Maryland 500Dm PDF Template

In Maryland, navigating state taxes involves understanding various forms that adjust how federal provisions impact local tax obligations. One such document, the Maryland 500DM form, plays a crucial role for taxpayers whose Maryland returns are influenced by specific federal laws. Essentials of the 500DM include its purpose for recalibrating the state tax implications of the special depreciation allowance, net operating loss (NOL) carryovers, and Section 179 depreciation deductions as outlined by the Job Creation and Worker Assistance Act of 2002 and the Jobs and Growth Tax Relief Reconciliation Act of 2003. The form consists of a worksheet designed to calculate the decoupling modification, guiding taxpayers through adjustments needed to align federal returns with Maryland's distinct regulations. Along with adjustments for depreciation and NOL, it also encompasses modifications from pass-through entities and other related changes affecting Maryland and local income taxes. Detailed instructions, alongside specific codes for various additions or subtractions on Maryland returns, provide clarity on filing requirements. This requisite form ensures that Maryland taxpayers comply with state tax laws while accounting for federal provision differences, making it indispensable for affected filings.

Maryland 500Dm Sample

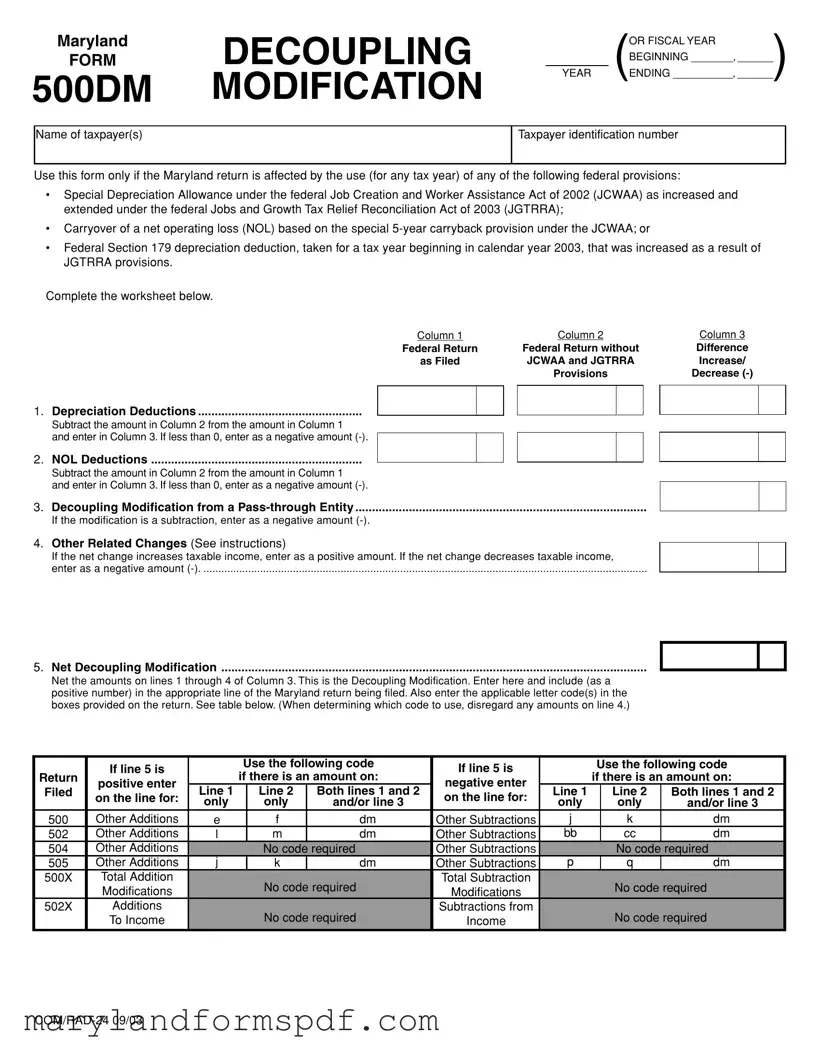

Maryland |

DECOUPLING |

YEAR |

OR FISCAL YEAR |

FORM |

_ (ENDING __________, ______) |

||

|

|

|

BEGINNING _______, ______ |

500DM |

MODIFICATION |

|

|

Name of taxpayer(s)

Taxpayer identification number

Use this form only if the Maryland return is affected by the use (for any tax year) of any of the following federal provisions:

•Special Depreciation Allowance under the federal Job Creation and Worker Assistance Act of 2002 (JCWAA) as increased and extended under the federal Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA);

•Carryover of a net operating loss (NOL) based on the special

•Federal Section 179 depreciation deduction, taken for a tax year beginning in calendar year 2003, that was increased as a result of JGTRRA provisions.

