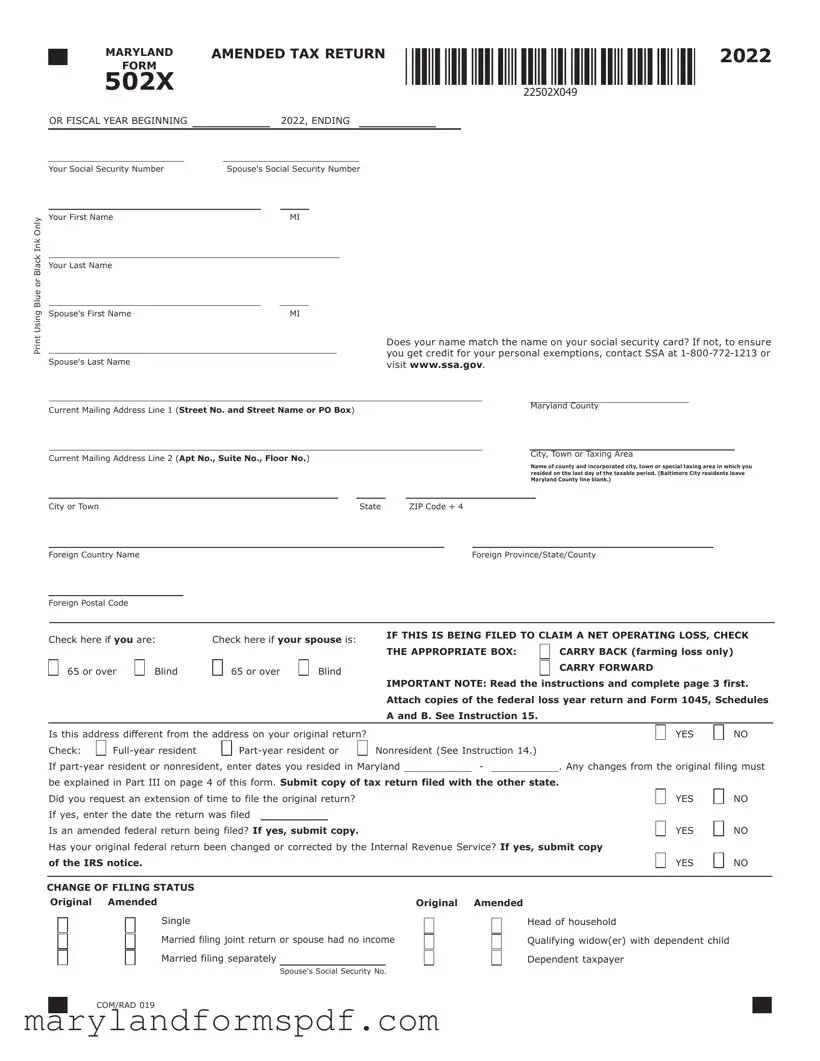

Maryland 502X PDF Template

When life throws us a curveball, sometimes we need to revisit the past – and that includes reviewing our tax returns. The Maryland 502X form is the lifesaver for residents who find themselves in such a situation, specifically tailored for those needing to amend their previously filed state income tax returns for the year 2020 or other fiscal years starting in 2020. Whether it's because of an overlooked deduction, a change in filing status, or a correction mandated by the Internal Revenue Service, this form is your go-to resource for setting the record straight. It requires meticulous attention to detail, as filers must indicate all changes from their original submission and attach any necessary documentation, such as a revised federal return or notices from the IRS. Moreover, the 502X form isn't just about correcting errors; it’s also a gateway for claiming net operating losses, adjusting to new information, or aligning state records after a federal amendment. With strict requirements on ink color for printing and comprehensive fields covering everything from personal information to income, deductions, and credits, the process demands precision. Additionally, Maryland places a strong emphasis on electronic filing, offering a streamlined way to manage amendments related to business income tax credits. Keep in mind, timeliness is crucial, as amendments are subject to audit and specific deadlines govern the filing window, based on the original due date, payments made, and other criteria. As every seasoned taxpayer knows, the devil is in the details – and navigating the complexities of the Maryland 502X form is a testament to that.

Maryland 502X Sample

|

MARYLAND |

AMENDED TAX RETURN |

2022 |

|||

|

FORM |

|||||

|

|

|

|

|

|

|

|

502X |

|

|

|

|

|

OR FISCAL YEAR BEGINNING |

|

2022, ENDING |

|

|||

|

|

|

|

|

|

|

Print Using Blue or Black Ink Only

Your Social Security Number

Your First Name

Your Last Name

Spouse's First Name

Spouse's Last Name

Spouse's Social Security Number

MI

MI

Does your name match the name on your social security card? If not, to ensure you get credit for your personal exemptions, contact SSA at

Current Mailing Address Line 1 (Street No. and Street Name or PO Box) |

|

|

|

|

|

|

|

Maryland County |

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current Mailing Address Line 2 (Apt No., Suite No., Floor No.) |

|

|

|

|

|

|

|

|

|

|

|

City, Town or Taxing Area |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of county and incorporated city, town or special taxing area in which you |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

resided on the last day of the taxable period. (Baltimore City residents leave |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Maryland County line blank.) |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or Town |

|

|

|

|

|

|

|

|

|

State |

ZIP Code + 4 |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Foreign Country Name |

|

|

|

|

|

|

|

|

|

|

|

|

Foreign Province/State/County |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign Postal Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Check here if you are: |

Check here if your spouse is: |

|

IF THIS IS BEING FILED TO CLAIM A NET OPERATING LOSS, CHECK |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

THE APPROPRIATE BOX: |

|

|

CARRY BACK (farming loss only) |

|

|||||||

65 or over |

Blind |

65 or over |

Blind |

|

|

|

|

|

|

|

|

|

CARRY FORWARD |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

IMPORTANT NOTE: Read the instructions and complete page 3 first. |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

Attach copies of the federal loss year return and Form 1045, Schedules |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

A and B. See Instruction 15. |

|

||||||||||

Is this address different from the address on your original return? |

|

|

|

|

|

|

|

YES |

NO |

|||||||||||||

Check: |

Nonresident (See Instruction 14.) |

|

||||||||||||||||||||

If |

|

- |

|

|

. Any changes from the original filing must |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

be explained in Part III on page 4 of this form. Submit copy of tax return filed with the other state. |

|

|||||||||||||||||||||

Did you request an extension of time to file the original return? |

|

|

|

|

|

|

|

|

|

YES |

NO |

|||||||||||

If yes, enter the date the return was filed |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Is an amended federal return being filed? If yes, submit copy. |

|

|

|

|

|

|

|

|

|

YES |

NO |

|||||||||||

Has your original federal return been changed or corrected by the Internal Revenue Service? If yes, submit copy

of the IRS notice.

YES

NO

CHANGE OF FILING STATUS

Original Amended

Single

Married filing joint return or spouse had no income

Married filing separately

Spouse's Social Security No.

