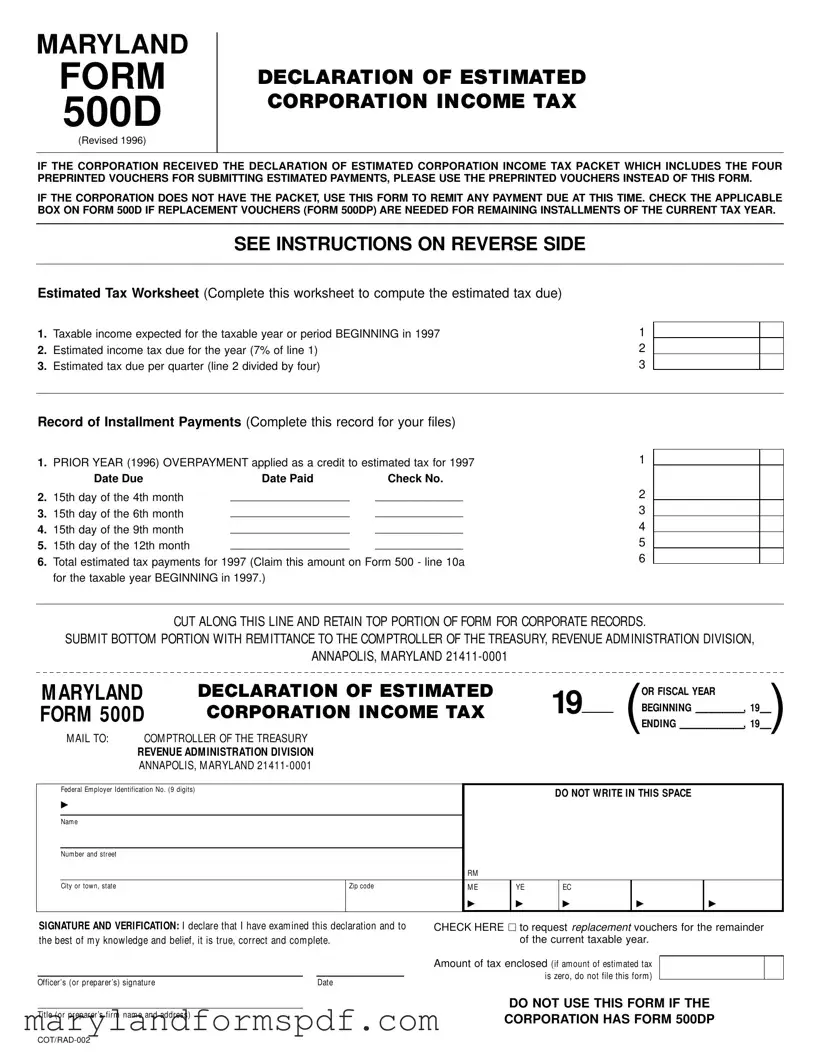

MARYLAND

FORM

500D

(Revised 1996)

DECLARATION OF ESTIMATED CORPORATION INCOME TAX

IF THE CORPORATION RECEIVED THE DECLARATION OF ESTIMATED CORPORATION INCOME TAX PACKET WHICH INCLUDES THE FOUR PREPRINTED VOUCHERS FOR SUBMITTING ESTIMATED PAYMENTS, PLEASE USE THE PREPRINTED VOUCHERS INSTEAD OF THIS FORM.

IF THE CORPORATION DOES NOT HAVE THE PACKET, USE THIS FORM TO REMIT ANY PAYMENT DUE AT THIS TIME. CHECK THE APPLICABLE BOX ON FORM 500D IF REPLACEMENT VOUCHERS (FORM 500DP) ARE NEEDED FOR REMAINING INSTALLMENTS OF THE CURRENT TAX YEAR.

