Maryland 500E PDF Template

Understanding the complexities of tax filings can be a challenging task for corporations in Maryland, which is where the Maryland Application for Extension of Time to File Corporation Income Tax Return, commonly known as Form 500E, comes into play. Deep diving into what this form entails, it essentially serves as a lifeline for corporations that aren’t able to meet their income tax filing deadlines. Revised in 1996, Form 500E offers a straightforward way for corporations to request an additional six months to file their income tax returns, ensuring they remain compliant with Maryland's tax laws while managing their financial planning more effectively. It's important to note that this form cannot be used by S corporations or for remitting employer withholding tax, making its applicability specific to certain business entities. Moreover, the form stipulates a necessity for the tentative tax amount and estimated tax payments to be declared upfront, accompanied by the total amount due if applicable. The stringent guidelines surrounding the submission process, including the automatic denial of extensions for late submissions or incomplete tax payments, underscore the importance of understanding and accurately completing the form. Addressed to the Comptroller of the Treasury, Revenue Administration Division in Annapolis, Maryland, Form 500E also emphasizes Maryland's disallowance of consolidated tax returns, requiring affiliated corporations who file a consolidated federal return to submit individual extension applications. With a wealth of specific instructions provided, including where and how to file, along with payment directions, the form underscores Maryland's structured approach to tax extensions, aiming to streamline the process while ensuring fiscal responsibility among its corporate citizens.

Maryland 500E Sample

M ARYLAND |

|

APPLICATION FOR EXTENSION OF TIME TO |

|

|

|

19 |

|

||||||||||

FORM 500E |

|

FILE CORPORATION INCOME TAX RETURN |

|

|

|

|

|||||||||||

(Revised 1996) |

|

|

FOR TAXABLE YEAR BEGINNING_____________, 19___ |

|

|

|

|

||||||||||

|

M AIL TO: |

COM PTROLLER OF THE TREASURY |

ENDING_____________, 19___ |

|

|

|

|

|

|

||||||||

|

|

REVENUE ADM INISTRATION DIVISION |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

ANNAPOLIS, M ARYLAND |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

DO NOT WRITE IN THIS SPACE |

|||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nam e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Num ber and street |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RM |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or tow n |

|

|

|

State |

Zip code |

|

M E |

YE |

|

EC |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

▶ |

|

▶ |

|

▶ |

|

▶ |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Federal Em ployer Identification No. (9 digits) |