Original Amended

Head of household

Qualifying widow(er) with dependent child

Dependent taxpayer

COM/RAD 019

|

|

MARYLAND |

AMENDED TAX RETURN |

|

2022 |

||||

|

|

|

FORM |

|

|||||

|

|

|

|

|

|

|

|

Page 2 |

|

|

|

502X |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||

LAST NAME |

|

|

|

SSN |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A. As originally reported or |

B. Net change – increase |

C. Corrected amount. |

|

|

|

|

|

|

|

as previously adjusted |

or (decrease) – |

|

|

|

|

|

|

|

|

(See instructions.) |

explain on page 4. |

|

|

1. Federal adjusted gross income. . . . . . . . . . . . . . . . . . . . .1.

1a. Earned income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1a.

2. Additions to income (from lines 2, 3, 4, and 5 of 502). . . .2.

3. Total (Add lines 1 and 2). . . . . . . . . . . . . . . . . . . . . . . . .3.

4.Subtractions from income (from lines 8 through 14 of 502).4.

5. Total Maryland adjusted gross income . . . . . . . . . . . . . . .5.

6.CHECK ONLY ONE METHOD (See Instruction 5.)

STANDARD DEDUCTION METHOD

STANDARD DEDUCTION METHOD

Enter 15% (See Instruction 5 for limits.)

ITEMIZED DEDUCTION METHOD

ITEMIZED DEDUCTION METHOD

Enter total MD itemized deductions from Part II,

on page 4. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6. 7. Net income (Subtract line 6 from line 5.) . . . . . . . . . . . . .7.

8. Exemption amount (See Instruction 5.) . . . . . . . . . . . . . .8.

9. Taxable net income (Subtract line 8 from line 7.) . . . . . . .9.

10.Maryland tax (from Tax Table or Computation Worksheet).10.

10a. Credits: Earned Income Credit. .

Poverty Level Credit . .

Personal Credit. . . . . .

Business Credit. . . . . .

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

Enter total credits. . . . . . . . . . . . . . . . . . . . . . 10a. 10b. Maryland tax after credits (Subtract line 10a from

line 10.) If less than 0, enter 0 . . . . . . . . . . . . . . . . . . 10b.

11.Local income tax (Use rate applicable for year of return.)

Multiply line 9 by . (See Instruction 7.). . . . . . . 11.

11a. Local credits: Earned Income Credit. . Poverty Level Credit. . .

Personal Credit. . . . . .

Enter total credits. . . . . . . . . . . . . . . . . .11a. 11b. Local tax after credits (Subtract line 11a from line 11.)

If less than 0, enter 0. . . . . . . . . . . . . . . . . . . . . . . . . 11b.

12.Total Maryland and local income tax

(Add lines 10b and 11b.) |

. . . . 12 |

|

|

||

13. Contribution: A. |

|

B. |

|

|

|

C. |

|

D. |

|

|

|

Enter total contributions (See Instruction 8.). . . . . . . . . . 13.

14.Total Maryland income tax, local income tax and

contribution (Add lines 12 and 13.) . . . . . . . . . . . . . . . . 14.

15. Total Maryland tax withheld. . . . . . . . . . . . . . . . . . . . . . 15.

16.Estimated tax payment, extension and payments made with

Form MW506NRS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16.

17. Refundable earned income credit . . . . . . . . . . . . . . . . . . 17.

18. Nonresident tax paid by

19.Refundable income tax credits

(Attach Form 502CR and/or 502S.) . . . . . . . . . . . . . . . . 19.

20. Total payments and credits (Add lines 15 through 19.) . . 20.

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

COM/RAD 019

|

MARYLAND |

AMENDED TAX RETURN |

||||

|

|

FORM |

|

|

|

|

|

|

|

|

|

||

|

502X |

|

|

|

|

|

LAST NAME |

|

SSN |

||||

|

|

|

|

|

|

|

21. Balance due (if line 14 is more than line 20). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.

22. Overpayment (if line 14 is less than line 20). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22.

23.Tax paid with original return, plus additional tax paid after it was filed (Do not include any interest or penalty.) 23.

24. Prior overpayment (Total all refunds previously issued.). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24.

25.REFUND (If line 21 is less than 23, subtract line 21 from 23.) (If line 24 is less than 22,

subtract line 24 from 22.) (Add lines 22 and 23.) (See Instruction 10.). . . . . . . . . . . . . . . . . . . . . . . REFUND 25.

26.BALANCE DUE (If line 21 is more than 23, subtract line 23 from 21.) (Add line 21 to 24.)

|

(If line 22 is less than 24, subtract line 22 from 24.) (See Instruction 10.) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

26. |

27. |

Interest and/or penalty charges on tax due and/or from Form 502UP (See Instruction 11.) |

27. |

|

28. |

TOTAL AMOUNT DUE (Add line 26 and line 27.) |

PAY IN FULL WITH THIS RETURN 28. |

|

2022

Page 3

.00

.00

.00

.00

.00

.00

.00

.00

I. INCOME AND ADJUSTMENTS TO INCOME: You must complete the following using the amounts from your federal income tax return. If there

are no changes to the amounts claimed on your original Maryland return, check here

and complete Column A and line 17 of Column C.

and complete Column A and line 17 of Column C.

INCOME AND ADJUSTMENTS INFORMATION (See Instruction 4.) 1. Wages, salaries, tips, etc. . . . . . . . . . . . . . . . . . . . . . . . .1.

2. Taxable interest income . . . . . . . . . . . . . . . . . . . . . . . . .2.

3. Dividend income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3.

4.Taxable refunds, credits or offsets of state and local

income taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4.

5. Alimony received . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5.

6. Business income or (loss) . . . . . . . . . . . . . . . . . . . . . . . .6.

7. Capital gain or (loss). . . . . . . . . . . . . . . . . . . . . . . . . . . .7.

8. Other gains or (losses) (from federal Form 4797) . . . . . . .8.

9.Taxable amount of pensions, IRA distributions,

and annuities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9.

10.Rents, royalties, partnerships, estates, trusts, etc.

(Circle appropriate item.) . . . . . . . . . . . . . . . . . . . . . . . 10.

11. Farm income or (loss). . . . . . . . . . . . . . . . . . . . . . . . . . 11.

12. Unemployment compensation. . . . . . . . . . . . . . . . . . . . . 12.

13.Taxable amount of Social Security and

Tier 1 Railroad Retirement benefits . . . . . . . . . . . . . . . . 13.

14.Other income (including lottery or other

gambling winnings). . . . . . . . . . . . . . . . . . . . . . . . . . . . 14.

15. Total income (Add lines 1 through 14.). . . . . . . . . . . . . . 15.

16.Total adjustments to income from federal return

(IRA, alimony, etc.) . . . . . . . . . . . . . . . . . . . . . . . . . . . 16.

17.Adjusted gross income (Subtract line 16 from 15.)

(Enter on page 2, in each appropriate column of line 1.) . 17.