SEE INSTRUCTIONS ON REVERSE SIDE

Estimated Tax Worksheet (Complete this worksheet to compute the estimated tax due)

1. |

Taxable income expected for the taxable year or period BEGINNING in 1997 |

1 |

|

|

|

|

|||

2. |

Estimated income tax due for the year (7% of line 1) |

2 |

|

|

|

|

|||

3. |

Estimated tax due per quarter (line 2 divided by four) |

3 |

|

|

|

|

|||

|

|

|

|

|

Record of Installment Payments (Complete this record for your files)

1. |

PRIOR YEAR (1996) OVERPAYMENT applied as a credit to estimated tax for 1997 |

1 |

||

|

||||

|

Date Due |

Date Paid |

Check No. |

|

2. |

15th day of the 4th month |

___________________ |

______________ |

2 |

3. |

15th day of the 6th month |

___________________ |

______________ |

3 |

4. |

15th day of the 9th month |

___________________ |

______________ |

4 |

5. |

15th day of the 12th month |

___________________ |

______________ |

5 |

6. |

Total estimated tax payments for 1997 (Claim this amount on Form 500 - line 10a |

6 |

||

|

||||

for the taxable year BEGINNING in 1997.)

CUT ALONG THIS LINE AND RETAIN TOP PORTION OF FORM FOR CORPORATE RECORDS.

SUBMIT BOTTOM PORTION WITH REMITTANCE TO THE COMPTROLLER OF THE TREASURY, REVENUE ADMINISTRATION DIVISION,

ANNAPOLIS, MARYLAND

M ARYLAND |

DECLARATION OF ESTIMATED |

|

|

|

|

|

OR FISCAL YEAR |

|

|

||||

FORM 500D |

CORPORATION INCOME TAX |

|

19 |

|

(ENDINGBEGINNING_____________________,, |

1919____) |

|||||||

|

|

||||||||||||

|

M AIL TO: COM PTROLLER OF THE TREASURY |

|

|

|

|

|

|

|

|

|

|

||

|

REVENUE ADM INISTRATION DIVISION |

|

|

|

|

|

|

|

|

|

|

||

|

ANNAPOLIS, M ARYLAND |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Federal Em ployer Identification No. (9 digits) |

|

|

|

|

DO NOT WRITE IN THIS SPACE |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|||||

|

▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nam e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Num ber and street |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RM |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or tow n, state |

|

Zip code |

M E |

YE |

|

EC |

|

|

|

|

|

|

|

|

|

|

▶ |

▶ |

|

▶ |

|

▶ |

▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SIGNATURE AND VERIFICATION: I declare that I have exam ined this declaration and to the best of m y knowledge and belief, it is true, correct and com plete.

Officer’s (or preparer’s) signature |

Date |

CHECK HERE □ to request replacement vouchers for the remainder of the current taxable year.

Amount of tax enclosed (if am ount of estim ated tax is zero, do not file this form )

Title (or preparer’s firm nam e and address)

DO NOT USE THIS FORM IF THE CORPORATION HAS FORM 500DP

INSTRUCTIONS FOR MARYLAND FORM 500D (Revised 1996)

DECLARATION OF ESTIMATED CORPORATION INCOME TAX

GENERAL INSTRUCTIONS

Purpose of Form Form 500D is used by a corporation to declare and remit estimated income tax when the preprinted Form 500DP is unavailable.

Corporations expected to be subject to estimated tax require- ments should have received a Declaration of Estimated Corporation Income Tax Packet. The estimated tax packet includes a work- sheet, record of payments, four preprinted vouchers (Form 500DP) and instructions. Please use the Form 500DP which contains pre- printed taxpayer information and provides for prompt and accurate processing of the declaration payment.

If the corporation does not have the estimated tax packet, use Form 500D to remit any payment due.

NOTE: Do not use this form for

General Requirements Every corporation having Maryland taxable income which will develop a tax in excess of $1,000 for the taxable year or period must make estimated income tax pay- ments. The total estimated tax payments for the year must be at least 90% of the tax developed for the current taxable year or 100% of the tax developed for the prior tax year. At least 25% of the total estimated tax must be remitted by each of the four installment due dates.

In the case of a short tax period the total estimated tax required is the same as for a regular taxable year, 90% of the tax developed for the current (short) taxable year or 100% of the tax developed for the prior tax year. The minimum estimated tax for each of the installment due dates is the total estimated tax required divided by the number of installment due dates occurring during the short tax year.

Maryland law provides for the accrual of interest and imposition of penalty for failure to pay any tax when due.

If it is necessary to amend the estimated, recalculate the amount of estimated tax required using the estimated tax worksheet provided on this form. Adjust the amount of the next installment to reflect any previous underpayment or overpayment. The remaining installments must be at least 25% of the amended estimated tax due for the year.

Consolidated returns are not allowed under Maryland law. Affiliated corporations which file a consolidated federal return must file separate Maryland declarations for each member corporation.