Complete the worksheet below.

Column 1 |

Column 2 |

Column 3 |

Federal Return |

Federal Return without |

Difference |

as Filed |

JCWAA and JGTRRA |

Increase/ |

|

Provisions |

Decrease |

1. Depreciation Deductions .................................................

Subtract the amount in Column 2 from the amount in Column 1

and enter in Column 3. If less than 0, enter as a negative amount

2.NOL Deductions ...............................................................

Subtract the amount in Column 2 from the amount in Column 1

and enter in Column 3. If less than 0, enter as a negative amount

3.Decoupling Modification from a

If the modification is a subtraction, enter as a negative amount

4.Other Related Changes (See instructions)

If the net change increases taxable income, enter as a positive amount. If the net change decreases taxable income,

enter as a negative amount

5.Net Decoupling Modification ...............................................................................................................................

Net the amounts on lines 1 through 4 of Column 3. This is the Decoupling Modification. Enter here and include (as a positive number) in the appropriate line of the Maryland return being filed. Also enter the applicable letter code(s) in the boxes provided on the return. See table below. (When determining which code to use, disregard any amounts on line 4.)

|

If line 5 is |

|

Use the following code |

If line 5 is |

|

Use the following code |

||||

Return |

|

if there is an amount on: |

|

if there is an amount on: |

||||||

positive enter |

|

negative enter |

|

|||||||

Filed |

Line 1 |

|

Line 2 |

Both lines 1 and 2 |

Line 1 |

|

Line 2 |

Both lines 1 and 2 |

||

on the line for: |

|

on the line for: |

|

|||||||

|

only |

|

only |

and/or line 3 |

only |

|

only |

and/or line 3 |

||

|

|

|

|

|

||||||

500 |

Other Additions |

e |

|

f |

dm |

Other Subtractions |

j |

|

k |

dm |

502 |

Other Additions |

l |

|

m |

dm |

Other Subtractions |

bb |

|

cc |

dm |

504 |

Other Additions |

|

|

No code required |

Other Subtractions |

|

|

No code required |

||

505 |

Other Additions |

j |

|

k |

dm |

Other Subtractions |

p |

|

q |

dm |

500X |

Total Addition |

|

|

No code required |

Total Subtraction |

|

|

No code required |

||

|

Modifications |

|

|

Modifications |

|

|

||||

502X |

Additions |

|

|

No code required |

Subtractions from |

|

|

No code required |

||

|

To Income |

|

|

Income |

|

|

||||

INSTRUCTIONS FOR |

PAGE 2 |

MARYLAND FORM 500DM |

|

DECOUPLING MODIFICATION

General Instructions

Purpose of Form

Maryland has decoupled from certain federal provisions, as listed at the top of Form 500DM, by enacting addition and subtraction modifications which eliminate the effect of the changes on Maryland and local taxes. This form is used to determine the amount of the required modification.

Use of Pro Forma Returns

Separate (pro forma) federal and Maryland returns must be prepared for use in completing Form 500DM. In addition to calculating depreciation and NOL deductions without the benefits afforded under the Job Creation and Worker Assistance Act of 2002 (JCWAA) and the Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA), pro forma returns will also help to determine other related items that affect Maryland and local income tax liability (e.g., income items, addition and subtraction modifications, deductions and credits).

Additional Information

For more information regarding these modifications, see Administrative Release 38 which is available on our website at www.marylandtaxes.com or from any office of the Comptroller.