A. As originally reported or |

B. Net increase or |

C. Corrected amount. |

|||

as previously adjusted |

(decrease). |

|

|

||

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

.00 |

.00 |

.00 |

|||

|

|

|

|

|

|

COM/RAD 019

|

|

MARYLAND |

AMENDED TAX RETURN |

2022 |

||

|

|

FORM |

||||

|

|

|

|

|

Page 4 |

|

|

|

502X |

|

|

|

|

|

|

|

|

|

|

|

LAST NAME |

|

|

SSN |

|

||

|

|

|

|

|

|

|

II.ITEMIZED DEDUCTIONS: If you itemized deductions on your Maryland return, you must complete the following. If there are no changes to the amounts claimed on your original Maryland return, check here

and complete Column A and line 11 of Column C.

and complete Column A and line 11 of Column C.

A. As originally reported or |

B. Net increase or |

C. Corrected amount. |

as previously adjusted |

(decrease). |

|

1. Medical and dental expenses . . . . . . . . . . . . . . . . . . . . . .1.

2. Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2.

3. Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3.

4. Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4.

5. Casualty or theft losses. . . . . . . . . . . . . . . . . . . . . . . . . .5.

6. Miscellaneous . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6.

7. Enter total itemized deductions from federal Schedule A . .7.

8.Enter state and local income taxes included on line 2

or from worksheet (See Instruction 4.). . . . . . . . . . . . . . .8.

9. Net deductions (Subtract line 8 from line 7.). . . . . . . . . . .9.

10.Less deductions during period of nonresident status

(See Instructions 13 & 14.) . . . . . . . . . . . . . . . . . . . . . . 10.

11.Total Maryland deductions (Subtract line 10 from line 9.) (Enter on page 2, in each appropriate column of line 6.) . 11.

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

.00 |

.00 |

.00 |

||

|

|

|

|

|

III.EXPLANATION OF CHANGES TO INCOME, DEDUCTIONS AND CREDITS: Enter the line number from page 2 for each item you are changing and give the reason for each change. Attach any required supporting forms and schedules for items changed.

Check here

if you authorize your preparer to discuss this return with us.

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief it is true, correct and complete. If prepared by a person other than taxpayer, the declaration is based on all information of which the preparer has any knowledge.

Your signature |

|

Date |

|

|

|

Spouse’s signature |

|

Date |

To make an online payment, scan the QR code below and follow instructions.

Signature of preparer other than taxpayer (Required by Law)

Printed name of the Preparer/Firm's name

Street address of Preparer/Firm

City, State, ZIP + 4 |

|

Telephone number of preparer |

Preparer’s PTIN (Required by Law) |

Write your Social Security number on your check in blue or black ink. Make checks payable and mail to:

|

Comptroller of Maryland |

|

Revenue Administration Division |

|

110 Carroll Street |

COM/RAD 019 |

Annapolis, Maryland |

MARYLAND |

AMENDED INCOME TAX RETURN |

FORM |

INSTRUCTIONS |

502X |

IMPORTANT NOTES

You must file your Maryland Amended Form 502X electronically to claim, or change information related to, business income tax credits from Form 500CR.

Changes made as part of an amended return are subject to audit for up to three years from the date that the amended return is filed.

WHEN AND WHERE TO FILE

Generally, Form 502X must be filed within three years from the date the original return was due (including extensions) or filed. The following exceptions apply:

•A claim filed after three years, but within two years from the time the tax was paid is limited to the amount paid within the two years immediately before filing the claim.

•A claim for refund based on a federal net operating loss carryback must be filed within 3 years after the due date (including extensions) of the return for the tax year of the net operating loss.

•A claim for refund resulting from a credit for taxes paid to another state must be filed within one year of the date of the final notification by the other state that income tax is due.

•If the claim for refund or credit for overpayment resulted from a final determination made by an administrative board or an appeal of a decision of an administrative board, that is more than three years from the date of filing the return or more than two years from the time the tax was paid, the claim for refund must be filed within one year of the date of the final decision of the administrative board or final decision of the highest court to which an appeal of the administrative board is taken.

•If the United States Internal Revenue Service (IRS) issues a final determination of adjustments that would result in a decrease to Maryland taxable income, file Form 502X within one year after the final adjustment report or the final court decision if appealed.

•If the IRS issued a final determination of adjustments that would result in an increase to Maryland taxable income, file Form 502X within 90 days after the final determination.

Do not file an amended return until sufficient time has passed to allow the original return to be processed. For current year returns, allow at least six weeks. Note that no refund for less than $1.00 will be issued.

The amended return must be filed electronically or with the

Comptroller of Maryland, Revenue Administration Division, 110 Carroll Street, Annapolis, Maryland 21411- 0001.

For more information regarding refund limitations, see Administrative Release 20.

PROTECTIVE CLAIMS

A protective claim is a claim for a specific amount of refund filed on an amended return with a request that the Comptroller delay acting on the refund request. The claim for refund may not be based on a federal audit. The delay requested must be due to a pending decision by a state or federal court which will affect the outcome of the refund, or for reasonable cause. The protective claim must be filed in accordance with the limitations outlined in the section WHEN AND WHERE TO FILE.

The Comptroller may accept or reject a protective claim. If rejected, the taxpayer will be informed of a right to a hearing. We cannot accept a protective claim unless an original return has been filed.

2022

Page 1

PENALTIES

There are severe penalties for failing to file a tax return, failing to pay any tax when due, filing false or fraudulent returns or making a false certification. The penalties include criminal fines, imprisonment and a penalty on your taxes. In addition, interest is charged on amounts not paid when due.

To collect unpaid taxes, the Comptroller is directed to enter liens against the salary, wages or property of delinquent taxpayers.

PRIVACY ACT INFORMATION

The Revenue Administration Division requests information on tax returns to administer the income tax laws of Maryland, including determination and collection of correct taxes. If you fail to provide all or part of the requested information, the exemptions, exclusions, credits, deductions or adjustments may be disallowed and you may owe more tax. In addition, the law provides penalties for failing to supply information required by law or regulations.

You may look at any records held by the Revenue Administration Division which contain personal information about you. You may inspect such records, and you have certain rights to amend or correct them.

As authorized by law, information furnished to the Revenue Administration Division may be given to the IRS, a proper official of any state that exchanges tax information with Maryland and to an officer of this state having a right to the information in that officer’s official capacity. The information also may be obtained with a proper legislative or judicial order.

USE OF FEDERAL RETURN

Most changes to your federal return will result in changes on your Maryland return and you will need the information from your federal amendment to complete your Maryland amended return. Therefore, complete your federal return first. Maryland law requires that your income and deductions be entered on your Maryland return exactly as they were reported on your federal return. However, all items reported on your Maryland return are subject to verification, audit and revision by the Maryland Comptroller’s Office.

If you are amending your federal return, attach a photocopy of the federal Form 1040X and any revised schedules to your Maryland Form 502X. If your tax has been increased by the IRS, you must report this increase to the Maryland Revenue Administration Division within 90 days from the final IRS determination.