When and Where to File File Form 500D on or before the 15th day of the 4th, 6th, 9th and 12th months following the beginning

of the taxable year or period. In addition to payment with Form 500DP or 500D, the corporation may partially or fully apply any overpayment from the prior year Form 500 – Corporation Income Tax Return to the estimated tax obligation for this year.

The estimated tax must be filed with the Comptroller of the Treasury, Revenue Administration Division, Annapolis, Maryland

SPECIFIC INSTRUCTIONS

Name, Address and Other Information Type or print the required information in the designated area. DO NOT USE THE LABEL FROM THE TAX BOOKLET COVER.

Enter the name exactly as specified in the Articles of Incorpo- ration, or as amended, and continue with any “Trading As” (T/A) name if applicable.

Enter the Federal Employer Identification Number (FEIN). If the FEIN has not been secured, enter “APPLIED FOR” followed by the date of application. If a FEIN has not been applied for, do so immediately.

Check the box to request replacement vouchers for the remainder of the current taxable year. Do not check the box to request vouchers for the next taxable year; a packet including vouchers will be issued automatically.

Taxable Year or Period ENTER THE BEGINNING AND END-

ING DATES OF THE TAXABLE YEAR IN THE SPACE PROVIDED ON FORM 500D.

The same taxable year or period used for the federal return must be used for Form 500D.

Amount of Tax Enclosed Enter the amount of tax due in the space provided and remit full payment with this form.

Signature and Verification An authorized officer or the paid preparer must sign and date Form 500D indicating the corporate title or preparer firm name and address.

Payment Instructions Include a check or money order made payable to the Comptroller of the Treasury for the full amount due. All payments must indicate the Federal Employer Identification Number, type of tax and tax year beginning and ending dates.

DO NOT SEND CASH.

Mailing Instructions Use the envelope provided in the tax booklet and place an “X” in the appropriate box in the lower left corner to indicate the type of document enclosed. Also, be sure to read and follow the reminders listed on the back of the envelope.

File Breakdown

| Fact | Detail |

|---|---|

| Form Name and Revision Year | Maryland Form 500D, Revised 1996 |

| Purpose | Used by corporations to declare and remit estimated income tax when preprinted Form 500DP is unavailable |

| Who Should Use | Corporations expecting to owe more than $1,000 in Maryland state income tax for the year |

| Estimated Tax Calculation | Must be at least 90% of the tax for the current year or 100% of the tax for the prior year, divided into at least four installments |

| Usage Restrictions | Not applicable for pass-through entities like S corporations, or for remitting employer withholding tax |

| Amendments | If estimated tax needs adjustment, recalculate and adjust future installments accordingly |

| Consolidated Returns | Not allowed under Maryland law; affiliated corporations filing a consolidated federal return must file separate Maryland declarations |

| Filing and Payment Deadlines | Due on the 15th day of the 4th, 6th, 9th, and 12th months of the taxable year |

Steps to Filling Out Maryland 500D

Filling out the Maryland Form 500D for estimated corporation income tax is an important step for corporations in Maryland that need to declare their taxes without the preprinted Form 500DP. This straightforward process ensures that your corporation remains compliant with state tax obligations. Below are the detailed steps to complete and submit the form correctly.

- Gather necessary financial documents that detail your corporation's expected taxable income for the year.

- Calculate the estimated income tax due based on 7% of your expected taxable income.

- Divide the estimated annual tax due by four to determine the estimated tax due per quarter.

- Complete the "Estimated Tax Worksheet" on the form with your calculated amounts.

- Proceed to fill out the "Record of Installment Payments" section for your records. Include any overpayment from the prior year that you wish to apply to the current year's estimated tax.

- Type or print the corporation's name as it appears in your Articles of Incorporation, including any trading names (T/A) if applicable.

- Enter your Federal Employer Identification Number (FEIN). If you have applied for but not yet received your FEIN, indicate "APPLIED FOR" and the application date.

- If you need replacement vouchers for the remaining installments of the current tax year, check the designated box on the form.

- Fill in the taxable year or period at the top of the form, making sure it matches the period used for your federal return.

- Enter the amount of tax you are enclosing with this submission in the designated space.

- An authorized officer or the paid preparer of the corporation must sign and date the form, indicating their corporate title or preparer firm name and address.