Specific Instructions

Column 1 – Federal Return as Filed

Column 1 (lines 1 and 2) is used for the amounts reported on the federal return which include the impacts of the Special Depreciation Allowance, the special

Column 2 – Federal Return Without JCWAA and JGTRRA Provisions

Examples of items affected by decoupling are:

¥Gain or loss on sale of property

¥Recapture of depreciation

¥Passive loss

¥Maryland itemized deductions

Line 5 – Total

Net the amounts from lines 1 through 4 and enter on line 5. If line 5 is positive, include this amount in the appropriate line of the Maryland tax return being filed. Also enter the appropriate code letter(s) in the box(es) provided for the type of addition modification (either depreciation or NOL, or both).

If line 5 is negative, include this amount as a positive number in the appropriate line of the Maryland tax return being filed. Enter the appropriate code letter(s) in the box(es) provided for the type of subtraction modification (either depreciation or NOL, or both).

See the table at the bottom of Form 500DM for the line numbers and code letters to use.

Credits

For Maryland income tax credits affected by electing JCWAA and/or JGTRRA treatment, enter on the return to be filed, credits as calculated on the Maryland pro forma return without JCWAA and/or JGTRRA treatment.

Note: If a credit for a tax paid to another state was claimed on the original return and the tax liability to the other state and/or Maryland changes as a result of the treatment of the JCWAA and/or JGTRRA provisions in either state, a revised Form 502CR must be completed using the Maryland and the other stateÕs returns to be filed including all amendments and modifications.

Column 2 (lines 1 and 2) is for the amounts which would have been reported on the federal return using federal law in effect prior to enactment of the JCWAA and JGTRRA (without regard to the Special Depreciation Allowance, the special

Column 3 – Change – increase/decrease

Lines 1 and 2 — Subtract the amount in Column 2 from the amount in Column 1. Enter in Column 3. Line 4 is for the change to taxable income in other related items (calculated before and after application of the JCWAA and JGTRRA provisions) that would affect taxable income. If the change decreases taxable income, enter the amount with a minus sign

Line 1 – Depreciation Deductions

Use line 1 only for the depreciation expense deductions.

Line 2 – NOL Deductions

Use line 2 for NOL deductions. For Columns 1 and 2, limit the deductions as follows: For a corporation, the deduction may not exceed the federal taxable income. For all others, the deduction may not exceed the federal modified taxable income as determined on federal Form 1045, Schedule B.

Line 3 – Decoupling Modification from a

Use line 3 for decoupling modifications reported by a

Line 4 – Other Related Changes

If the entity is a PTE (partnership,

Income from a PTE

Each partner, shareholder or member that has a decoupling modification from a PTE must also complete Form 500DM. Enter the decoupling modification from the PTE on line 3 of Form 500DM. Also use this amount to adjust the income from the PTE on the pro forma federal return to determine if other related changes exist. These changes would be entered on line 4 of Form 500DM. Do not include any decoupling modification on the Maryland pro forma return.

Attachment of Forms

¥Original Return Attach the completed Form 500DM to the Maryland income tax return to be filed. Pro forma returns used to complete this form are not to be filed with the Comptroller or the IRS, but should be retained with your tax records.

¥Amended Return Attach the completed Form 500DM, schedules and pro forma returns to amended return to be filed.

For questions concerning Form 500DM contact:

Revenue Administration Division

Annapolis, Maryland

www.marylandtaxes.com

Decoupling may also affect other items included in federal adjusted gross income (AGI) allowable itemized deductions, as well as Maryland addition and subtraction modifications. Because these items also affect Maryland taxable income, the decoupling modification must include an adjustment for these changes. If the net change for these items reduces taxable income, enter as a negative amount

07/03

File Breakdown

| Fact Name | Description |

|---|---|

| Purpose of Form 500DM | This form is used to adjust a taxpayer's income for Maryland state tax purposes, removing the effect of certain federal tax provisions such as special depreciation allowance and net operating loss carryovers. |

| Required Adjustments | Taxpayers must re-calculate depreciation and NOL deductions without considering the JCWAA and JGTRRA provisions, among other related adjustments. |

| Use of Pro Forma Returns | Separate federal and Maryland pro forma returns are prepared to assist in completing the 500DM, focusing on income, modifications, deductions, and credits without JCWAA and JGTRRA benefits. |

| Decoupling Items | Decoupling adjustments include items like gain or loss on property sale, depreciation recapture, passive loss adjustments, and Maryland itemized deductions. |

| Completing the Form | The form is filled out using columns to list federal return amounts with and without JCWAA and JGTRRA provisions, and to calculate the necessary adjustments. |

| Attachment and Filing | Completed Form 500DM should be attached to the Maryland income tax return being filed. Pro forma returns used for calculations aren’t submitted but should be kept for records. |

| Governing Law | The adjustments aim to nullify the effect of specific federal provisions under JCWAA and JGTRRA on Maryland state taxes, as per the state's decoupling legislation. |