MARYLAND |

AMENDED INCOME TAX RETURN |

FORM |

INSTRUCTIONS |

502X |

SPECIFIC INSTRUCTIONS

1NAME, ADDRESS AND YEAR INFORMATION.

Enter the year, Social Security number, correct name and current address on the lines on page 1. Be sure to check the appropriate box if you or your spouse are 65 or over or blind on the last day of the tax year. Also enter the correct county, city or taxing area for the last day of the tax year being amended. If your address is different from the address on your original return, be sure to answer “Yes” to the first question.

If using a foreign address, complete the lines indicated for Country Name, Province/State/County, and Postal Code.

2QUESTIONS.

Answer all of the questions and attach copies of any federal notices, amended forms and schedules. If filing your amended return for a Net Operating Loss Carryback or Carryforward, check the appropriate box. If you have checked

3FILING STATUS.

Enter the filing status you used on your original return and show any change of filing status. Your filing status should correspond to the filing status used on your federal return.

Generally, you may not change from married filing joint to married filing separately after the original due date of the return. Any change in filing status to or from married filing joint requires the signature of both spouses. Enter a complete explanation in Part III on page 4 of Form 502X.

4COMPLETE PAGE 3 AND 4 OF FORM 502X.

PART I

Enter your original or previously adjusted amounts of income in Column A. Enter any increase (or decrease) in Column B and enter the corrected amounts in Column C. If you are not making any changes to your income as previously reported, complete Column A only and enter the total on line 17 of Column C.

2022

Page 2

PART II

If you itemized deductions, enter your original or previously adjusted amounts in Column A. Enter any increase (or decrease) in Column B and enter the corrected amounts in Column C. If you are not making any changes to your deductions as previously reported, complete Column A only and enter the total on line 11 of Column C.

NOTE: Any amount deducted as contributions of Preservation and Conservation Easements for which a credit is claimed must be included on line 8 of Part II of Form 502X.

PART III

Use this section to provide a detailed explanation of the changes being made on the amended return. A filing status change must be fully explained here. If this is a

Enter the line number from page 2 for each item you are changing and state the reason for the change. Be sure to attach any required schedules or forms.

NOW COMPLETE PAGE 2 AND 3 OF FORM 502X.

COLUMNS

In Column A, enter the amounts from your return as originally filed or as previously adjusted or amended.

In Column B, enter the net increase or net decrease for each line you are changing. Show all decreases in parentheses. Explain each change in Part III of Form 502X and attach any related schedule or form. If you need more space, show the required information on an attached statement.

For Column C, add the increase in Column B to the amount in Column A, or subtract the Column B decrease from Column A. For any item you do not change, enter the amount from Column A in Column C.

5FIGURE YOUR MARYLAND TAX.

LINE 1 – Income and adjustments from federal return.

Copy the amounts from your federal amended return or as corrected by the IRS and enter a complete explanation of the changes in Part III.

LINE 1a. – Earned income. Enter the amount from line 1b of form 502 used to calculate your federal earned income credit (EIC), Maryland Earned Income Credit, or poverty level credit (PLC). Earned income includes wages, salaries, tips, professional fees and other compensation received for personal services you performed. It also includes any amount received as a scholarship that you included in your federal AGI.

2022 Tax Rate Schedules

Tax Rate Schedule I

For taxpayers filing as Single, Married Filing Separately, or as Dependent Taxpayers. This rate is also used for taxpayers filing as

Fiduciaries.

If taxable net income is: |

Maryland Tax is: |

|||

At least: |

but not over: |

|

|

|

$0 |

$1,000 |

|

2.00% |

of taxable net income |

$1,000 |

$2,000 |

$20.00 |

plus 3.00% |

of excess over $1,000 |

$2,000 |

$3,000 |

$50.00 |

plus 4.00% |

of excess over $2,000 |

$3,000 |

$100,000 |

$90.00 |

plus 4.75% |

of excess over $3,000 |

$100,000 |

$125,000 |

$4,697.50 |

plus 5.00% |

of excess over $100,000 |

$125,000 |

$150,000 |

$5,947.50 |

plus 5.25% |

of excess over $125,000 |

$150,000 |

$250,000 |

$7,260.00 |

plus 5.50% |

of excess over $150,000 |

$250,000 |

$12,760.00 |

plus 5.75% |

of excess over $250,000 |

|

Tax Rate Schedule II

For taxpayers filing Joint, Head of Household, or for Qualifying Widows/ Widowers.

If taxable net income is: |

Maryland Tax is: |

|||

At least: |

but not over: |

|

|

|

$0 |

$1,000 |

|

2.00% |

of taxable net income |

$1,000 |

$2,000 |

$20.00 |

plus 3.00% |

of excess over $1,000 |

$2,000 |

$3,000 |

$50.00 |

plus 4.00% |

of excess over $2,000 |

$3,000 |

$150,000 |

$90.00 |

plus 4.75% |

of excess over $3,000 |

$150,000 |

$175,000 |

$7,072.50 |

plus 5.00% |

of excess over $150,000 |

$175,000 |

$225,000 |

$8,322.50 |

plus 5.25% |

of excess over $175,000 |

$225,000 |

$300,000 |

$10,947.50 |

plus 5.50% |

of excess over $225,000 |

$300,000 |

$15,072.50 |

plus 5.75% |

of excess over $300,000 |

|

MARYLAND AMENDED INCOME TAX RETURN |

2022 |

FORM |

|

502X |

INSTRUCTIONS |

Page 3 |

|

||

|

|

LINE 2 – Additions to income. For decoupling and tax preference items and amounts to be added when credits are claimed, include corrected Form(s) 500DM, 502TP, 502CR or 500CR. In addition, enter the amount equal to a tax credit claimed for tax paid on distributive or

LINE 4 – Subtractions from income. Enter items such as child care expenses, pension exclusion and other subtractions (shown in the instructions for your original return). Attach revised Form 502SU if there were any changes to that form. Enter an explanation of the changes in Part III and attach any corrected forms.

LINE 6 – Method of computation.

Standard deduction method. The standard deduction is 15% of the Maryland adjusted gross income with the following minimums and maximums.

Filing Status |

|

Single |

Minimum of $1,600 and maximum |

Married filing separately |

of $2,400 |

Dependent taxpayer |

|

or |

|

Filing Status |

|

Married filing joint or |

Minimum of $3,200 and maximum |

spouse had no income |

of $4,850 |

Head of household |

|

Qualifying widow(er) |

|

with dependent child |

|

Itemized deduction method. Check the box and enter your total Maryland itemized deductions.

LINE 8 – Exemptions. Multiply exemptions for taxpayers 65 or over or blind by $1,000, the personal exemption is $3,200.

This exemption is reduced once the taxpayer’s federal adjusted gross income exceeds $100,000 ($150,000 if filing Joint, Head

of Household, or Qualifying Widow(er) with Dependent Child). If you are subject to this reduction, see the exemption chart, Instruction 10 of the Resident Instructions. Attach amended Form 502B if you are changing dependent information.

LINE 10 – Computing the tax. Line 9 will be your Maryland taxable income. Use the rate schedule.

