Maryland 502Cr PDF Template

The Maryland 502Cr form, an integral document for individuals seeking income tax credits in Maryland, consolidates various tax credits that taxpayers might be eligible for and directly impacts their annual return filing. Its scope covers, among others, tax credits for income taxes paid to other states, child and dependent care expenses, and specific incentives such as the Quality Teacher Incentive, Long-Term Care Insurance Credit, and credits for contributions to preservation and conservation easements. Moreover, it accommodates credits related to aquaculture oyster floats and certain refundable business income tax credits, including neighborhood stabilization and heritage structure rehabilitation tax credits. The form mandates detailed information and the attachment of supplementary documentation to validate the credits claimed, necessitating careful adherence to instructions and completeness. Its structure, consisting of various parts, each related to a distinct type of credit, underscores the state's diverse initiatives to reduce taxpayers’ liabilities while promoting personal and collective benefits such as education, conservation, and community development. The versatility of the 502Cr form embodies Maryland's approach to tax relief, offering a broad spectrum of opportunities for taxpayers to reduce their overall tax burden through credits that reflect wider policy goals. By attaching the 502Cr form to their tax return, residents and part-year residents of Maryland can navigate through complex tax relief options, ensuring compliance and optimizing their financial outcomes. Given its comprehensive nature, understanding the eligibility requirements, applicable credits, and proper form submission procedures is essential for maximizing potential benefits and contributing to the state's socio-economic objectives.

Maryland 502Cr Sample

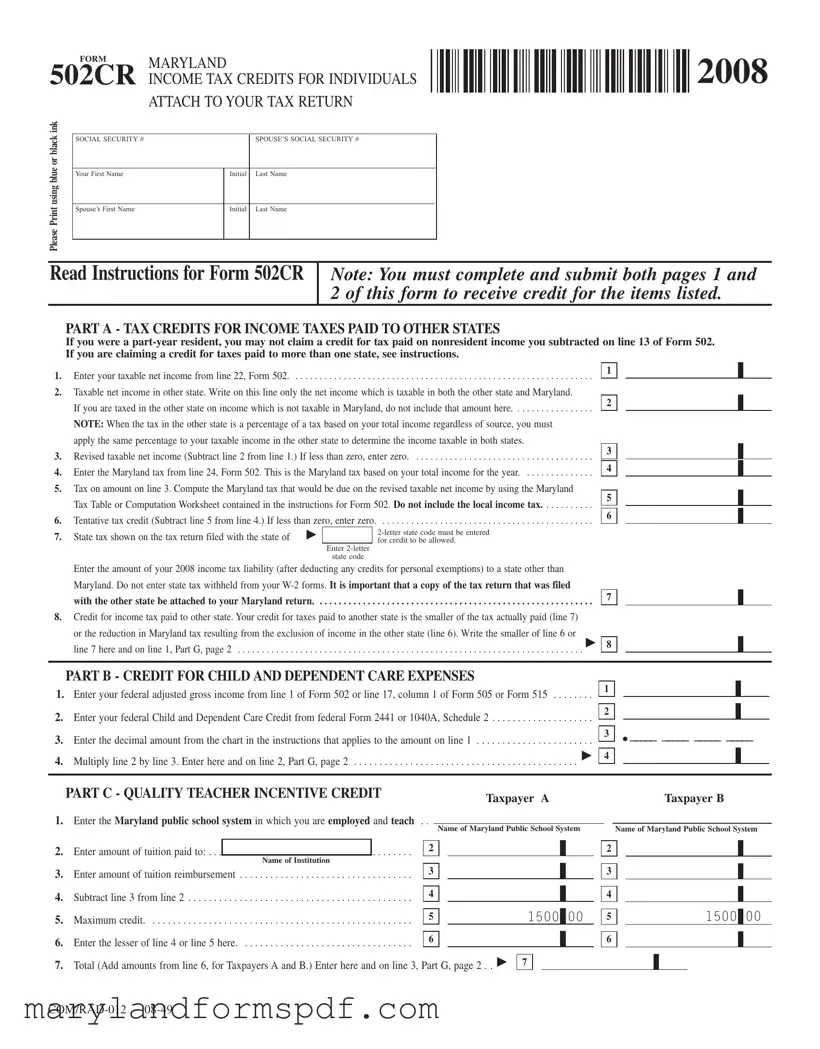

FORMMARYLAND

502CR INCOME TAX CREDITS FOR INDIVIDUALS ATTACH TO YOUR TAX RETURN

2008

2008

ink |

|

|

|

blackor |

SOCIAL SECURITY # |

|

SPOUSE’S SOCIAL SECURITY # |

blueusing |

|

|

|

Your First Name |

Initial |

Last Name |

|

|

|

|

|

Spouse’s First Name |

Initial |

Last Name |

|

|

|

|

|

Please |

|

|

|

|

|

|

Read Instructions for Form 502CR

Note: You must complete and submit both pages 1 and 2 of this form to receive credit for the items listed.

PART A - TAX CREDITS FOR INCOME TAXES PAID TO OTHER STATES

If you were a

1.Enter your taxable net income from line 22, Form 502. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2.Taxable net income in other state. Write on this line only the net income which is taxable in both the other state and Maryland.

If you are taxed in the other state on income which is not taxable in Maryland, do not include that amount here. . . . . . . . . . . . . . . . .