- Prepare a check or money order for the full amount due, payable to the Comptroller of the Treasury. Include your FEIN, type of tax, and the beginning and ending dates of the tax year on your payment.

- Mail the completed form and payment to the Comptroller of the Treasury, Revenue Administration Division, Annapolis, Maryland 21411-0001, using the envelope provided in the tax booklet. Ensure to mark the appropriate type of document in the lower left corner of the envelope.

After submitting Form 500D, your corporation should monitor its income and expenses closely throughout the year. This vigilance will help in preparing for the next quarterly estimated payment or any necessary adjustments to the estimated tax. Accurate and timely filing supports the financial health and compliance of your corporation.

More About Maryland 500D

What is the purpose of Maryland Form 500D?

Form 500D is designed for corporations to declare and remit estimated income tax in Maryland. This form steps in when the preprinted Form 500DP, which includes preprinted taxpayer information for estimated tax payments, is unavailable. Its primary use is to ensure corporations accurately estimate and pay their income tax during the year if they expect to owe $1,000 or more. The form facilitates proper planning and payment, helping corporations avoid underpayment penalties and interest charges.

Who is required to file Form 500D?

Any corporation that expects to have Maryland taxable income resulting in a tax due exceeding $1,000 for a taxable year or period must complete Form 500D to make estimated tax payments. It's important to note that this form is not applicable to pass-through entities such as S corporations or for remitting employer withholding tax.

How is the estimated tax calculated and paid?

The estimated tax payment is calculated based on the corporation's expected taxable income for the year. The following steps guide you through this calculation:

- Determine the taxable income expected for the year.

- Calculate the estimated income tax due for the year, which is 7% of the expected taxable income.

- Divide this amount by four to determine the estimated tax due per quarter.

When are Form 500D payments due?

Payments are due on the 15th day of the 4th, 6th, 9th, and 12th months following the beginning of the taxable year or period. These deadlines ensure that the corporation remains compliant throughout the year by spreading their tax liability across evenly spaced installments.

Where should Form 500D be submitted?

Completed Form 500D and the accompanying payment should be sent to the Comptroller of the Treasury, Revenue Administration Division, in Annapolis, Maryland. This submission ensures proper processing and recording of your estimated tax payments, maintaining the corporation's good standing with Maryland tax laws.

What should you do if you need to amend a previously filed Form 500D?

If amendments to a previously filed Form 500D are necessary, the corporation should recalculate the estimated tax using the worksheet provided on the form. Any adjustments for overpayments or underpayments are then reflected in the subsequent installment. This recalibration ensures the total estimated tax for the year accurately reflects the corporation's financial situation, adjusting for any deviations from initial projections.

Common mistakes

Filling out the Maryland Form 500D, the Declaration of Estimated Corporation Income Tax, can sometimes be tricky. Below are seven common mistakes that should be avoided to ensure accurate and timely processing:

- Not using the preprinted vouchers provided in the Declaration of Estimated Corporation Income Tax Packet when available. These vouchers contain preprinted information that helps facilitate prompt and accurate processing.

- Incorrectly calculating the estimated tax due by either overestimating or underestimating the corporation's taxable income expected for the taxable year. This impacts line 2 (Estimated income tax due for the year) and line 3 (Estimated tax due per quarter).

- Failing to request replacement vouchers for the remaining installments of the current tax year by not checking the applicable box on Form 500D when necessary.

- Not applying prior-year overpayment correctly to the estimated tax for the current year or not keeping accurate records of installment payments, which can lead to discrepancies in the record of installment payments section.

- Incorrectly entering the Federal Employer Identification Number (FEIN), or neglecting to enter it if it hasn't been secured yet. If "APPLIED FOR" and the application date should be noted in its absence.

- Misunderstanding the due dates for filing Form 500D and making installment payments, which are the 15th day of the 4th, 6th, 9th, and 12th months following the beginning of the taxable year.

- Incorrectly filling out the name, address, and other information section by either using the label from the tax booklet cover or not entering the corporate name as specified in the Articles of Incorporation.

To avoid these errors, it's important to thoroughly review the instructions provided with Form 500D and ensure all information is complete, accurate, and submitted on time.