6EARNED INCOME CREDIT, POVERTY LEVEL CREDIT, CREDITS FOR INDIVIDUALS AND BUSINESS TAX CREDITS.

Enter each credit being claimed on the appropriate field on line 10a. You may claim your earned income credit on line 10a. Refer to the Resident Instructions and worksheet to compute the allowable credit. If you were a

You may also claim a credit on line 10a equal to 5% of your earned income if your income is less than the poverty level guidelines. Refer to the Resident Instructions and worksheet to compute the allowable credit. If you were a

Personal income tax credits from Form 502CR should be entered on the appropriate field on line 10a. A credit for a portion of the local income tax may also be available. See instructions to Form 502CR, Part A and the instructions in Part

7 below. If this amount is different from the original return, be sure to attach completed Form 502CR with appropriate documentation or certification.

You must file your amended return electronically to claim or modify a business tax credit from Form 500CR.

The amount of the nonrefundable portion of the business tax credit Form 500CR should be entered on line 10a of the electronic version of 502X. If this amount is different from the original return, be sure to include the appropriate documentation or certification with the electronic version.

If the total credits on line 10a are greater than the tax on line 10, enter zero on line 10b. The credits entered on line 10a are nonrefundable. For information concerning refundable credits, see Instruction 9.

7LOCAL INCOME TAX AND LOCAL CREDITS.

Complete lines 11, 11a and 11b.

The local income tax is calculated by multiplying the taxable net income from line 9 by the local tax rate shown on the following Local Tax Rate Chart. Use the local tax rate for the county (or Baltimore City) in which you resided on the last day of the tax year. Enter the result on line 11.

A separate calculation of the earned income credit is required when computing the local income tax. Use the worksheets in the appropriate instructions to compute the local credits and enter the result on line 11a. If you were a

Enter the amount of the credit calculated in the local summary of Form 502CR, Part L on the Personal Credit field on line 11a.

2022 Local Tax Rate |

|

Subdivision |

Rate |

Baltimore City |

.0320 |

Allegany County |

.0305 |

Anne Arundel County |

.0281 |

Baltimore County |

.0320 |

Calvert County |

.0300 |

Caroline County |

.0320 |

Carroll County |

.0303 |

Cecil County |

.0300 |

Charles County |

.0303 |

Dorchester County |

.0320 |

Frederick County |

.0296 |

Garrett County |

.0265 |

Harford County |

.0306 |

Howard County |

.0320 |

Kent County |

.0320 |

Montgomery County |

.0320 |

Prince George’s County |

.0320 |

Queen Anne’s County |

.0320 |

St. Mary’s County |

.0310 |

Somerset County |

.0320 |

Talbot County |

.0240 |

Washington County |

.0300 |

Wicomico County |

.0320 |

Worcester County |

.0225 |

8CONTRIBUTIONS TO THE CHESAPEAKE BAY AND ENDANGERED SPECIES FUND, DEVELOPMENTAL DISABILITIES SERVICES AND SUPPORT FUND, MARYLAND CANCER FUND AND FAIR CAMPAIGN FINANCING FUND.

Enter the amounts of your contribution in 13A for the

MARYLAND AMENDED INCOME TAX RETURN |

2022 |

|

FORM |

INSTRUCTIONS |

|

502X |

Page 4 |

|

Chesapeake Bay and Endangered Species Fund, 13B for the Developmental Disabilities Services and Support Fund, 13C for the Maryland Cancer Fund, 13D for the Fair Campaign Financing Fund. Any contribution will increase your balance due or reduce your refund. Enter the total of your contributions in the appropriate columns. Additional information concerning the funds is contained in the instructions for the tax year of the amended return.

9TAXES PAID AND CREDITS.

Write your taxes paid and credits on lines

Enter the correct amounts on lines 15 through 19 and attach any additional or corrected

Refundable Earned Income Credit. You may be eligible for

arefundable earned income credit if

Refundable Income Tax Credits. Enter the total of your refundable income tax credits on line 19. You must attach Form 502CR.

1.STUDENT LOAN DEBT RELIEF TAX CREDIT. See Form 502CR Instructions.

2.HERITAGE STRUCTURE REHABILITATION TAX CREDIT. See Form 502S Instructions.

3.REFUNDABLE BUSINESS INCOME TAX CREDIT. See Form 500CR Instructions for qualifications. You must amend your return electronically to claim a business tax credit from Form 500CR.

4.IRC SECTION 1341 REPAYMENT CREDIT. If you repaid an amount this year reported as income on a prior year federal tax return that was greater than $3,000, you may be eligible for an IRC Section 1341 repayment credit. See Administrative Release 40.

5.CATALYTIC REVITALIZATION PROJECTS AND HISTORIC REVITALIZATION TAX CREDIT. If you are an individual, business entity or nonprofit organization, you may claim a tax credit in an amount equal to 20% of the amount stated in the final tax credit certificate issued by the Secretary of this subtitle for 5 consecutive taxable years beginning with the taxable years in which the Catalytic Revitalization Projects is completed. See Form 502CR Instructions.

6.

7.CREDIT FOR CHILD AND DEPENDENT CARE EXPENSES. If your Maryland credit for child and dependent care expenses exceeds your Maryland Tax, you may qualify for this credit. See Form 502CR Instructions.

8.MARYLAND CHILD TAX CREDIT. If you have any dependent(s) under the age of 17 on the last day of the tax year who has (have) a disability, you may be eligible for this credit. See Form 502CR Instructions.

9.PTE TAX PAID ON MEMBERS’ DISTRIBUTIVE OR PRO RATA SHARES OF INCOME. If you are the beneficiary of a trust or a Qualified Subchapter S Trust which elected to pay the tax imposed with respect to members’ distributive or

pro rata shares, you may be entitled to a credit for your share of that tax. Enter the amount on this line and attach the Maryland Schedule

If you are a member of a PTE

10 BALANCE DUE OR OVERPAYMENT.

Calculate the balance due or overpayment by subtracting the total on line 20 from the amount on line 14 and enter the result on either line 21 or line 22.

Enter the tax paid with the original return plus any additional tax paid after filing on line 23 (do not enter interest or penalty paid), OR enter the overpayment from your original return plus any additional overpayments from prior amendments or adjust- ments on line 24.

If there is an amount on line 21:

•and line 21 is more than line 23, you owe additional tax. Enter the difference on line 26 and compute the interest due using the interest rates in Instruction 11.

•and there is also an amount on line 24, you owe additional tax. Add the two together and enter the total on line 26. Compute the interest due. See Instruction 11.

•and line 21 is less than line 23, you are due a refund. Enter the difference on line 25.

If there is an amount on line 22:

•and line 22 is more than line 24, you are due an additional refund. Enter the difference on line 25.

•and there is also an amount on line 23, you are due an additional refund. Add the two together and enter on line 25.

•and line 22 is less than line 24, you owe additional tax. Enter the difference on line 26 and compute the interest due using the interest rates in Instruction 11.