NOTE: When the tax in the other state is a percentage of a tax based on your total income regardless of source, you must apply the same percentage to your taxable income in the other state to determine the income taxable in both states.

3.Revised taxable net income (Subtract line 2 from line 1.) If less than zero, enter zero. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4.Enter the Maryland tax from line 24, Form 502. This is the Maryland tax based on your total income for the year. . . . . . . . . . . . . . .

5.Tax on amount on line 3. Compute the Maryland tax that would be due on the revised taxable net income by using the Maryland

Tax Table or Computation Worksheet contained in the instructions for Form 502. Do not include the local income tax. . . . . . . . . . .

6.Tentative tax credit (Subtract line 5 from line 4.) If less than zero, enter zero. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7. |

State tax shown on the tax return filed with the state of |

▶ |

|

|

|

for credit to be allowed. |

|||

|

|

|

Enter |

|

|

|

|

state code |

|

Enter the amount of your 2008 income tax liability (after deducting any credits for personal exemptions) to a state other than Maryland. Do not enter state tax withheld from your

8.Credit for income tax paid to other state. Your credit for taxes paid to another state is the smaller of the tax actually paid (line 7) or the reduction in Maryland tax resulting from the exclusion of income in the other state (line 6). Write the smaller of line 6 or

▶

line 7 here and on line 1, Part G, page 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

2

3

4

5

6

7

8

PART B - CREDIT FOR CHILD AND DEPENDENT CARE EXPENSES

1. Enter your federal adjusted gross income from line 1 of Form 502 or line 17, column 1 of Form 505 or Form 515 . . . . . . . .

2. Enter your federal Child and Dependent Care Credit from federal Form 2441 or 1040A, Schedule 2 . . . . . . . . . . . . . . . . . . . .

3. Enter the decimal amount from the chart in the instructions that applies to the amount on line 1 . . . . . . . . . . . . . . . . . . . . . . .

▶

4. Multiply line 2 by line 3. Enter here and on line 2, Part G, page 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

2

3

4

._____ _____ _____ _____

|

PART C - QUALITY TEACHER INCENTIVE CREDIT |

|

|

|

|

Taxpayer A |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

1. |

Enter the Maryland public school system in which you are employed and teach . |

. |

|

|

|

|

|

|

|

|

|

|

|

|||

|

Name of Maryland Public School System |

|

||||||||||||||

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Enter amount of tuition paid to: . . . |

|

|

2 |

|

|

|

|

|

|

|

|

|

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

Name of Institution |

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Enter amount of tuition reimbursement |

3 |

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Subtract line 3 from line 2 |

4 |

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

1500 |

|

|

||

5. |

Maximum credit |

5 |

|

|

|

|

|

|

|

00 |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

Enter the lesser of line 4 or line 5 here |

6 |

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7. |

Total (Add amounts from line 6, for Taxpayers A and B.) Enter here and on line 3, Part G, page 2 |

|

▶ |

|

7 |

|

|

|

|

|||||||

. . |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer B

Name of Maryland Public School System

2

3

4

51500 00

6

FORM MARYLAND |

|||

502CR |

INCOME TAX CREDITS FOR INDIVIDUALS |

||

2008 |

|||

|

|

||

|

NAME ________________________________ SSN ________________________ |

||

|

|||

|

|

||

PART D - CREDIT FOR AQUACULTURE OYSTER FLOATS |

|||

1. Enter the amount paid to purchase an aquaculture oyster float(s) |

|||

Enter here and on line 4 of Part G below. This credit is limited. See Instructions |

▶ |

1 |

. . . |

|

Page 2

PART E -

Answer the questions and see instructions below before completing Columns A through E for each person for whom you paid

Question 1 |

- Did the insured individual have |

Yes ☐ |

No ☐ |

Question 2 |

- Is the credit being claimed for the insured individual in this year by any other taxpayer? . . . . |

Yes ☐ |

No ☐ |

Question 3 |

- Has credit been claimed by anyone for the insured individual in any other tax year? |

Yes ☐ |

No ☐ |

If you answered YES to any of the above questions, that insured person does NOT qualify for the credit.

Complete Columns A through D only for insured individuals who qualify for credit. Enter in Column E the lesser of the amount of premium paid for each insured person or:

$310 for those insured that are 40 or less, as of 12/31/08 $500 for those insured that are over age 40, as of 12/31/08.

Add the amounts in Column E and enter the total on line 5 (TOTAL) and Part G, line 5.

|

Column A |

|

Column B |

Column C |

Column D |

Column E |

|

Name of Qualifying Insured Individual |

Age |

Social Security No. of Insured |

Relationship to Taxpayer |

Amount of Premium Paid |

Credit Amount |

1. |

|

▶ |

▶ |

|

▶ |

1. |

|

|

|

|

|

|

|

2. |

|

▶ |

▶ |

|

▶ |

2. |

|

|

|

|

|

|

|

3. |

|

▶ |

▶ |

|

▶ |

3. |

|

|

|

|

|

|

|

4. |

|

▶ |

▶ |

|

▶ |

4. |

|

|

|

|

|

|

|

5. |

TOTAL |

|

|

|

|

5. |

|

|

|

|

|

|

|

PART F - CREDIT FOR PRESERVATION AND CONSERVATION EASEMENTS. JOINT FILERS SEE INSTRUCTIONS

1. |

Enter the total of the current year donation amount, and any carryover from prior year(s) |