Steps to Filling Out Maryland 500Dm

Completing the Maryland 500DM form is a necessary step for taxpayers in Maryland who must adjust their state tax returns due to specific federal tax provisions. This modification ensures that the tax impact of certain federal allowances, such as special depreciation, net operating loss (NOL) carrybacks, and increased section 179 deductions, are neutralized on the Maryland tax return. By following a defined set of steps, taxpayers can accurately complete this form, ensuring compliance with Maryland's tax laws and possibly affecting their tax liability.

- Begin by entering the Decoupling Year or Fiscal Year for which you are filing this form at the top of the page, including both the starting and ending dates.

- Write the Name of Taxpayer(s) exactly as it appears on the Maryland tax return to ensure consistency across documents.

- Provide the Taxpayer Identification Number next to the taxpayer's name, which can be a Social Security Number for individuals or an Employer Identification Number for businesses.

- Under the worksheet section, start with Column 1 by entering the amounts from your federal tax return that include the effects of JCWAA and JGTRRA for:

- Depreciation Deductions

- NOL Deductions

- In Column 2, calculate and enter the amounts for Depreciation and NOL Deductions without the federal JCWAA and JGTRRA provisions. This typically requires the preparation of pro forma federal tax returns.

- Subtract the amounts in Column 2 from those in Column 1, and record the results in Column 3. If the result is negative, ensure to mark it with a minus sign (-).

- For Decoupling Modification from a Pass-through Entity, enter any adjustments passed through to you from partnerships, S-corporations, or similar entities as a negative amount if it is a subtraction.

- If there are Other Related Changes that increase or decrease taxable income due to decoupling, calculate the net change and enter it in Column 3. Use a negative sign for decreases.

- The Net Decoupling Modification requires you to total the amounts on lines 1 through 4 of Column 3. Record this total in Column 3, line 5, and include it on your Maryland tax return.

- Refer to the code table provided on the form to determine the appropriate letter code(s) for your situation based on the net decoupling modification. Enter this code in the boxes provided on the Maryland return.

- For any Maryland income tax credits affected, calculate these using pro forma return figures without JCWAA and JGTRRA treatment. Include these credits on your Maryland return if applicable.

- If adjustments are made for a credit for tax paid to another state, and it alters your tax liability, complete a revised Form 502CR using both the Maryland and other state’s returns, including modifications.

- Attach Form 500DM to your Maryland tax return. Maintain copies of pro forma returns used for this calculation with your records.

This procedure ensures that taxpayers properly account for disallowed federal provisions, effectively aligning their Maryland state tax obligations with state-specific requirements. By meticulously filling out the Maryland 500DM form, taxpayers can address any discrepancies between federal and state tax calculations, thereby adhering to Maryland tax laws and potentially adjusting their tax liabilities.

More About Maryland 500Dm

What is the purpose of the Maryland Form 500DM?

The Maryland Form 500DM, also known as the Decoupling Modification Form, serves to adjust the amount of income subject to tax in Maryland. This adjustment is necessary due to Maryland's decision to not follow certain federal tax provisions related to depreciation, net operating losses, and deductions. By completing this form, taxpayers ensure that their Maryland tax returns accurately reflect these decoupling adjustments.

When should a taxpayer use Form 500DM?

Form 500DM should be used if a taxpayer's Maryland return is influenced by the adoption of any of the following federal provisions:

- Special Depreciation Allowance under the federal Job Creation and Worker Assistance Act of 2002, as extended or increased by subsequent legislations.

- Carryover of a net operating loss (NOL) using the special 5-year carryback provision.

- Section 179 depreciation deduction, with an increase for any tax year beginning in 2003, due to legislative changes.

What are the key components of Form 500DM?