|

FEIN Applied for date |

|

Date of Incorporation (6 digits) |

|

|

Federal Business Code No. (4 digits) |

|||||||||

|

▶ |

|

|

|

|

|

|

▶ |

|

|

|

|

|

▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CHECK HERE IF: |

|

☐ NAME OR ADDRESS HAS CHANGED |

NOTE: DO NOT USE THIS FORM |

) |

|

|

|

|

|||||||||

|

FOR S CORPORATIONS — SEE |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

☐ FIRST FILING OF THE CORPORATION |

(INSTRUCTIONS FOR FORM 510 |

|

|

|

|

|||||||||

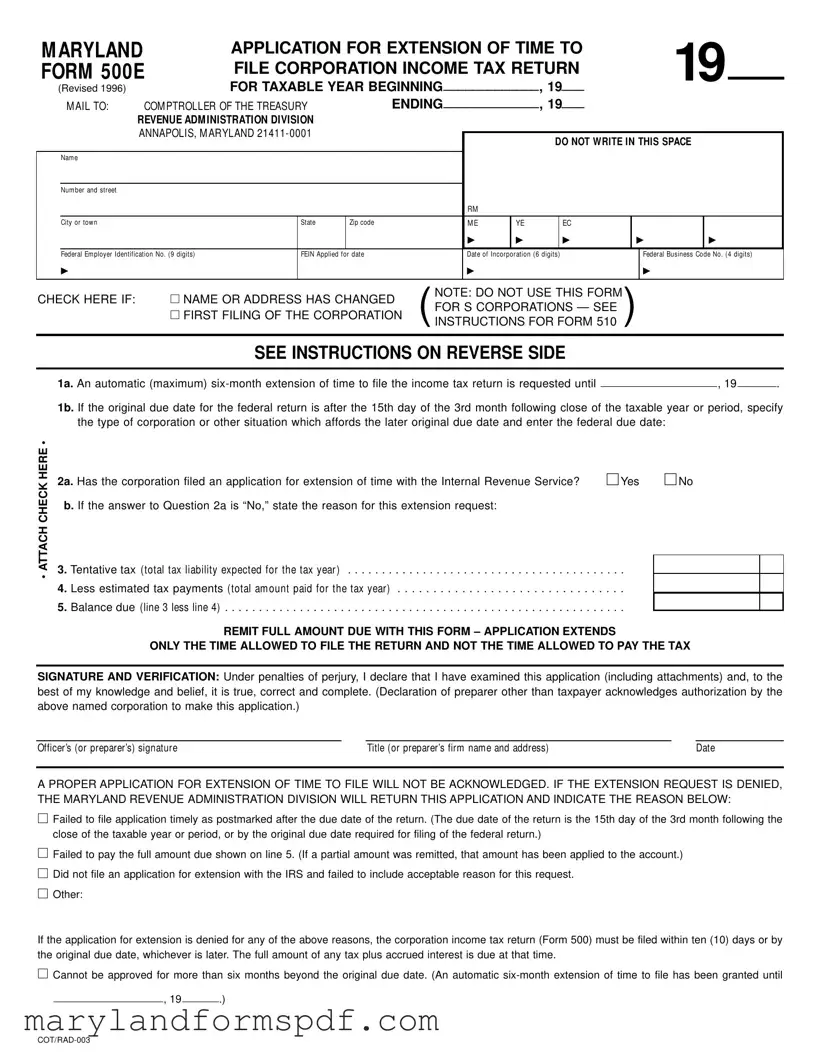

SEE INSTRUCTIONS ON REVERSE SIDE

• ATTACH CHECK HERE •

1a. An automatic (maximum)

1b. If the original due date for the federal return is after the 15th day of the 3rd month following close of the taxable year or period, specify the type of corporation or other situation which affords the later original due date and enter the federal due date:

2a. Has the corporation filed an application for extension of time with the Internal Revenue Service? |

☐ Yes |

☐ No |

0b. If the answer to Question 2a is “No,” state the reason for this extension request:

3. Tentative tax (total tax liability expected for the tax year ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. Less estimated tax payments (total am ount paid for the tax year) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5. Balance due (line 3 less line 4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

REMIT FULL AMOUNT DUE WITH THIS FORM – APPLICATION EXTENDS

ONLY THE TIME ALLOWED TO FILE THE RETURN AND NOT THE TIME ALLOWED TO PAY THE TAX

SIGNATURE AND VERIFICATION: Under penalties of perjury, I declare that I have examined this application (including attachments) and, to the best of my knowledge and belief, it is true, correct and complete. (Declaration of preparer other than taxpayer acknowledges authorization by the above named corporation to make this application.)

Officer’s (or preparer’s) signature |

Title (or preparer’s firm nam e and address) |

Date |

A PROPER APPLICATION FOR EXTENSION OF TIME TO FILE WILL NOT BE ACKNOWLEDGED. IF THE EXTENSION REQUEST IS DENIED, THE MARYLAND REVENUE ADMINISTRATION DIVISION WILL RETURN THIS APPLICATION AND INDICATE THE REASON BELOW:

☐Failed to file application timely as postmarked after the due date of the return. (The due date of the return is the 15th day of the 3rd month following the close of the taxable year or period, or by the original due date required for filing of the federal return.)

☐Failed to pay the full amount due shown on line 5. (If a partial amount was remitted, that amount has been applied to the account.)

☐Did not file an application for extension with the IRS and failed to include acceptable reason for this request.

☐Other:

If the application for extension is denied for any of the above reasons, the corporation income tax return (Form 500) must be filed within ten (10) days or by the original due date, whichever is later. The full amount of any tax plus accrued interest is due at that time.

☐Cannot be approved for more than six months beyond the original due date. (An automatic

__________________, 19 ______.)

INSTRUCTIONS FOR MARYLAND FORM 500E (Revised 1996)

APPLICATION FOR EXTENSION OF TIME

TO FILE CORPORATION INCOME TAX RETURN

GENERAL INSTRUCTIONS

Purpose of Form Form 500E is used by a corporation to request an extension of time to file the corporation income tax return (Form 500) and to remit any balance of tax due.

NOTE: Do not use this form for

General Requirements Maryland law provides for an extension of time to file, but in no case can an extension be granted for more than six months beyond the original due date. A request for exten- sion of time to file will be automatically granted for six months, provided that:

1)Form 500E is properly filed and submitted by the original due date (15th day of the 3rd month following close of the tax year or period, or by the original due date required for filing of the federal return);

2)full payment of any balance due is submitted with Form 500E; and

3)an application for extension of time has been filed with the Internal Revenue Service or an acceptable reason has been provided with Form 500E.