. . |

2. |

Enter the amount of any payment received for the easement during 2008 |

. . |

3. |

Subtract line 2 from line 1 |

. . |

4. |

Enter the amount from line 24 of Form 502, line 32c of Form 505 or line 33 of Form 515, or $5,000, whichever is less |

. . |

5. |

Enter the lesser of lines 3 or 4 here and on line 6 of Part G below. (If you itemize deductions, see Instruction 14.) . . . . |

▶ |

. . |

||

6. |

Excess credit carryover. Subtract line 5 from line 3 |

. . |

1

2

3

4

5

6

PART G - INCOME TAX CREDIT SUMMARY

1. Enter the amount from Part A, line 8 (If more than one state, see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2. Enter the amount from Part B, line 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3. Enter the amount from Part C, line 7 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. Enter the amount from Part D, line 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5. Enter the amount from Part E, line 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6. Enter the amount from Part F, line 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

▶

7. Enter the amount from Section 2, line 4 of Form 502H. Attach Form 502H. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

8. Total (Add lines 1 through 7.) Enter this amount on line 27 of Form 502, line 35 of Form 505 or line 36 of Form 515 . . . . . . . . . .

1

2

3

4

5

6

7

8

PART H - REFUNDABLE INCOME TAX CREDITS

▶

1. Neighborhood Stabilization Credit. Enter the amount and attach certification. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

▶

2. Heritage Structure Rehabilitation Tax Credit (See instructions for Form 502H.) Attach certification. . . . . . . . . . . . . . . . . . . . . . . . . .

▶

3. Refundable Business Income Tax Credit (See instructions for Form 500CR) Attach 500CR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

▶

4. IRC Section 1341 Repayment Credit. (See Instructions) Attach documentation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

▶

5. Form 1041 Schedule

6. Total (Add lines 1 through 5.) Enter this amount on line 44 of Form 502, line 47 of Form 505, or line 54 of Form 515. . . . . . . . . .

1

2

3

4

5

6

INSTRUCTIONS FOR FORM 502CR

INCOME TAX CREDITS FOR INDIVIDUALS |

2008 |

GENERAL INSTRUCTIONS

Purpose of Form. Form 502CR is used to claim personal income tax credits for individuals.

You may report the following tax credits on this form: the Credit for Income Taxes Paid to Other States, Credit for Child and Dependent Care Expenses, Quality Teacher Incentive Credit,

The Neighborhood Stabilization Credit, a portion of the Heritage Structure Rehabilitation Tax Credit, certain business tax credits from Form 500CR and the IRC Section 1341 Repayment Credit are refundable. The balance of the Heritage Structure Rehabilitation Tax Credit and all of the other credits may not exceed the state income tax.

Excess credit for preservation and conservation easements and for

Name and Other Information. Type or print the name(s) as shown on Form 502, Form 505 or Form 515 in the designated area. Enter the Social Security number for each taxpayer.

When and Where to File. Form 502CR must be attached to the annual return (Form 502, 505 or 515) and filed with the Comptroller of Maryland, Revenue Administration Division, Annapolis, Maryland

PART A - CREDIT FOR INCOME TAXES PAID TO OTHER STATES

If you are a Maryland resident and you paid income tax to another state, you may be eligible for a credit on your Maryland return. Non- residents (filing Form 505 or Form 515) are not eligible for this credit.

Find the state to which you paid a nonresident tax in the groups listed below. The instructions for that group will tell you if you are eligible for credit and should complete Part A of Form 502CR. You must file your Maryland income tax return on Form 502 and com- plete lines 1 through 24 of that form. Then complete Form 502CR Parts A and G and attach to Form 502.

A completed, signed copy of the income tax return filed in the other state must also be attached to Form 502.

CAUTION: Do not use the income or withholding tax reported on the wage and tax statement

If you are claiming credit for taxes paid to more than one state, a separate Form 502CR must be completed for each state. Total the amount from each Form 502CR, Part A, line 8. Using only one summary section, record the total on Part G, line 1. Credit cannot be allowed for the local portion of the tax calculated on the return of the other state or on the Maryland return (line 31 of Form 502).

GROUP I - Nonreciprocal - Credit is taken on the Maryland resi- dent return.

Alabama - AL |

Kansas - KS |

New Mexico - NM |

Arizona - AZ |

Kentucky - KY |

New York - NY |

Arkansas - AR |

Louisiana - LA |

North Carolina - NC |

California - CA |

Maine - ME |

North Dakota - ND |

Colorado - CO |

Massachusetts - MA |

Ohio - OH |

Connecticut - CT |

Michigan - MI |

Oklahoma - OK |

Delaware - DE |

Minnesota - MN |

Oregon - OR |

Georgia - GA |

Mississippi - MS |

Pennsylvania - PA |

Hawaii - HI |

Missouri - MO |

(except wage income) |

Idaho - ID |

Montana - MT |

Rhode Island - RI |

Illinois - IL |

Nebraska - NE |

South Carolina - SC |

Indiana - IN |

New Hampshire - NH |

Tennessee - TN |

Iowa - IA |

New Jersey - NJ |

Texas - TX |

Utah - UT |

West Virginia - WV |

American Samoa - AS |

Vermont - VT |

(except wage income) |

Guam - GU |

Virginia - VA |

Wisconsin - WI |

Northern Mariana |

(except wage income) |

Territories and |

Island - MP |

Washington, DC - DC |

Possessions of the |

Puerto Rico - PR |

(except wage income) |

United States |

U.S. Virgin Islands - VI |

Group I - A Maryland resident having income from one of these states must report the income on the Maryland resident return Form

502.To claim a credit for taxes paid to the other state, complete Form 502CR and attach it and a copy of the other state’s nonresident income tax return (not just your

GROUP II - Reciprocal for wages, salaries, tips and commission income only.