Form 500DM includes columns for entering amounts from the federal return with and without the provisions of JCWAA and JGTRRA, alongside any resulting difference. Specific lines on the form help calculate adjustments related to:

- Depreciation Deductions

- NOL Deductions

- Decoupling Modification from a Pass-through Entity

- Other Related Changes

- Net Decoupling Modification

What should be included in the Decoupling Modification from a Pass-through Entity (PTE)?

For any decoupling modifications reported by a Pass-through Entity, partners, shareholders, or members must include only their share of the modification. Additions are entered as a positive number, while subtractions are indicated with a negative sign (-).

How does one calculate the Net Decoupling Modification?

The Net Decoupling Modification is calculated by netting the amounts on lines 1 through 4 of Column 3. This total modification then needs to be reported on the Maryland income tax return being filed, with the appropriate code letters indicating whether it's an addition or subtraction modification.

Are there specific instructions for income adjustments from Pass-through Entities?

Income adjustments from a Pass-through Entity require the taxpayer to also fill out Form 500DM, reporting their share of the decoupling modification. Additionally, this information should be utilized to adjust the income from the PTE on the pro forma federal return for any related changes. However, these modifications should not be added or subtracted on the Maryland pro forma return.

What are the requirements for attaching Form 500DM?

Upon completion, Form 500DM must be attached to the Maryland income tax return. While the pro forma returns employed to fill out Form 500DM are not filed with the Comptroller or the IRS, they must be kept as part of the taxpayer's records. If an amended return is being filed, Form 500DM along with any schedules and pro forma returns must accompany this submission.

Who can be contacted for further inquiries about Form 500DM?

For additional questions, taxpayers can contact the Revenue Administration Division in Annapolis, Maryland, either by calling 410-260-7980 or toll-free at 1-800-MDTAXES. Further information can also be found online at www.marylandtaxes.com.

Common mistakes

Filling out the Maryland 500DM form can be challenging, with several common mistakes that individuals often make. Recognizing and avoiding these mistakes can streamline the filing process and ensure accurate reporting of your financial information. Here are nine mistakes to watch out for:

- Not using pro forma returns for comparison: Failing to prepare separate federal and Maryland pro forma returns to calculate depreciation and NOL deductions without the benefits under JCWAA and JGTRRA laws can lead to inaccuracies.

- Incorrect calculations in Column 3: It's crucial to subtract the amount in Column 2 from Column 1 accurately. If the result is less than zero, it must be entered as a negative amount.

- Skipping the depreciation deductions on Line 1, which can result in an incomplete decoupling modification calculation.

- Omitting or misreporting NOL deductions on Line 2 can lead to an incorrect understanding of fiscal health and tax obligations.

- Forgetting to adjust for pass-through income decoupling modifications from a Pass-through Entity on Line 3, when applicable, whether as an addition or subtraction.

- Overlooking other related changes that could affect taxable income, mentioned on Line 4, leading to discrepancies in the net decoupling modification.

- Not properly calculating the net decoupling modification on Line 5, including it inaccurately on the Maryland return.

- Failing to attach the completed Form 500DM to the filed Maryland income tax return, or if amended, to the amended return.

- Ignoring specific instructions for calculating Maryland income tax credits affected by JCWAA and/or JGTRRA treatment, which can result in an incorrect amount being reported.

By steering clear of these mistakes, taxpayers can ensure a smoother and more accurate filing process.

Documents used along the form

When handling Maryland's Form 500DM, understanding the context and complementary documentation is vital for individuals and businesses aiming to comply with state tax regulations fully. While the 500DM form is specifically designed to adjust for decoupling modifications, various other forms and documents often accompany it to ensure a comprehensive approach to tax filing in Maryland. This selection of documents spans from initial business registration to intricate tax details, reflecting the diverse needs throughout the tax preparation process.

- Maryland Form 1: Articles of Organization for LLCs, or incorporation documents for corporations, are foundational. They're essential for establishing legal identity and tax obligations in Maryland.

- Maryland Form 510: Used by pass-through entities like S-corporations, partnerships, LLCs treated as partnerships for tax purposes, to report income, gains, losses, and deductions, and to calculate the entity's Maryland income tax.

- Maryland Form 502: The individual income tax return form for Maryland residents, applicable for individuals reporting personal income, adjustments, deductions, and credits to the state.