A proper application for extension of time to file will not be acknowledged. If the extension request is denied, the corporation will be notified.

Form 500E does not extend the time allowed to pay the tax. Maryland law provides for accrual of interest and imposition of penalty for failure to pay any tax when due.

Consolidated returns are not allowed under Maryland law. Affiliated corporations which file a consolidated federal return must file separate Maryland extension applications for each member corporation.

When and Where to File File Form 500E by the 15th day of the 3rd month following the close of the taxable year or period, or by the original due date required for filing the federal return. The application for extension of time must be filed with the Comptroller of the Treasury, Revenue Administration Division, Annapolis, Maryland

SPECIFIC INSTRUCTIONS

Name, Address and Other Information Type or print the required information in the designated area. DO NOT USE THE LABEL FROM THE TAX BOOKLET COVER.

Enter the name exactly as specified in the Articles of Incorpo- ration, or as amended, and continue with any “Trading As” (T/A) name if applicable.

Enter the Federal Employer Identification Number (FEIN). If a FEIN has not been secured, enter “APPLIED FOR” followed by the date of application. If a FEIN has not been applied for, do so immediately.

Check the applicable box if the name or address has changed or if this is the first filing of the corporation.

Taxable Year or Period ENTER THE BEGINNING AND END-

ING DATES OF THE TAXABLE YEAR IN THE SPACE PROVIDED AT THE TOP OF FORM 500E.

The same taxable year or period used for the federal return must be used for Form 500E.

Tentative Tax Enter the total amount of income tax liability expected for the tax year on line 3.

Estimated Tax Payments Enter on line 4 the total amounts paid with Form 500DP or 500D – Declaration of Estimated Corporation Income Tax for the taxable year or period. Also include any amount carried forward as a credit from the prior year Form 500 – Corporation Income Tax Return.

Balance Due Enter the amount of tax due on line 5 and remit full payment with this form.

Signature and Verification An authorized officer or the paid preparer must sign and date Form 500E indicating the corporate title or preparer firm name and address.

Payment Instructions Include a check or money order made payable to the Comptroller of the Treasury for the full amount of any balance due. All payments must indicate the Federal Employer Identification Number, type of tax and tax year beginning and ending dates. DO NOT SEND CASH.

Mailing Instructions Use the envelope provided in the tax booklet and place an “X” in the appropriate box in the lower left corner to indicate the type of document enclosed. Also, be sure to read and follow the reminders listed on the back of the envelope.

File Breakdown

| Fact | Detail |

|---|---|

| Purpose of Form 500E | Used by corporations to request an extension of time to file the Maryland Corporation Income Tax Return (Form 500) and to remit any balance of tax due. |

| Governing Law | Maryland law allows for an extension of time to file but not beyond six months of the original due date. It also mandates accrual of interest and imposes penalties for not paying taxes when due. |

| Eligibility | Not applicable for pass-through entities (including S corporations) or for remitting employer withholding tax. |

| Automatic Extension Period | An automatic six-month extension will be granted if the application is properly filed by the original due date, full payment of the balance due is made, and an IRS extension has been filed or an acceptable reason is provided. |

| Payment Requirements | Form 500E does not extend the time allowed to pay the tax; full payment of any tax balance is required when filing the form. |

| Filing Instructions | Must be filed by the 15th day of the 3rd month following the close of the taxable year or by the original due date required for the federal return, directed to the Comptroller of the Treasury, Revenue Administration Division, Annapolis, Maryland. |

Steps to Filling Out Maryland 500E

After completing the necessary preparation, attention now turns to accurately filling out the Maryland Form 500E. This form, designed for corporations seeking an extension for filing their income tax returns, requires careful attention to detail. The correct and timely submission of this document ensures compliance with state tax obligations, thereby avoiding possible penalties and interest for late filings. Next listed are the recommended steps to efficiently complete and submit the Form 500E, ensuring all required information is correctly provided and the process aligns with state requirements.

- Start by indicating the taxable year beginning and ending dates at the top of the form.

- In the designated area, correctly type or print the corporation's name, number and street, including city or town, state, and zip code.

- Fill in the Federal Employer Identification Number (FEIN). If FEIN is pending, write "APPLIED FOR" and the application date.

- Check appropriate boxes if the corporation's name or address has changed, or if this is the first filing.

- Complete section 1a by entering the date to which an extension is being requested.