Pennsylvania - PA |

Washington, DC - DC |

Virginia - VA |

West Virginia - WV |

Group II - Maryland has a reciprocal agreement with the states included in Group II. The agreement applies only to wages, salaries, tips and commissions. It does not apply to business income, farm income, rental income, gain from the sale of tangible property, etc. If you had such income subject to tax in these states, complete Form 502CR and attach it and a copy of the other state’s nonresi- dent income tax return (not just your

If you had wages, plus income other than wages from a state listed in Group II, you should contact the taxing authorities in the other state to determine the proper method for filing the nonresident return.

GROUP III - No state income tax - No credit allowed.

Alaska - AK |

South Dakota - SD |

Florida - FL |

Washington - WA |

Nevada - NV |

Wyoming - WY |

Group III - You must report income from these states on your Mary- land resident return. You cannot claim any credit for income earned in these states because you did not pay any income tax to the other state.

PART A – IMPORTANT NOTE FOR DUAL RESIDENTS

A person may be a resident of more than one state at the same time for income tax purposes. If you must file a resident return with both Maryland and another state, use the following rules to determine where the credit should be taken:

1.A person who is domiciled in Maryland and who is subject to tax as a resident of any of the states listed in Group I or II can claim a credit on the Maryland return (Form 502) using Part A of Form 502CR.

2.A person domiciled in any state listed in Group I or II who must file a resident return with Maryland must take the credit in the state of domicile.

PART A – SPECIAL INSTRUCTIONS

Members of

If the Maryland resident must file an individual nonresident return reporting the partnership, S corporation, LLC or business trust income, a separate Form 502CR must be completed for each state and submitted with a copy of the return filed with the other state. For both composite returns and individual returns, no credit is avail- able for taxes paid to states in Group III, or for taxes paid to cities or local jurisdictions.

Shareholders of S Corporations - Maryland resident shareholders can claim a credit for taxes paid by an S corporation to a state which does not recognize federal S corporation treatment. A copy of the corporation return filed in the other state is required to be attached to the Maryland return. A separate Form 502CR should be completed for each state showing the following information:

_______________% x_______________ =________________________

Stock ownership |

Corporation taxable Line 2, Part A, Form 502CR |

percentage |

income |

_______________% x_______________ =________________________

Stock ownership Corporation tax |

Line 7, Part A, Form 502CR |

percentage |

|

NOTE: A preliminary calculation using Form 502 must be made before calculating the credit on Form 502CR. Complete lines 1 through 24 on Form 502 to determine the amounts to be used for the 502CR computation.

The credit amount shown on line 8 of Part A, Form 502CR must then be included as an addition to income on line 5 of the Form 502 you will file.

D.C. Unincorporated Business Franchise Tax -

Installment Sales in Another State - You may be eligible for cred- it for taxes paid to another state for gain recognized on installment sales proceeds, even if the other state required that the total gain be recognized in an earlier tax year. Credit is allowed against the state income tax only. The gain must have been deferred for feder- al tax purposes, but fully taxed in the year of the sale by another state that does not recognize the deferral. The credit allowed is the amount of the gain taxed in Maryland in the current year multiplied by the lesser of:

•the highest state tax rate used on your Maryland tax return or

•the tax rate imposed by the other state on the gain.

PART B - CREDIT FOR CHILD AND DEPENDENT CARE EXPENSES

If you were eligible for a Child and Dependent Care Credit on your federal income tax return, Form 1040 or 1040A for tax year 2008, you may be entitled to a credit on your Maryland state income tax return. The credit starts at 32.5% of the federal credit allowed, but is phased out for taxpayers with federal adjusted gross incomes above $41,000 ($20,500 for individuals who are married, but file separate income tax returns). No credit is allowed for an individual whose federal adjusted gross income exceeds $50,000 ($25,000 for married filing separately). Use the chart below to determine the decimal amount to be entered on line 3 of Part B.

PART C - QUALITY TEACHER INCENTIVE CREDIT

If you are a Maryland teacher, you may be able to claim a credit against your State tax liability for tuition paid to take

a. currently hold a standard professional certificate or advanced professional certificate;

b. are employed by a county/city board of education in Maryland;

c. teach in a public school and receive a satisfactory performance evaluation for teaching;

d. successfully complete the courses with a grade of B or better; and

e. have not been fully reimbursed by the county/city for these expenses. Only the unreimbursed portion qualifies for the credit.

Each spouse that qualifies may claim this credit. Complete a sepa- rate column in the worksheet for each spouse.

INSTRUCTIONS

Line 1. Enter the name of the Maryland public school system in which you are employed and teach.

Line 2. Enter the amount of tuition paid for

Line 3. Enter the amount received as a reimbursement for tuition from your employer.

Line 5. The maximum amount of credit allowed is $1,500 for each qualifying individual.

Line 6. The credit is limited to the amount paid less any reimburse- ment up to the maximum amount allowed for each qualify- ing individual. Enter the lesser of line 4 or line 5.

Line 7. Enter the total of line 6, for Taxpayers A and B. Also enter this amount on line 3, Part G.