- Maryland Form 502CR: A form for claiming various nonrefundable and refundable Maryland tax credits, including credits for taxes paid to other states, geared towards individual taxpayers.

- Maryland Form 500: The corporate income tax return form, necessary for C corporations to file their annual income tax to the state. It encompasses comprehensive details about income, taxes, and credits.

- Maryland Form MW506NRS: Required for nonresident sale of real property, this form is crucial for real estate transactions involving out-of-state sellers, ensuring proper income reporting and withholding.

- Schedule K-1 (Form 510): This document outlines each pass-through entity member's share of income, deductions, and credits. It's pivotal for personal tax filings, connecting individual liability with entity earnings.

- Maryland Form 504: The fiduciary income tax return, used by estates and trusts to report income, deductions, gains, losses, and to calculate their Maryland income tax liability.

- Maryland Personal Property Return: A yearly requirement for businesses to report personal property (equipment, furniture, etc.) for taxation purposes, affecting local county taxes.

Each of these documents plays a specific role in the comprehensive tapestry of tax and legal compliance within Maryland. They embody the intricate balance between state-specific requirements and federal tax obligations, ensuring entities and individuals meet their complete reporting and payment responsibilities. Understanding how these forms interact with the Form 500DM is crucial for accurate tax filing and minimizes the risk of errors or oversights that could lead to penalties or missed opportunities for tax optimization.

Similar forms

The Maryland 500DM form is similar to other tax documents that require adjustments related to specific legislative provisions. This form provides a clear example of how state responses can diverge from federal tax legislation through its focus on decoupling from federal tax provisions. Below, two notable documents resembling the Maryland 500DM form in purpose and structure are explored.

Form 1045, Application for Tentative Refund: This federal form is somewhat akin to the Maryland 500DM, particularly in its handling of net operating loss (NOL) deductions. Both forms require detailed calculations to adjust taxable income — the 500DM for the decoupling adjustments and Form 1045 for carrying back NOLs to obtain tentative refunds. Specifically, they share a similar layout in requiring taxpayers to list initial amounts, adjustments, and the results of those adjustments. However, while Form 1045 focuses on federal NOL provisions, the Maryland 500DM specifically addresses adjustments needed to separate Maryland tax calculations from federal provisions under the JCWAA and JGTRRA.

Form 4562, Depreciation and Amortization: Similar to the Maryland 500DM, IRS Form 4562 involves the calculation of depreciation, but for federal tax purposes. Both documents require taxpayers to report depreciation but for somewhat different reasons. Form 4562 is used to calculate the depreciation and amortization that are deductible on a taxpayer's federal return, including the Section 179 expense deduction and the special depreciation allowance. The Maryland 500DM form requires similar information to make necessary adjustments for Maryland state tax purposes, ensuring that the state's decoupling provisions are accurately reflected in Maryland taxable income. This decoupling requires a comparison of federal deductions with what those deductions would be without the application of certain federal provisions, underscoring the form's role in adjusting how federal legislative changes impact state taxes.

Dos and Don'ts

When completing the Maryland 500DM form, attention to detail can ensure accurate reporting and compliance with state tax laws. Below are essential dos and don'ts to guide taxpayers through the process.

- Do thoroughly review the general instructions before starting to ensure you understand the form's requirements.

- Do use the pro forma federal and Maryland returns as a basis for completing the 500DM, focusing on accurately calculating adjustments.

- Do carefully fill out Column 1 with the federal return figures as filed, including all relevant impacts of federal provisions.

- Do calculate the figures for Column 2 based on federal law prior to the JCWAA and JGTRRA provisions, ensuring accurate adjustments are made.

- Do ensure that adjustments in Column 3 accurately reflect the increase or decrease from Columns 1 to 2, using a negative sign (-) for decreases.

- Don't overlook adjustments needed for pass-through entities; ensure that modifications are accurately reported on both relevant sections of the form.

- Don't neglect to attach the completed Form 500DM to your Maryland income tax return, as failure to do so can result in processing delays.

- Don't discard your pro forma returns after completion; retain them with your tax records for future reference or in case of audit.

- Don't hesitate to consult with a tax professional if you encounter difficulties or have questions about specific adjustments or provisions.