- If applicable, fill out section 1b with the type of corporation or situation that allows for a later original federal return due date, including this date.

- Mark "Yes" or "No" for question 2a to indicate if an extension has been filed with the IRS. If "No," provide a reason in section 2b.

- Enter the tentative total tax liability expected for the tax year in the space provided for section 3.

- Document the estimated tax payments already made for the tax year in section 4.

- Calculate and enter the balance due, if any, on line 5, and prepare to remit the full amount with the form.

- The form must be signed and dated by an authorized officer or the preparer, indicating their title or firm name and address in the "Signature and Verification" section.

- Include a check or money order payable to the Comptroller of the Treasury for any balance due. Ensure the corporation's FEIN, type of tax, and the tax year's beginning and ending dates are indicated on the payment.

- Finally, mail the completed Form 500E and payment to the Comptroller of the Treasury, Revenue Administration Division, Annapolis, Maryland 21411-0001, using the envelope provided in the tax booklet. Place an “X” in the appropriate box in the lower left corner to indicate the type of document enclosed and follow the envelope's mailing instructions.

Accurately following these steps for completing and submitting Maryland Form 500E is essential for securing an extension of time to file the corporation income tax return while remaining compliant with Maryland tax laws.

More About Maryland 500E

What is the Maryland Form 500E and when is it used?

The Maryland Form 500e serves as an application for corporations seeking an extension of time to file their income tax return. This form becomes relevant when a corporation cannot file its return by the original due date, which is typically the 15th day of the 3rd month following the close of the tax year. By submitting this form by the proper deadline, a corporation can request up to a six-month extension to file. However, it's important to note that this extension applies only to the filing deadline, not to the payment of any taxes owed.

What are the conditions for automatically granting the extension?

An extension to file using Form 500e is automatically granted under the following conditions:

- The form is properly filled out and submitted by the original due date.

- The full payment of any balance due is included with the form submission.

- An application for an extension of time has also been filed with the IRS, or an acceptable reason for not doing so is provided.

How should the Maryland Form 500E be filled out and submitted?

To properly complete the Maryland Form 500E, corporations must:

- Fill in the corporation’s name as it appears in the Articles of Incorporation, including any trading names if applicable.

- Provide the Federal Employer Identification Number (FEIN). If this hasn't been secured, indicate that it's been applied for along with the application date.

- Check the appropriate box if there's been a change in name or address, or if it’s the corporation's first filing.

- Clearly state the taxable year or period for which the extension is requested.

- Calculate and enter the tentative tax due, estimated tax payments made, and the balance due.

What happens if the extension request is denied?

If the Maryland Revenue Administration Division denies the extension request, they will return the application indicating the reason for denial. Common reasons include filing the application late, failure to pay the full amount due, or not filing an extension application with the IRS without providing an acceptable reason. If denied, the corporation must file its income tax return (Form 500) within ten days or by the original due date, whichever is later, along with the full amount of any tax due plus accrued interest.

Common mistakes

Filling out the Maryland 500E form, which is an application for an extension of time to file the corporation income tax return, may seem straightforward, yet mistakes can easily be made. These errors can delay processing or even result in the denial of the extension request. Here are five common mistakes to watch for:

- Incorrect or Incomplete Name and Address Information: The top error is not entering the corporation's name and address as per the Articles of Incorporation or as amended. Any "Trading As" (T/A) name should also be included if applicable. Always double-check the entered Federal Employer Identification Number (FEIN) for accuracy.

- Filing Under Incorrect Entity Type: Many mistakenly use Form 500E for pass-through entities including S Corporations, which is not permitted. This form is exclusively for C Corporation or entities required to file as C Corporations for Maryland tax purposes.

- Not Including the Required Payment with the Application: An extension to file is not an extension to pay. Any tax due should be accurately calculated on Line 5 and fully paid when submitting Form 500E. Failing to do so can lead to a denial of the extension request and the accrual of interest and penalties.

- Application Not Timely Filed: Another common mistake is not submitting the form by the due date – the 15th day of the 3rd month following the close of the taxable year or period, or by the original due date required for the filing of the federal return. A late submission automatically disqualifies the request for an extension.

- Omitting Signature and Verification: The form requires an authorized officer's or paid preparer’s signature, along with their title or firm name and address. An unsigned application can be seen as incomplete and can result in the denial of the extension request.

Attention to detail can significantly influence the successful processing of the Maryland 500E form. By avoiding these common pitfalls, corporations can ensure a smoother extension request process.