CREDIT FOR CHILD AND

DEPENDENT CARE EXPENSES CHART

If your filing status is Married Filing Separately |

Decimal Amount |

For all other filing statuses, if your federal |

||

and your federal adjusted gross income is: |

|

adjusted gross income is: |

||

|

|

|

|

|

At Least |

But less than |

|

At least |

But less than |

$0- |

$20,501 |

.3250 |

$0 |

$41,001 |

$20,501 |

$21,001 |

.2925 |

$41,001 |

$42,001 |

|

|

|

|

|

$21,001 |

$21,501 |

.2600 |

$42,001 |

$43,001 |

$21,501 |

$22,001 |

.2275 |

$43,001 |

$44,001 |

$22,001 |

$22,501 |

.1950 |

$44,001 |

$45,001 |

$22,501 |

$23,001 |

.1625 |

$45,001 |

$46,001 |

|

|

|

|

|

$23,001 |

$23,501 |

.1300 |

$46,001 |

$47,001 |

$23,501 |

$24,001 |

.0975 |

$47,001 |

$48,001 |

|

|

|

|

|

$24,001 |

$24,501 |

.0650 |

$48,001 |

$49,001 |

$24,501 |

$25,001 |

.0325 |

$49,001 |

$50,001 |

$25,001 |

OR OVER |

.0000 |

$50,001 |

OR OVER |

|

|

|

|

|

PART D - CREDIT FOR AQUACULTURE OYSTER FLOATS

A credit is allowed for 100% of the amounts paid to purchase a new aquaculture oyster float that is designed to grow oysters at or under an individual homeowner’s pier. The device must be buoyant and assist in the growth of oysters for the width of the pier. The credit cannot exceed $500. In the case of a joint return, each spouse is entitled to claim the credit, provided each spouse purchases or contributes to the purchase of a float.

PART E -

A

A credit may not be claimed if:

a. the insured was covered by LTC insurance prior to July 1, 2000;

b. the credit for the insured is being claimed in this year by another taxpayer; or

c. the credit is being or has been claimed by anyone in any other tax year.

The credit is equal to the LTC premiums paid with a maximum per insured of:

Amount |

Age of Insured as of 12/31/08 |

$310 |

40 or less |

$500 |

over 40 years |

SPECIFIC INSTRUCTIONS

•Answer Questions 1 through 3. If you answered “yes” for any of the questions, no credit is allowed for that individual.

•Complete columns A through D of the worksheet for each qualifying insured individual who qualifies for the credit. If more space is required, attach a separate statement.

•Enter in Column E the amount of premiums paid for each qualifying insured individual up to the maximum for that age group.

•Add the amounts in Column E and enter the total on line 5. Also enter this amount on line 5, Part G.

PART F - CREDIT FOR PRESERVATION AND

CONSERVATION EASEMENTS

If you donated an easement to the Maryland Environmental Trust or the Maryland Agricultural Land Preservation Foundation to preserve open space, natural resources, agriculture, forest land, watersheds, significant ecosystems, viewsheds or historic prop- erties, you may be eligible for a credit if:

1.the easement is perpetual;

2.the easement is accepted and approved by the Board of Public Works; and

3.the fair market value of the property before and after the conveyance of the easement is substantiated by a certified real estate appraiser.

The credit is equal to the difference in the fair market values of the property reduced by payments received for the easement.

If the property is owned jointly by more than one individual such as a husband and wife, each individual owner is entitled to the credit based on their percentage of ownership. Individual members of a

You can use the rules for filing separate returns in Instruction 8 in the Resident booklet to calculate each spouse’s Maryland tax.

If the individual’s allowable credit amount exceeds the maximum of $5,000 the excess may be carried forward for up to 15 years or until fully used. Complete lines

For Line 1, enter the amount by which the fair market value of the property before the conveyance of the easement exceeds the fair market value after the conveyance as substantiated by a certified real estate appraiser, plus any carryover from the prior year.

The carryover amount can be found on Part F line 6 of Form 502CR for tax year 2007.

For additional information, contact the Maryland Environmental Trust at

PART G - INCOME TAX CREDIT SUMMARY

This part is to summarize parts A through F and the

PART H - REFUNDABLE INCOME TAX CREDITS

Line 1 - NEIGHBORHOOD STABILIZATION CREDIT

If you live in the Waverly or Landsdowne sections of Baltimore City, or in the Hillendale, Northbrook, Pelham Woods, or Tay- lor/Dartmouth areas of Baltimore County, you may qualify for this credit. Credit for homes purchased in Baltimore City must have been applied for by December 31, 2002. Credit for homes purchased in Baltimore County must have been applied for by December 31, 2005. After certification by Baltimore City or Bal- timore County, you may claim an income tax credit equal to the property tax credit granted by Baltimore City or Baltimore Coun- ty. Enter the amount on line 1 of Part H and attach a copy of the certification.

Line 2 - HERITAGE STRUCTURE REHABILITATION TAX CREDIT

See instructions for Form 502H.

Line 3 - REFUNDABLE BUSINESS INCOME TAX CREDIT

Development Tax Credit and the Biotechnology Investment Incentive Tax Credit.

Line 4 - IRC SECTION 1341 REPAYMENT CREDIT

If you repaid an amount reported as income on a prior year tax return this year that was greater than $3,000, you may be eligible for an IRC Section 1341 Repayment credit. Attach docu- mentation. For additional information, see Administrative Release 40.