Documents used along the form

When businesses complete the Maryland Form 500D for declaring and remitting estimated corporation income tax, there are other forms and documents they might also need. These documents help in different aspects of tax and financial management for a corporation operating in Maryland. Below is a list and brief description of each:

- Form 500 - Maryland Corporation Income Tax Return: This is the annual tax return document for corporations. After estimating taxes using Form 500D, Form 500 helps in reporting the actual income and calculating the precise tax liability for the year.

- Form 500DP - Declaration of Estimated Corporation Income Tax Payment Vouchers: These preprinted vouchers are for corporations to submit their estimated tax payments. If a corporation doesn't have this form, Form 500D is used instead.

- Form MW506NRS - Maryland Nonresident Sale of Real Estate: Relevant for corporations that deal with real estate, particularly when selling property owned by nonresidents of Maryland.

- Form 1 - Annual Report and Personal Property Tax Return: Required by the Maryland Department of Assessments and Taxation for most businesses to report personal property and for annual registration.

- Form 505 - Nonresident Income Tax Return: Corporations with income from Maryland sources but based elsewhere file this form to report and pay income tax on their Maryland-sourced gains.

- Form RAD-102 - Request for Copy of Tax Form: If a corporation needs a copy of previously filed tax forms, this request form is necessary.

- Form MW506 - Employer's Return of Income Tax Withheld: This form is for reporting and remitting income taxes withheld from employees' wages.

Understanding each document and its purpose within the broader context of a corporation's financial and tax reporting obligations in Maryland is crucial. These forms often interconnect, ensuring corporations meet their full reporting requirements and maintain compliance with Maryland tax law.

Similar forms

The Maryland 500D form is similar to other documents used for estimating and paying taxes in advance. These forms share a common goal: to help entities calculate and remit their taxes before the end of the fiscal period. By comparing these documents, it becomes clear how they function within the broader tax framework, each serving specific types of taxpayers or entities.

Form 1040-ES, "Estimated Tax for Individuals" is one such document. It is used by individuals, rather than corporations, to calculate and pay their estimated tax to the IRS. The similarity lies in the purpose of both forms: to allow taxpayers to estimate their tax liability and make payments in advance, based on their expected income for the year. However, while the Maryland 500D form is specifically for corporations operating within Maryland, Form 1040-ES is for individual taxpayers on a federal level. Both forms require the calculation of estimated income, the application of the appropriate tax rates, and the payment of estimated tax in installments. The key difference relates to the taxpayer type (individuals vs. corporations) and the jurisdiction (federal vs. state).

Form 1120-W, "Estimated Tax for Corporations" is more directly comparable to the Maryland 500D form. Both are designed for corporations, but Form 1120-W is used for federal tax purposes. Like the Maryland 500D, it helps corporations estimate their tax liability and make quarterly payments. Both forms include instructions for calculating estimated tax based on expected annual income, applying the correct tax rate, and dividing the total estimated tax into installment payments. The parallel between them underscores the unified approach to tax planning and compliance for corporations, differing mainly in their application at the state versus the federal level.

In essence, while the Maryland 500D form serves a specific segment of taxpayers within a particular jurisdiction, it shares a foundational purpose with forms like the 1040-ES and 1120-W. These documents facilitate the advance payment of taxes based on estimated earnings, mirroring the structure and intent across different taxpayer categories and levels of government. Their existence simplifies the process of tax compliance, ensuring that taxpayers can manage their tax obligations efficiently and effectively.

Dos and Don'ts

When preparing to fill out the Maryland 500D form for declaring estimated corporation income tax, there are several key practices to keep in mind to ensure that the process is done accurately and efficiently. Below are seven do's and don'ts:

- Do ensure that the corporation does not have the preprinted vouchers (Form 500DP) before using Form 500D, as the preprinted vouchers contain taxpayer information that facilitates prompt and accurate processing.

- Do not use this form for pass-through entities, including S corporations, or to remit employer withholding tax, as it is not intended for these purposes.

- Do make sure to calculate the estimated tax payments accurately, ensuring that they meet at least 90% of the tax for the current taxable year or 100% of the tax for the prior tax year to avoid penalties.

- Do not neglect the installment due dates. At least 25% of the total estimated tax must be remitted by each of the due dates to comply with Maryland law.

- Do use the estimated tax worksheet provided on the form to compute the estimated tax due accurately, adjusting for any overpayment or underpayment from previous installments as necessary.

- Do not check the box to request replacement vouchers without ensuring that you do indeed need them for the remaining installments of the current tax year, to avoid unnecessary requests.