Previous interest and penalty

Interest and/or penalty charges for the year you are amending, whether previously paid or still outstanding, may be adjusted as a result of your amendment. Any payments made on the account have been applied first to penalty, then to interest and lastly to tax due. These payments may require reallocation depending on the result of the amendment. We will notify you of the net balance due or refund when we have completed pro- cessing your Form 502X.

NOTE: If all or part of the overpayment on your original return was credited to an estimated tax account for next year, we cannot reduce or remove this credit without specific authoriza- tion from you. If you have a balance due, and wish to apply monies credited to a 2022 estimated tax account, attach writ- ten authorization for the amount to be removed. Interest charges are assessed even if the balance due is paid from the 2022 account.

11 |

INTEREST ON TAX DUE AND INTEREST FOR |

UNDERPAYMENT OF ESTIMATED TAX. |

Interest must be computed and paid on any balance of tax due. Interest is due from the date the return was originally due to be filed until the date the tax is paid. Interest is due at the rate of 9.0% annually or 0.7500%

MARYLAND |

AMENDED INCOME TAX RETURN |

FORM |

INSTRUCTIONS |

502X |

per month for any month or part of a month that a tax is paid after the original due date of the 2022 return but before January 1, 2024. For assistance in calculating interest for tax paid on or after January 1, 2024, visit www.marylandtaxes.gov.

UNDERPAYMENT OF ESTIMATED TAX

If you do not meet the requirement for avoidance of interest for underpayment of estimated tax, obtain Form 502UP online at www.marylandtaxes.gov or from any office of the Revenue Administration Division. Complete and attach it to your amended return. Enter any interest due on line 27 of Form 502X.

If you calculated and paid interest on underpayment of estimated tax with your original return, recalculate the interest based on your amended tax return, and attach a copy of a revised Form 502UP showing your recalculation.

12 |

SIGNATURE, ATTACHMENTS AND PAYMENT |

INSTRUCTIONS. |

Sign and date your return on page 4 and attach all required forms, schedules and statements.

SIGNATURES

You must sign your return. Both spouses must sign a joint return. Your signature(s) signify that your return, including all attachments, is, to the best of your knowledge and belief, true, correct and complete, under penalties of perjury.

TAX PREPARERS

If another person prepared your return, that person also must sign the return and enter their Preparer’s Tax Identification Number (PTIN). The preparer declares that the return is based on all information required to be reported of which the preparer has knowledge, under penalties of perjury. Penalties may be imposed for tax preparers who fail to sign the tax return and provide their tax identification number.

ATTACHMENTS

Be sure to attach wage and tax statements (Forms

MAILING INSTRUCTIONS

Mail your return to:

Comptroller of Maryland

Revenue Administration Division

Amended Return Unit

110 Carroll Street

Annapolis, MD

PAYMENT INSTRUCTIONS

Make your check or money order payable to “Comptroller of Maryland.” Write the type of tax and year of tax being paid on your check. It is recommended that you include your Social Security number on check using blue or black ink.

DO NOT SEND CASH.

13 CHANGE OF RESIDENT STATUS.

Be sure to enter a full explanation of the change of resident status in Part III on page 4 of the amended form.

If you are changing your resident status from a resident to a

2022

Page 5

nonresident, see Instruction 14. Complete Part III with a full explanation of your reasons for the change. A nonresident of Maryland is subject to tax on income from Maryland sources; that is, wages and salaries from services performed in Maryland, income from business carried on in Maryland, gambling winnings from Maryland sources, income from

If you are amending to show

IIIand attach a photocopy of the income tax return filed with the other state or states of residence. If you are changing your status from a nonresident to a resident, you must use Form 502X and follow the instructions as written.

Maryland Income Factor

You must adjust your standard or itemized deductions and exemptions based on the percentage of your income subject to Maryland tax. Divide your Maryland adjusted gross income (line 5) by your federal adjusted gross income (line 1) to figure the percentage of Maryland income to total income. Use amended amounts if either of these lines were changed. The factor cannot exceed 1 (100%) and cannot be less than zero (0%). If line 5 is 0 or less, the factor is 0. If line 5 is greater than 0 and line 1 is 0 or less, the factor is 1. Another method of allocating itemized deductions may be allowed if you receive written approval prior to the filing of your return.

14 NONRESIDENTS.

Generally, nonresident taxpayers will use Form 505X and Form 505NR to amend their return; however, nonresidents who wish to amend Form 515, must use Form 502X and a revised Form 505NR.

In addition, if you are changing from nonresident to resident status, you must use Form 502X and see Instruction 13.

15 NET OPERATING LOSS (NOL).

To claim a deduction for a federal NOL on the Maryland return, you must first calculate the NOL for federal purposes. A deduction will be allowed on the Maryland return for the amount of the loss actually used on the federal return. The amount of loss used for federal purposes is generally equal to the federal taxable income (before loss is used) or the federal modified taxable income as calculated for the year of carryback or carryforward.

An addition or subtraction modification may be required in a carryback or carryforward year when the federal NOL, or the year to which the NOL is carried, includes certain items included in certain provisions of the Internal Revenue Code from which the State of Maryland has decoupled, including items included in certain special depreciation allowances and

An NOL generated when an individual or a business entity is

MARYLAND |

AMENDED INCOME TAX RETURN |

FORM |

INSTRUCTIONS |

502X |

not subject to Maryland income tax law, in a tax year beginning on or after October 22, 2007, cannot be used as a deduction to offset Maryland income. For acquisitions or liquidations occurring on or after October 22, 2007, the acquiring business entity which is subject to Maryland income tax law cannot use the acquired or liquidated business entity’s NOL as a deduction to offset Maryland income, if the acquired or liquidated business entity was not subject to Maryland income tax law when its NOL was generated. An NOL being carried forward from tax years beginning before October 22, 2007 can be used until exhausted.

An addition to income may be required in a carryback or carryforward year if the total Maryland additions to income exceeds the total Maryland subtractions from income in the loss year. The required addition to income represents a recapture of the excess additions over subtractions. The addition to income required is generally equal to the lesser of the NOL deduction in the carryback year or the net addition modification (NAM) in the loss year unless the loss year includes a decoupling modification. For more information regarding NAM, refer to Administrative Release 18.

If you elect to forego a carryback for the loss year, a copy of the federal election for the loss year must be attached with the Maryland amended return.

You must attach copies of amended federal Form 1045 or 1040X, whichever was used for federal purposes, and a copy of the federal income tax return for the year of the loss. Also include Schedules A and B of Form 1045 or the equivalent worksheets used to develop the federal NOL and show the amounts used on the federal return in the carryback or carryforward years. Check the appropriate CARRY BACK or CARRY FORWARD box on page 1 of Form 502X.