Line 5 - FORM 1041 SCHEDULE

If you are the beneficiary of a Trust or a Qualified Subchapter S Trust for which nonresident PTE tax was paid, you may be enti- tled to a credit for your share of that tax. Enter the amount on this line and attach both the Form 1041 Schedule

Line 6 - Add lines 1 through 5 and enter the total on the appro- priate line of the income tax form being filed.

Free iFile visit us at www.marylandtaxes.com

File Breakdown

| Fact Name | Description |

|---|

Steps to Filling Out Maryland 502Cr

The Maryland 502CR form is a crucial document for individuals looking to claim various income tax credits on their Maryland tax return. It may encompass credits for taxes paid to other states, child and dependent care expenses, and many others. Proper completion and submission of both pages of this form are integral to receiving these credits. To assist you in navigating through this form accurately, here are detailed steps for completing it.

- Part A - Tax Credits for Income Taxes Paid to Other States:

- Locate your taxable net income from line 22 on Form 502 and enter it.

- Input the taxable net income that is taxed in both Maryland and the other state(s).

- Calculate your revised taxable net income by subtracting line 2 from line 1, input the result or 0 if it's less.

- Enter the Maryland tax amount from line 24 on Form 502.

- Compute the Maryland tax due on the revised taxable net income using the Maryland Tax Table or Worksheet provided in Form 502 instructions and input it.

- Determine the tentative tax credit by subtracting line 5 from line 4.

- Input the state tax amount from your tax return filed with the other state(s) and provide the 2-letter state code.

- Calculate your credit for income tax paid to another state - the smaller of line 6 or line 7. Input this on line 8.

- Part B - Credit for Child and Dependent Care Expenses:

- Enter your federal adjusted gross income from Form 502 or its equivalents.

- Input the federal Child and Dependent Care Credit from your federal Form.

- Refer to the chart in instructions and enter the decimal that corresponds to your income range.

- Multiply line 2 by line 3 for your total credit and input it.

- Part C - Quality Teacher Incentive Credit:

- Write the name of the Maryland public school system where you teach.

- Enter the amount of tuition paid for qualifying courses.

- Input any tuition reimbursement received.

- Subtract line 3 from line 2 for the net qualifying expenses.

- The maximum credit allowed is $1,500. Enter this or the result from line 4, whichever is lesser.

- Add the amount for Taxpayers A and B if applicable and input the total.

- Part D - Credit for Aquaculture Oyster Floats:

- Enter the amount paid for purchasing new aquaculture oyster float(s).

- Part E - Long-Term Care Insurance Credit:

- Answer the qualifying questions and fill in the worksheet following the specific instructions provided.

- Part F - Credit for Preservation and Conservation Easements:

- Input the total of the current year donation amount and any carryover from prior years.

- Enter any payment received for the easement during the tax year.

- Subtract line 2 from line 1 for the credit amount before limitations.

- Input the lesser of the difference from line 3 or $5,000, or your tax due, whichever is less.

- If there's excess credit, calculate and input the carryover amount.

- Part G - Income Tax Credit Summary:

- Through 7: Summarize the amounts from Parts A through F, and any other credits you're claiming, accurately tallying and inputting the totals.

- Part H - Refundable Income Tax Credits:

- List any applicable refundable credits, like the Neighborhood Stabilization Credit, and input the qualifying amounts.

When your form is completed, double-check all the information for accuracy. Ensure to attach Form 502CR to your Maryland tax return along with any required documentation, such as copies of tax returns filed in other states or receipts for qualified expenses. Submitting an accurate and complete form is essential for the timely processing of your income tax credits.

More About Maryland 502Cr

What is the Form 502CR in Maryland?

The Form 502CR is designed for Maryland residents to claim various personal income tax credits. These credits may include those for taxes paid to other states, childcare and dependent expenses, quality teacher incentives, long-term care insurance premiums, and several others. It must be submitted alongside the Maryland tax return.

Who can use Form 502CR?

Individuals who may be eligible for any of the listed tax credits on the form can use Form 502CR. This includes Maryland residents who have paid income tax to another state, paid for child and dependent care, are qualified teachers, or have invested in long-term care insurance, among other eligible credits.

How does the credit for taxes paid to other states work?

If you are a Maryland resident and have paid income taxes to another state, you may be eligible for a credit on your Maryland tax return. This credit prevents double taxation of the same income. It's calculated based on the lesser of the tax paid to the other state or the amount of Maryland tax attributable to the income taxed by the other state.

Can non-residents file Form 502CR?

No, non-residents (filing Form 505 or Form 515) are not eligible for the credits provided by Form 502CR. This form is specifically designed for Maryland residents.

How do I claim the credit for childcare and dependent care expenses?

To claim this credit, you must first qualify for the Child and Dependent Care Credit on your federal income tax return. The amount of credit on your Maryland return starts at 32.5% of the federal credit and is phased out for higher income levels, with no credit for individuals earning above a certain threshold.

What is the Quality Teacher Incentive Credit?

This credit is available to Maryland teachers who pay for graduate-level courses required for certification. Teachers must meet specific criteria, including employment by a Maryland public school system and a satisfactory performance evaluation. The credit covers unreimbursed tuition expenses up to a certain maximum.

How do I claim the Long-Term Care Insurance Credit?