By following these guidelines, taxpayers can navigate the complexities of the Maryland 500DM form with confidence, ensuring compliance and minimizing the risk of errors. Proper attention to each step of the process will facilitate accurate decoupling adjustments and contribute to smoother tax return preparation overall.

Misconceptions

Understanding the Maryland Form 500DM, used for decoupling modifications, involves clearing up common misconceptions. This form is essential for correcting the differences between federal and state taxable income due to specific federal provisions. Here are four common misunderstandings about the form:

- It's only for businesses. While the form appears complex and business-oriented due to terms like "depreciation" and "net operating loss," it's not solely for corporations or businesses. Individuals participating in pass-through entities, such as partnerships or S corporations, may also need to complete this form if they have decoupling modifications.

- All federal tax provisions are decoupled in Maryland. Only specific federal provisions trigger the need for the Maryland 500DM form. These are special depreciation under the JCWAA and JGTRRA, the special 5-year NOL carryback provision under the JCWAA, and increased Section 179 deductions. Maryland has not decoupled from all federal tax provisions.

- The form complicates tax returns for everyone. Actually, the form simplifies the process of adjusting returns for those affected by Maryland's decision to decouple from specific federal provisions. By clearly outlining the differences between federal and state returns, it ensures taxpayers do not pay more state tax than necessary.

- Decoupling adjustments always result in higher taxes. While it's true that decoupling can sometimes lead to higher taxable income at the state level, this is not always the case. For instance, if the adjustment involves subtracting an addition made to the federal taxable income or adds back an excess deduction, it could lower the state taxable income or have a neutral effect. The actual impact depends on individual circumstances and the nature of the decoupling modification.

In conclusion, the Maryland Form 500DM is a critical tool for accurately reporting state income tax in light of specific federal tax provision decouplings. By addressing these misconceptions, taxpayers can better understand the form's purpose and its effects on their tax liability.

Key takeaways

The Maryland 500DM form is instrumental in adjusting state tax returns for individuals and entities whose taxes are influenced by specific federal tax provisions that Maryland "decouples" from. Understanding how to accurately complete and utilize this form ensures compliance with state tax laws, effectively managing tax liabilities, and avoiding potential errors that could lead to audits or penalties. Here are four key takeaways about the Maryland 500DM form:

- Decoupling Purpose: Maryland has elected to decouple from certain federal tax provisions, namely the Special Depreciation Allowance, specific Net Operating Loss (NOL) carryback provisions, and increased Section 179 depreciation deductions. Form 500DM serves as a tool to adjust the state tax return, neutralizing the impact of these federal provisions on Maryland and local income taxes.

- Use of Pro Forma Returns: To accurately complete the 500DM form, taxpayers must prepare pro forma federal and Maryland tax returns. These pro forma returns calculate depreciation and NOL deductions without the benefits of the federal Job Creation and Worker Assistance Act of 2002 (JCWAA) and the Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA), among other related adjustments. This step is crucial for identifying the necessary modifications to the Maryland tax return.

- Reporting Modifications: The form guides taxpayers through calculating and reporting the difference between the federal return with and without the JCWAA and JGTRRA provisions. Taxpayers need to determine the net decoupling modification and how it affects their tax liability. Positive modifications increase taxable income and require a specific code on the Maryland return, while negative modifications decrease taxable income and are also coded differently.

- Pass-Through Entity Adjustments and Credits: For pass-through entities (PTEs) and their members, Form 500DM is essential for reporting each partner, shareholder, or member's share of decoupling modifications. Moreover, Maryland income tax credits that might be affected by the federal provisions need recalculation without the federal benefits on a separate pro forma return. This recalculated figure is then reported on the Maryland return being filed.

Overall, proper completion and understanding of the 500DM form are essential for accurately reporting taxes in Maryland, particularly for those affected by specific federal provisions that the state does not follow. This ensures tax compliance while potentially mitigating tax liabilities attributed to the decoupling adjustments.

Common PDF Templates

Masonic Charities of Maryland - Contains a privacy statement regarding the use and protection of personal information submitted through the application.

Maryland Corporate Tax Due Date - Demands a thorough review and completion of nonresident beneficiary deductions to accurately report tax liabilities.

Printable New Employee Forms - Reports on the Maryland New Hire Registry Reporting Form must be submitted within 20 days of the employee's start date.