16 INCOME TAX ASSISTANCE.

If you need more information, visit www.marylandtaxes. gov. You may also call

2022

Page 6

File Breakdown

| Fact Name | Description |

| Form Title | Maryland Amended Tax Return 2020, Form 502X |

| Use | To amend a previously filed Maryland state tax return |

| Ink Requirement | Must be completed in blue or black ink |

| Electronic Filing Requirement | Form 502X must be filed electronically for amendments related to business income tax credits from Form 500CR |

| Time Limit for Filing | Generally, within three years from the date the original return was due or filed |

| Exceptions for Time Limit | Various exceptions apply, including specific timelines for claims based on federal net operating loss carrybacks and credits for taxes paid to another state |

| Audit Possibility | Amended returns are subject to audit up to three years after the amended return is filed |

| Minimum Refund Issue | No refund will be issued for amounts less than $1.00 |

| Address for Mailing | Comptroller of Maryland, Revenue Administration Division, 110 Carroll Street, Annapolis, Maryland 21411-0001 |

| Requirements if Federal Return is Amended | If an amended federal return is filed, a photocopy of Form 1040X and any revised schedules must be attached to the Maryland Form 502X |

| Protective Claims | Allows a taxpayer to file a claim for a specific refund amount pending a decision by a court which will affect the outcome, under certain conditions |

| Governing Law | Maryland income tax laws and regulations |

Steps to Filling Out Maryland 502X

Filing an amended tax return can often seem like a daunting task, but it's necessary when you need to correct any information on your original tax return or report additional income or deductions. In Maryland, the form used for this purpose is Form 502X for the year 2020. The process involves providing updated income and deduction information, and potentially adjusting your tax liability or refund. Given the need to ensure accuracy in these adjustments, it's crucial to follow the steps carefully to avoid potential issues with the state tax authority.

- Begin by obtaining the correct form, Maryland Form 502X, for the specific tax year you are amending.

- Use blue or black ink to fill out the form, ensuring legibility and preventing issues with processing.

- Enter your personal information, including your Social Security Number, name, and if filing jointly, your spouse's name and Social Security Number.

- Verify that your name matches the name on your Social Security card. If not, contact the Social Security Administration for guidance.

- Provide your current mailing address, including any apartment or suite number, city, town, or taxing area, and Maryland County if applicable.

- Indicate if there are any changes in your residency status and provide the relevant dates if you were a part-year resident or nonresident.

- If your original return's filing status has changed, mark the amended status on the form.

- On Page 2, under "Income and Adjustments to Income," report your federal adjusted gross income and any changes that have occurred. Here, you'll adjust your income with the corrected amounts or note any increases or decreases.

- Proceed to calculate your Maryland adjusted gross income, exemptions, and deductions, following instructions carefully to ensure changes are correctly noted and accurately recalculated.

- Fill out the Tax Computation section to reflect any changes in your Maryland state tax, taking into account any additional credits or taxes paid.

- If you have adjustments to itemized deductions, complete Section II as required, specifying the net change.

- In Part III, provide a detailed explanation for each change you're reporting on this amended return, including specific line numbers and reasons for adjustments. Attach any necessary documentation or revised schedules to support these changes.

- Sign and date the amended return. If filing jointly, your spouse must also sign.

- Make a copy of the entire package for your records.

- Mail the completed form, along with any payment due or as directed for a refund, to the Comptroller of Maryland, Revenue Administration Division, at the specified address.

- If you are attaching a payment, write your Social Security number on your check and use blue or black ink.

- After submitting, monitor your status through the state's tax department to ensure processing and to address any follow-up questions.

Once your amended return is filed, the state tax authority may take several weeks to process the adjustments. It's important to stay informed on the status and be prepared to provide additional information if contacted. Filing an amended return correctly is crucial for ensuring your tax obligations are accurate, avoiding potential penalties for underreported income or incorrect deductions.

More About Maryland 502X

What is a Maryland Form 502X and who needs to file it?

Maryland Form 502X is an Amended Tax Return form designed for taxpayers who need to correct or update their previously filed Maryland state income tax returns. This could involve changes to income, deductions, credits, or filing status. If you've noticed errors or if your federal return has been amended and it affects your Maryland return, then you would need to file Form 502X to make the necessary corrections.

How do I file a Maryland Form 502X?

To file a Maryland Form 502X, you will need to:

- Complete the form using blue or black ink if filing by paper, or electronically through a system approved by the Maryland Comptroller's Office for those eligible for electronic filing.

- Include any required supporting documents. For example, if your federal return was amended, attach a copy of the federal Form 1040X along with any revised schedules.

- Explain the reasons for the changes in Part III on page 4 of the form.

- File within the specific timeframe as detailed in the WHEN AND WHERE TO FILE section to avoid penalties and ensure your return is accepted.

When is the deadline to file Form 502X?

The general deadline for filing Form 502X is within three years from the date the original tax return was due or filed, whichever is later. There are exceptions and specific circumstances that may alter this deadline, such as filing a claim based on a federal net operating loss carryback, or following a final determination made by the IRS that affects your Maryland taxable income. It's critical to file within these timeframes to ensure your amendment is considered valid.

Can I file Maryland Form 502X electronically?

Yes, Maryland encourages taxpayers to file their amended returns electronically for faster processing and convenience. Form 502X is eligible for electronic filing if amending for certain reasons, such as claiming business income tax credits from Form 500CR. However, if your amendment is not related to these specific credits, you may need to file a paper return. Check the Maryland Comptroller's Office website or contact them directly for the most current information on electronic filing eligibility and processes.

What should I do if my address has changed since filing my original return?

If your address has changed since you filed your original tax return, ensure you update this information on Form 502X. Check the box indicating a change of address and provide your new mailing address. This is crucial for receiving any correspondence or refunds from the Comptroller of Maryland. Additionally, consider updating your address directly with the Comptroller to ensure all future communications are sent to the right place.

Common mistakes

When people fill out the Maryland 502X form to amend their taxes, several common mistakes can complicate the process or delay refunds. Identifying these pitfalls can ensure a smoother amendment process. Here’s a look at eight typical errors:

- Not using blue or black ink for manual submissions can cause readability issues.

- Forgetting to check the box indicating whether an address has changed from the original return leads to confusion and potential miscommunication.

- Selecting the incorrect filing status when it differs from the original submission or failing to update it accordingly complicates processing.

- Entering incorrect Social Security numbers or not matching them with the Social Security Administration's records results in processing delays.

- Omitting attachments such as copies of the federal return, schedules, or IRS notices when there are adjustments reported by the IRS or an amended federal return was filed.

- Miscalculating the Maryland adjusted gross income by either not correctly transferring the federal adjusted gross income or making errors in additions or subtractions.

- Selecting the wrong deduction method or inaccurately computing either the standard or itemized deductions.

- Failure to provide a detailed explanation in Part III for changes made to income, deductions, and credits, along with not attaching any required supporting forms and schedules.

By avoiding these common errors and double-checking all entries, filers can help ensure that their amended Maryland tax return process is as efficient and mistake-free as possible.

Documents used along the form

When completing the Maryland 502X form, various documents and forms often accompany the submission to ensure thorough processing and compliance with state tax regulations. These documents support claims, offer supplemental information, or correct previously submitted data. Understanding each is pivotal for a smooth amendment process.