- Do type or print the corporation's information clearly and accurately, including the Federal Employer Identification Number (FEIN) and the taxable year or period, to avoid processing delays or errors.

Adhering to these guidelines will help ensure that your Maryland 500D form is filled out correctly and submitted on time, thereby fulfilling your corporation's tax obligations effectively.

Misconceptions

Understanding the nuances of Form 500D for Maryland's Declaration of Estimated Corporation Income Tax can sometimes lead to confusion. Here are six common misconceptions about this important document and the clarifications that aim to demystify these misunderstandings:

- Only corporations with profit must file: It's a common belief that only corporations expecting to make a profit need to file Form 500D. However, any corporation with Maryland taxable income that will result in more than $1,000 of tax for the year is required to make estimated tax payments, regardless of their profit margins.

- You can use last year’s packet without updates: Some think if they have last year's packet, they don't need to use the updated Form 500D. While previous packets provide a useful guide, tax rates, allowances, and other important figures can change from year to year. It's crucial to use the updated form or ensure that any preprinted vouchers reflect current tax year information.

- Consolidated returns are acceptable: A significant misunderstanding is that consolidated returns are an option for affiliated corporations in Maryland. Maryland law expressly prohibits consolidated returns for state income tax purposes, requiring affiliated corporations that file a consolidated federal return to file separate declarations in Maryland.

- Overpayments always roll forward: Some believe that any overpayment from the previous year automatically rolls forward as a credit against the next year’s estimated tax. Corporations have the option to apply prior year overpayments to the estimated tax of the current year, but this is not automatic and needs to be specified.

- All corporations must pay quarterly: Another common misconception is that all corporations must adhere to a quarterly payment schedule. While Form 500D delineates a quarterly payment structure, the amount and frequency of payments may vary based on the corporation’s tax situation, and in the case of a short tax year, the schedule adjusts accordingly.

- Online payments aren’t allowed: There's a false belief that payments related to Form 500D can only be made via mail. However, the Maryland Comptroller’s Office encourages electronic payments for ease and efficiency. Corporations should verify current electronic payment options to ensure compliance and expedite processing.

Dispelling these misconceptions about the Maryland Form 500D can help corporations comply with state tax obligations effectively. Accurate knowledge empowers businesses to manage their financial responsibilities with confidence and avoid potential pitfalls related to misinterpretation of tax requirements.

Key takeaways

Filing the Maryland Form 500D is crucial for corporations operating within the state to comply with estimated income tax payments when preprinted vouchers are not available. Here are key takeaways to ensure successful compliance:

- The Maryland Form 500D is designed for corporations to declare and pay estimated income taxes in situations where the preprinted Form 500DP is unavailable.

- If a corporation expects to owe more than $1,000 in Maryland state income tax for the year, they must make estimated tax payments to meet the state’s minimum requirements.

- Payments must be at least 90% of the tax for the current year or 100% of the prior year’s tax to avoid penalties.

- Estimated tax payments are split into four installments, each comprising at least 25% of the total estimated taxes for the year, due on the 15th day of the 4th, 6th, 9th, and 12th months of the taxable period.

- When filling out Form 500D, corporations should accurately enter their Federal Employer Identification Number (FEIN), name as per the Articles of Incorporation or as amended, and check the box if replacement vouchers are needed for the remainder of the taxable year.

- All calculations for estimated tax due should be meticulously derived using the Estimated Tax Worksheet provided in the form instructions.

- Corporations must sign and verify the form, confirming the accuracy and completeness of the information provided. This can be done by an authorized officer or the paid preparer, who must then include their corporate title or preparer firm's name and address.

- To submit the form and any accompanying payment, use a check or money order made payable to the Comptroller of the Treasury, ensuring all relevant tax year and identification information is clearly indicated. Mail the completed form and payment to the specified address in Annapolis, Maryland.

Understanding these elements of Form 500D can help corporations navigate the complexities of Maryland's estimated income tax requirements, ensuring compliance and avoiding unnecessary penalties.

Common PDF Templates

Maryland Tax Withholding - The form fosters compliance with state tax laws while allowing nonresidents to take advantage of Maryland-specific tax benefits and credits.

Maryland Car Registration - Completing the Maryland Application Vehicle form is essential for obtaining the necessary license plates to legally drive on Maryland roads.