You can claim this credit for premiums paid on qualifying long-term care insurance policies for yourself or certain family members. There are caps based on the age of the insured individual. Specific conditions must be met to qualify, including residency in Maryland for the insured.

What are the requirements for the Credit for Preservation and Conservation Easements?

This credit applies if you donated an easement to preserve land, natural resources, or historic properties in Maryland. The easement must be perpetual and approved by the state. The credit equals the difference in the property's fair market value before and after the easement, up to a limit, with provisions for carryover.

What is included in the Refundable Income Tax Credits section of Form 502CR?

This section covers credits like the Neighborhood Stabilization Credit, the Heritage Structure Rehabilitation Tax Credit, and the Refundable Business Income Tax Credit among others. These credits are refundable, meaning they can provide a refund beyond your tax liability. Documentation and certifications may be required to claim these credits.

Common mistakes

-

Filling out the form in an ineligible color of ink. The form specifies to use black or blue ink, yet some individuals use other colors, potentially leading to processing delays or unreadability.

-

Incorrectly calculating taxable net income to claim the Credit for Income Taxes Paid to Other States. Some people mistakenly include income not taxable in Maryland, thereby inflating the value of their credit.

-

Omitting important documentation. To verify claims, especially for taxes paid to other states or for credits like the Quality Teacher Incentive Credit, attached documentation is required. Failure to include these documents can lead to credit denial.

-

Using incorrect Social Security numbers. Accurately entering Social Security numbers is crucial for processing, and mistakes can result in significant delays or misattribution of filings.

-

Not completing both pages of the form. Some filers overlook the requirement to complete and submit both pages, which is necessary to receive credit.

-

Misinterpreting the Long-Term Care Insurance Credit eligibility, particularly regarding pre-2000 policies or policies claimed by another taxpayer or in another tax year. Misunderstandings of these rules can result in incorrect claims.

-

Failing to correctly apply the decimal amount for the Child and Dependent Care Expense Credit. This amount is contingent upon adjusted gross income and requires careful attention to the provided chart to ensure accuracy.

-

Entering the wrong amount for the Child and Dependent Care Expenses Credit. Some individuals incorrectly calculate or miswrite the credit amount from their federal return, leading to discrepancies.

-

Not adhering to the specific qualifications for credits, such as the Quality Teacher Incentive Credit or the Credit for Aquaculture Oyster Floats. Each credit has unique requirements, and overlooking these details can result in unallowed credits.

Documents used along the form

Filing taxes can sometimes feel overwhelming due to the number of documents needed, especially when applying for specific tax credits. Understanding the accompanying forms for the Maryland 502CR form helps streamline the process. The Maryland 502CR form is primarily used to apply for income tax credits, including credits for taxes paid to other states and credits for child and dependent care expenses.

- Maryland Form 502: As the main personal income tax return form for Maryland residents, this is essential for calculating your total income, deductions, and credits before applying specifics from the 502CR. It provides the baseline figures that the 502CR adjustments are applied to.

- Form 2441 or 1040A Schedule 2: These federal forms are used to calculate the Child and Dependent Care Credit at the federal level. The information from these forms is needed for Part B of the 502CR to calculate the corresponding state credit.

- State Income Tax Return(s) from Other States: If you are claiming a credit for taxes paid to another state on the 502CR form, you must attach a copy of the tax return(s) filed with that state. This documentation is necessary to verify the taxes paid and ensure the correct credit amount on your Maryland return.

- Form 500CR: For businesses, this form is used to claim various Maryland business income tax credits. It's relevant for individuals as some business credits, like the Refundations Bonus Income Tax Credit, can pass through to individual owners or members and may be claimed on the individual's 502CR form.

Each of these documents serves its specific purpose in ensuring the Maryland 502CR form is filled out accurately, helping individuals and businesses in Maryland obtain the tax credits they're eligible for. Giving attention to these supporting documents can make the process smoother and potentially more beneficial financially.

Similar forms

The Maryland 502Cr form is similar to the Federal Form 2441, Child and Dependent Care Expenses, in its functionality for claiming child and dependent care credits. Both forms allow individuals to claim a tax credit for expenses incurred in the care of qualifying individuals, typically children or dependent adults, to enable the taxpayer (and spouse, if filing jointly) to work or actively look for work. Federal Form 2441 calculates the credit based on expenses paid towards the care of the qualifying individual and applies a percentage based on the taxpayer's adjusted gross income to determine the credit amount. Similarly, the Maryland 502CR takes into account child and dependent care expenses for state tax credit calculation, allowing taxpayers to reduce their state tax liability based on a portion of their federal credit adjusted for income levels.

Another document resembling the Maryland 502CR is the Form 500CR, Maryland Business Income Tax Credits, in regards to offering tax credits, albeit for different purposes and audiences. Form 500CR is aimed at businesses seeking tax credits for various activities, including job creation, research and development, and investment in Maryland. In contrast, Form 602CR provides personal income tax credits to individuals. Both forms supplement the main tax return document with the specific mechanism for calculating and claiming respective credits. While the target and specific credits differ, the resemblance lies in their supplementary role in the tax filing process, enabling both businesses and individuals to claim applicable credits, thereby potentially reducing their tax liabilities.

Dos and Don'ts

When filling out the Maryland 502CR form, it's important to follow specific guidelines to ensure that you correctly claim your eligible income tax credits. Below are five things you should do and five things you shouldn't do when completing this form.

Things You Should Do:

Read the instructions carefully before starting to fill out the form to ensure you understand the eligibility requirements for the tax credits.