Documents used along the form

When preparing for corporate income tax matters, businesses in Maryland utilize the Maryland Form 500E to request additional time for filing their annual tax returns. However, it's pivotal to understand that this form does not operate in isolation. Several other documents often accompany the Form 500Pox proceeding with filing or extending time frames for a corporation's income tax obligations. These documents ensure compliance with state tax laws and facilitate the accurate processing of requests and tax returns.

- Form 500: The Maryland Corporation Income Tax Return is the primary document filed after or alongside the Maryland Form 500E when the extension period ends. It comprehensively covers the corporation's income, deductions, and taxes due for the year.

- Form 500DP: This Declaration of Estimated Corporation Income Tax Payments voucher is used for corporations to submit their estimated tax payments. It is crucial for those that expect to owe, ensuring they meet payment obligations throughout the year and avoid penalties for underpayment.

- Form 500D: Similar to Form 500DP, the Maryland Declaration of Estimated Corporation Income Tax is designed for corporations to file and pay their estimated taxes quarterly, assisting in spreading the tax burden across the fiscal year.

- Form MW506NRS: For corporations that manage properties in Maryland and make payments to nonresident members, this Annual Return of Income Tax Withholding for Nonresident Sale of Real Property is necessary. It ensures proper reporting and withholding taxes on such transactions.

- Form CRA: The Combined Registration Application is essential for newly formed corporations or existing ones that have not previously registered with the state. This form is a comprehensive application for several tax-related responsibilities, including unemployment insurance, sales and use tax, and income tax withholding.

Together, these forms create a network of documentation that supports the Maryland Form 500E, ensuring that corporations meet their tax obligations thoroughly. Proper completion and timely submission of these documents guarantee compliance with Maryland's tax laws and help corporations avoid penalties associated with late filings or payments. It's a collective effort toward maintaining fiscal responsibility and contributing to the state's economic health.

Similar forms

The Maryland 500E form is similar to other tax extension forms used both federally and in various states, designed to grant businesses more time to file their tax returns without penalties for late submission, provided certain conditions are met. Three such forms that share similarities with the Maryland 500E form are the IRS Form 7004, the California Form 3539, and the New York CT-5 Form. Each of these forms serves a similar purpose but has unique elements reflecting the tax laws and requirements of their respective jurisdictions.

IRS Form 7004 is a federal application for an automatic extension of time to file certain business income tax, information, and other returns. Like the Maryland 500E, the IRS Form 7004 does not extend the time to pay any taxes due but allows for additional time to file the necessary paperwork. Both forms require the filer to estimate their tax liability and pay any expected balance due at the time of filing the extension request. The primary difference lies in the scope, with Form 7004 applicable to a wide range of business entities at the federal level, while the 500E is specific to corporations operating within Maryland.

California Form 3539, or the Payment for Automatic Extension for Corporations and Exempt Organizations, offers a parallel to Maryland's 500E in that it provides corporations and other entities an extension of time to file their income tax returns. Similarities include the necessity for estimated tax payments to accompany the form if taxes are owed. However, the Form 3539 is specific to California and caters to both corporations and exempt organizations needing more time to file their state income tax returns. This illustrates a commonality in the procedural approaches states take to facilitate tax filings and extensions while highlighting the variance in forms tailored to each state's tax code.

New York's CT-5 Form allows corporations to request a six-month extension to file their franchise tax return. Much like the Maryland 500E, the CT-5 requires the payment of any estimated tax due by the original due date of the return. The form accommodates entities that are subject to New York State's franchise tax, reflecting the state-specific nature of tax administration and compliance. Despite their jurisdictional differences, both forms underscore the principle that while filings can be delayed, the responsibility for calculating and remitting any taxes owed by the original deadline remains with the taxpayer.

Dos and Don'ts

When filling out the Maryland 500 years form, individuals and corporations should take certain steps to ensure accuracy and compliance with tax regulations. Below are things you should and shouldn't do when completing this form:

Do review the general instructions carefully before beginning to fill out the form to understand the form's purpose and the requirements.

Do make sure the form is submitted by the original due date to avoid penalties.

Do ensure full payment of any balance due is submitted with Form 500E as the extension only applies to the filing, not to the payment.

Do file an application for extension of time with the Internal Revenue Service, if applicable, and provide acceptable reasoning if not.

Do type or print the required information clearly in the designated areas to avoid processing delays.

Do not use this form for pass-through entities, including S corporations, or to remit employer withholding taxes.