- Form W-2: This form reports an individual's annual wages and the amount of taxes withheld from their paycheck. It’s crucial for verifying income and tax withholding on the amended return.

- Form 1099: Various 1099 forms report income from sources other than wages, such as independent contractor income (1099-NEC), interest income (1099-INT), and dividend income (1099-DIV). These forms support adjustments in income not initially reported or corrected.

- Schedule A (Itemized Deductions): If the taxpayer itemized deductions on their original return and is making adjustments to those deductions, a revised Schedule A may need to be included with Form 502X to detail the changes.

- Form 1040X: The Amended U.S. Individual Income Tax Return is often required if adjustments made on the state level are because of changes to the federal return. A copy of the amended federal return substantiates the amendments made on the state return.

- Form MW506NRS: This is the Nonresident Sale of Real Property form. If the amendment relates to income or withholding from the sale of Maryland real property by a nonresident, this form supports adjustments in reported income or taxes withheld.

Each of these documents plays a definitive role in ensuring that the Maryland 502X form is accurately processed. They provide a narrative and numerical substantiation of the adjustments being reported, hence enabling the Maryland Revenue Administration Division to understand and verify the changes. It is the responsibility of the taxpayer to provide comprehensive and accurate documentation to avoid discrepancies or potential audits. Preparing and submitting these documents thoughtfully can lead to a more favorable and expeditious amendment process.

Similar forms

The Maryland 502X form is similar to the IRS Form 1040X. Both are used to amend previously filed income tax returns. When taxpayers discover errors or receive new information that changes their taxable income, tax credits, or deductions, these forms come into play. The main purpose of these forms is to correct errors and ensure the accurate calculation of tax liability. The Maryland 502X form requires information similar to that on the federal Form 1040X, such as original tax figures, changes being made, and the corrected amounts. Additionally, it prompts filers to explain the reason for each change, mirroring the federal form's requirement for an explanation of the amendments made.

Another document similar to the Maryland 502X form is the state amended tax return forms from other states, such as the California Form 540X. Like the Maryland 502X, these forms serve the same fundamental function: to amend a previously filed state income tax return. They typically require the taxpayer to provide the original figures, detail the changes, and submit the corrected figures. This process ensures that taxpayers can address any discrepancies or changes in their income, deductions, or credits that were not correctly reported on their original state tax returns. The primary differences among these forms are the specific line items and tax laws referenced, which vary by state.

Dos and Don'ts

Do use blue or black ink when filling out the Maryland 502X form to ensure legibility and compliance with the instructions.

Do not use different colored inks as they may not be accepted or could cause issues in processing your amended tax return.

Do double-check that your name matches the name on your social security card. If there are any discrepancies, promptly contact the Social Security Administration (SSA) at 1-800-772-1213 or visit www.ssa.gov.

Do not ignore discrepancies in your personal information. Any mismatches could result in processing delays or issues with your tax records.

Do ensure to check the correct status box that applies to you, such as full-year resident, part-year resident, or nonresident, based on your situation during the tax year.

Do not inaccurately report your residency status. Misreporting can lead to incorrect calculation of taxes or penalties.

Do attach copies of the federal loss year return and Form 1045, Schedules A and B, if you are filing to claim a net operating loss.

Do not file your 502X form without the required attachments if you're claiming adjustments related to a net operating loss or any changes that have been corrected by the Internal Revenue Service (IRS).

Do provide an explanation for any changes from the original filing in Part III on page 4 of the form. Attach any required supporting documents for the items you have changed.

Do not leave out explanations for the changes made to your income, deductions, and credits. Failing to explain the adjustments could raise questions or delay the processing of your amended return.

Do make sure that if there’s a change in your address, you check the appropriate box and update the information to ensure you receive all correspondence regarding your amended return.

Do not use the form without verifying whether an amended federal return is being filed or if your original federal return has been changed or corrected by the IRS. If yes, submit a copy of the notice or amended federal return.

Do sign and date your amended return. If you are filing jointly, ensure your spouse also signs the return.

Do not forget to write your Social Security number on your check in blue or black ink if you owe additional taxes and are making a payment with your return.

Misconceptions

Understanding the Maryland 502X form can sometimes be challenging, leading to misconceptions. Here are some common misunderstandings clarified to help ensure the process is smoother for those needing to amend their Maryland tax returns.

- Misconception 1: The Maryland 502X form does not require information from the federal tax return.

This is incorrect. The Maryland 502X form requires specifics from your federal income tax return. Changes made on your federal return can affect your Maryland amended return. Thus, completing the federal amendment first is advisable as it provides necessary details for the Maryland 502X.

- Misconception 2: Amended returns can be filed at any time.

There are specific time frames within which an amended return must be filed. Generally, Form 502X must be submitted within three years from the original return's due date, including extensions. There are exceptions for unique situations like claiming a refund based on a federal net operating loss carryback. Understanding these deadlines is crucial to ensure your amendment is considered timely.

- Misconception 3: Electronic filing is optional for the Maryland 502X form.

In fact, the Maryland 502X form must be filed electronically if it includes claims or changes to business income tax credits from Form 500CR. Electronic submission ensures faster processing and is a requirement in certain situations, illustrating the move towards more digital tax administration processes.

- Misconception 4: Any change on the Maryland 502X form results in an immediate refund.

Filing an amended return does not guarantee an immediate refund. The amended return is subject to review and verification by the Maryland Comptroller's office. The process involves checking for accuracy and completeness, which may lead to adjustments in tax liability. If a refund is due, it will be processed after these considerations, and remember, no refund will be issued for amounts less than $1.00.

Understanding these aspects of the Maryland 502X form can alleviate concerns and ensure the amended tax return process is completed accurately. For further clarifications, it's recommended to consult directly with Maryland's tax authorities or a tax professional.

Key takeaways

Filing the Maryland 502X form is necessary if you need to amend a previously filed state tax return. This could be due to changes in your income, deductions, or credits, or if you have made an error on your original submission.

When making amendments, it's essential to use blue or black ink and ensure all information is legible. This includes correctly filling out your social security number, name, and current mailing address, as these details are key to processing your amended return accurately.

The 502X form requires a detailed explanation for each change made from the original return. Part III of the form provides space to explain these adjustments, and attaching any required supporting documentation is critical for validating these changes.

If your amendment results from corrections made by the IRS to your federal return, you must also file an amended return in Maryland. Copies of the notice from the IRS, indicating the changes made, should accompany your 502X submission.

Finally, there are specific time frames within which an amended return must be filed to be considered valid. Typically, you have three years from the original due date of the return, including any extensions, to file a 502X form. However, there are exceptions based on particular circumstances, such as claims based on federal net operating loss carrybacks or adjustments following a federal audit.

Common PDF Templates

Maryland 2023 Tax Forms - Includes provision for calculating local tax rates specific to Maryland's jurisdictions.

Maryland Confidential Morbidity Report - Features detailed options for indicating specific laboratory tests related to viral hepatitis.