Use black or blue ink for clarity and legibility, which helps prevent processing errors or delays.

Ensure you complete and attach both pages 1 and 2 of the form to your tax return to avoid missing out on any credits.

Attach a copy of the tax return filed with the other state when claiming a credit for income taxes paid to other states, as required for validation.

Correctly calculate the credit for child and dependent care expenses, quality teacher incentive credit, and any other applicable credits by following the specific instructions provided for each section.

Things You Shouldn't Do:

Do not leave any sections that apply to you incomplete. Failing to provide required information could result in the denial of eligible credits.

Avoid guessing when it comes to figures or information requested. Use exact numbers from your financial documents and prior state returns.

Do not include income that is not taxable in Maryland when calculating the credit for taxes paid to other states.

Do not forget to enter the 2-letter state code when claiming a credit for taxes paid to other states, as failing to do so could disqualify you from receiving the credit.

Avoid omitting documentation such as receipts for child and dependent care expenses, tuition payments for quality teacher incentives, or proof of purchase for aquaculture oyster floats.

By adhering to these guidelines, you can ensure that your Maryland 502CR form is properly filled out and submitted, maximizing your potential tax credits while complying with state tax laws.

Misconceptions

There are several common misconceptions regarding the Maryland 502CR form, a crucial document for individuals seeking to claim various income tax credits in the state of Maryland. Here is a clarification of four such misconceptions:

- Misconception 1: The credit for taxes paid to other states is unlimited.

In reality, the credit for taxes paid to other states, as outlined in Part A of the 502CR form, has limitations. It is restricted to the smaller amount between the tax actually paid to the other state or the proportion of Maryland tax attributable to the income taxed by the other state. This ensures that the credit does not exceed Maryland's tax liability on the same income.

- Misconception 2: The 502CR form is only for claiming credits for income taxes paid to other states.

Contrary to this belief, the Maryland 502CR form is used to claim various personal income tax credits, not just the credit for income taxes paid to another state. It includes credits such as the Child and Dependent Care Expenses Credit, Quality Teacher Incentive Credit, Long-Term Care Insurance Credit, among others.

- Misconception 3: If you did not owe any income tax in the other state, there is no need to complete Part A of the 502CR form.

This is incorrect. Part A needs to be completed to determine the credit for income taxes paid to other states, even if no tax was paid. This section helps to identify the portion of income subject to tax in both Maryland and the other state, which can affect the calculation of the Maryland tax liability.

- Misconception 4: All tax credits claimed on form 502CR are refundable.

Not all tax credits listed on the Maryland 502CR form are refundable. While it includes refundable credits like the Neighborhood Stabilization Credit and certain business tax credits from Form 500CR, many of the credits provided are non-refundable. Non-refundable tax credits can only reduce the tax liability to zero and cannot result in a refund.

Understanding these aspects of the Maryland 502CR form is essential for accurately claiming and maximizing the benefits of available income tax credits.

Key takeaways

The Maryland 502CR form is intended for individuals claiming personal income tax credits. It encompasses various credits, including income taxes paid to other states, child and dependent care expenses, and long-term care insurance credits, among others.

- The form must be completed in full and attached to your tax return to be eligible for any credits.

- For credits regarding taxes paid to other states, both pages 1 and 2 of the form need to be submitted.

- Part-year Maryland residents cannot claim credits for tax paid on income from other states that isn’t taxable in Maryland.

- If claiming credit for taxes paid to multiple states, separate calculations are required for each state.

- Maryland residents are eligible for a credit for taxes paid to other states; however, nonresidents filing Maryland taxes cannot claim this credit.

- Credits for child and dependent care expenses depend on your federal adjusted gross income, with specific calculations provided for Maryland tax purposes.

- The Quality Teacher Incentive Credit is designed for Maryland public school teachers paying for graduate-level courses necessary for certification, contingent on several eligibility factors, including not being fully reimbursed for these expenses.

- There's a one-time Long-Term Care Insurance Credit available for payments made on qualifying insurance premiums, with the amount based on age and premium paid, subject to certain exclusions.

- The Heritage Structure Rehabilitation Tax Credit, among others listed, is refundable, whereas other credits may reduce your state tax liability but are not refundable themselves. Excess credit for certain non-refundable credits may carry over to the next tax year.

It is crucial that you attach a copy of the tax return filed in the other state when claiming credit for taxes paid to that state. Also, all relevant information, such as names and Social Security numbers, should be printed clearly, using black or blue ink.

For particular credits, like the credit for child and dependent care expenses and the long-term care insurance credit, specific eligibility criteria based on income or other conditions apply. Calculations for these credits must align with the guidelines provided within the instructions for Form 502CR.

Individuals claiming the credit for preservation and conservation easements must satisfy certain requirements, such as the easement being perpetual and accepted and approved by the Maryland Board of Public Works. The credit calculated should reflect the decrease in fair market value of the property due to the easement.

In summary, properly filling out the Maryland 502CR form involves careful attention to eligibility requirements, accurate calculation of credit amounts, and adherence to filing instructions, including attaching additional documentation as necessary.

Common PDF Templates

Maryland Anatomy Board - By filling out the Maryland Anatomy form, donors provide invaluable resources that support advancements in surgical techniques, disease treatment, and medical education.

Maryland State Compliance Application - Specific testing areas like Forensic Toxicology and Immunology are addressed in Schedule A.