Do not leave the Federal Employer Identification Number (FEIN) section blank. If a FEIN has not been secured, promptly apply for one.

Do not neglect to include any changes in name or address or forget to mark the box if this is the first filing of the corporation.

Do not underestimate the tentative tax and estimated tax payments as this could result in a balance due that could accumulate interest and penalties.

Do not forget to sign and date the form. An authorized officer or the paid preparer must sign the form indicating their corporate title or preparer's firm name and address.

Following these guidelines will help ensure the Maryland 500E form is completed accurately and submitted on time, thereby avoiding possible delays or penalties.

Misconceptions

Understanding the Maryland Form 500E, the application for an extension of time to file a corporation income tax return, is crucial for businesses operating in Maryland. However, there are several misconceptions surrounding this form. Addressing these misconceptions can clarify its purpose and requirements.

- Misconception 1: The 500E form extends the time to pay taxes.

This is incorrect. The form only extends the filing deadline, not the time to pay owed taxes. Any taxes due are expected to be paid by the original due date to avoid penalties and interest. - Misconception 2: S Corporations can use Form 500E.

S Corporations must not use this form. Instead, they should refer to instructions for Form 510, which is geared towards pass-through entities like S Corporations. - Misconception 3: You can use the 500E form without an FEIN.

All corporations must provide their Federal Employer Identification Number (FEIN) on the form. If it has not been secured, "Applied For" along with the application date should be entered. - Misconception 4: Filing Form 500E automatically grants a six-month extension.

While generally true, the extension is only granted if the form is correctly filed by the due date, includes full payment of any taxes due, and accompanies an IRS extension request, if applicable. - Misconception 5: The form must be acknowledged to be valid.

A proper application does not require acknowledgment from the Maryland Comptroller's Office to be considered valid. If the request is denied, however, the applicant will be notified. - Misconception 6: Penalties and interest are paused with Form 500E.

Filing this form does not stop the accrual of interest and penalties for taxes not paid by the original due date. - Misconduct 7: Any balance due when filing Form 500E can be paid later.

Any tax liability expected for the year must be paid with the application to avoid penalties for late payment. - Misconcept 8: Consolidated returns are allowed for corporations filing Form 500E.

Maryland law does not permit consolidated returns. Affiliated corporations filing a consolidated federal return must submit separate Maryland extension applications. - Misconcept 9: Late filing of Form 500E is permissible without consequences.

Submitting Form 500E after the due date can lead to rejection of the extension request, necessitating filing the tax return within ten days or by the original due date, whichever is later, along with full payment of taxes plus accrued interest.

Correcting these misconceptions helps ensure that Maryland Corporations file Form 500E appropriately and comply with state tax regulations, avoiding unnecessary penalties and interest.

Key takeaways

Understanding the Maryland 500E form is essential for businesses operating within the state. Here are some key takeaways to ensure proper completion and use:

- Form 500E serves as an application for extension of time to file the corporation income tax return (Form 500) and to remit any outstanding balance of tax due.

- The form must be filed by entities that are not classified as S corporations or pass-through entities which include specific instructions not to use this form.

- To be eligible for a 6-month automatic extension, the form must be properly filed by the original due date, which is the 15th day of the 3rd month following the close of the tax year or by the original due date required for filing the federal return.

- The application does not extend the time to pay the tax. Any balance due must be fully paid with the submission of Form 500E to avoid penalties and interest.

- If the corporation has not filed an application for extension with the IRS, a valid reason for requesting the extension in Maryland must be provided on Form 500E.

- Ensure the Federal Employer Identification Number (FEIN) is included. If not yet obtained, mark "applied for" and the date of application.

- It's important to report any changes in name or address and to mark the first filing for the corporation if applicable.

- Payment methods include check or money order made payable to the Comptroller of the Treasury, indicating the FEIN, type of tax, and tax year information.

- A proper application for extension of time to file will not be acknowledged, but if an extension request is denied, the tax return must be filed within ten days or by the original due date, whichever is later, along with the full amount of any tax due plus interest.

By following these guidelines when completing and submitting the Maryland Form 500E, corporations can ensure compliance with state tax filing requirements while efficiently managing their tax liabilities.

Common PDF Templates

Maryland Sales and Use Tax - Documentation needed by Maryland retailers to buy items tax-free that will be resold to customers.

Maryland Amended Tax Return - Submit Form 505X to report errors in special deductions allowed to Maryland nonresidents.

Maryland 510d - Special instructions for investment partnerships and manufacturing entities are provided to address specific tax considerations.