Maryland 504 PDF Template

The Maryland 504 Fiduciary Income Tax Return is a crucial document for fiduciaries managing estates or trusts within Maryland. This form, relevant for the fiscal year 2008, encompasses a range of details including the federal employer identification number, the name and address of the fiduciary, and specific data about the type of entity being reported such as decedent's estate, simple trust, complex trust, grantor type trust, bankruptcy estate, qualified funeral trust, among others. Key sections of the form involve reporting federal taxable income, exemptions claimed, and modifications specific to Maryland law. It also addresses the calculation of Maryland adjusted gross income, taxable net income, and applicable taxes or contributions toward state funds. An amended return option is available for corrections or updates to previously filed returns. Additionally, the form includes provisions for nonresident beneficiaries, highlighting the state's approach to income sourced from intangible personal property. Completion of the Maryland 504 is a vital step for fiduciaries to comply with state tax obligations, facilitate accurate tax reporting for estates or trusts, and ensure beneficiaries’ interests are properly managed and protected under Maryland law.

Maryland 504 Sample

|

|

MARYLAND |

FIDUCIARY INCOME |

|

|||||

|

|

|

|||||||

|

|

FORM |

TAX RETURN |

|

|||||

|

|

|

|||||||

|

504 |

|

|

|

|

|

|

|

|

|

|

OR FISCAL YEAR BEGINNING |

2022, ENDING |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

Federal Employer Identification Number (9 digits) |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

Name of Estate or Trust |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Black Ink Only |

Name and Title of Fiduciary |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Current Mailing Address of Fiduciary - Line 1 (Street No. and Street Name or PO Box) |

|

||||||||

Using Blue or |

|

|

|

|

|

||||

Current Mailing Address of Fiduciary - Line 2 (Apt No., Suite No., Floor No.) |

|

||||||||

|

|

|

|

|

|

|

|

|

|

2022

$

STAPLE CHECK HERE

|

City or Town |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

|

ZIP Code |

|

|

|

+4 |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Country Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign Province/State/County |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Foreign postal code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

TYPE OF ENTITY - Check the box(es) on the return corresponding to your federal return. |

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

|

|

1. |

|

Decedent's estate |

4. |

|

|

|

|

Grantor type trust |

7. |

|

|

|

Electing Small Business Trust |

|

|

|

||||||||||||||||||||||||

|

|

2. |

|

Simple trust |

5. |

|

|

|

|

Bankruptcy estate |

8. |

|

|

|

Other |

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

3. |

|

Complex trust |

6. |

|

|

|

|

Qualified funeral trust |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DECEDENT'S ESTATE INFORMATION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

If Decedent's estate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Date of death |

|

|

|

|

|

|

|

|

|

|

|

Decedent's Social Security Number |

|

|

|

|

|

|

|

||||||||||||||||||||||

|

Domicile of decedent |

|

|

|

|

|

|

|

|

|

|

|

|

|

Check here if final return. |

(do not enter / or |

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RESIDENT STATUS |

|

|

|

|

|

|

|

|

|

|

|

AMENDED RETURN |

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

Check box if resident and complete the following |

|

|

|

|

|

Check applicable box(es). |

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

Subdivision Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This is an amended return. (Attach documentation) |

|

|

|

||||||||||||||||||||||

|

County |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net operating loss is being carried back. |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

City, town or taxing area |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name or address has changed. |

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

Check box if nonresident. See Form 504NR |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

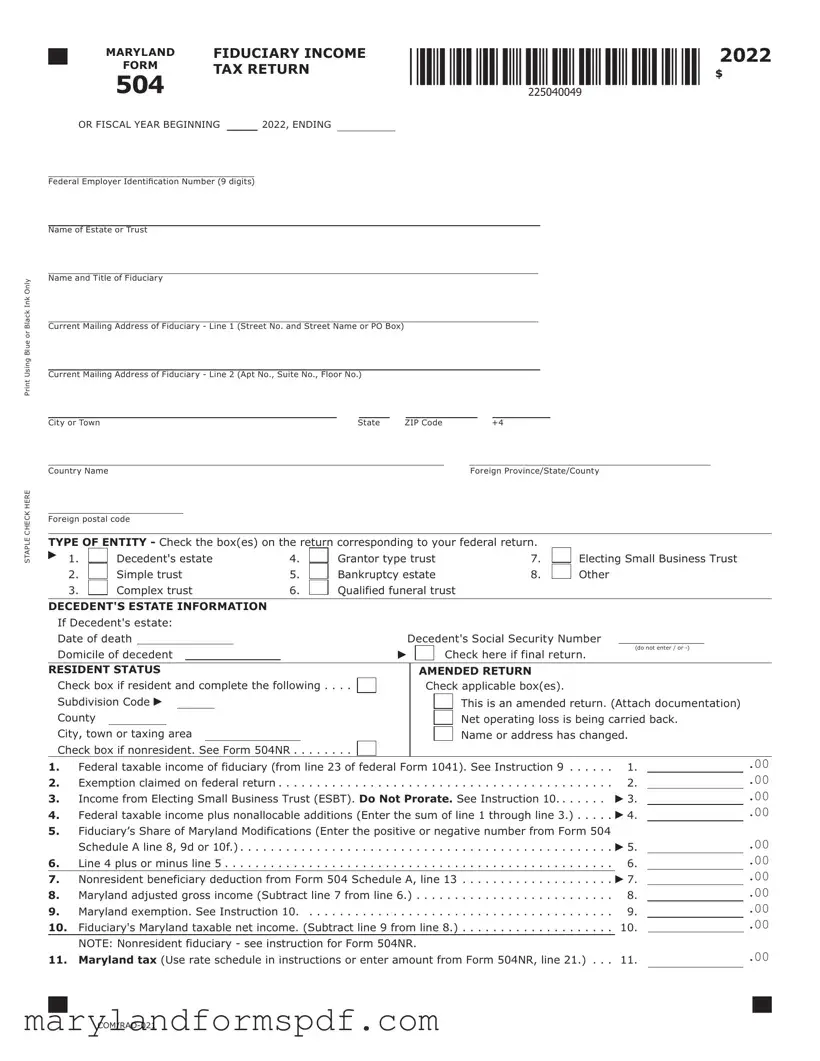

1. |

Federal taxable income of fiduciary (from line 23 of federal Form 1041). See Instruction 9 |

1. |

|

|

|

.00 |

|

|||||||||||||||||||||||||||||||||||

2. |

Exemption claimed on federal return |

2. |

|

|

|

.00 |

|

|||||||||||||||||||||||||||||||||||

3. |

.. .Income from Electing Small Business Trust (ESBT). Do Not Prorate. See Instruction 10 |

3. |

|

|

|

.00 |

|

|||||||||||||||||||||||||||||||||||

4. |

Federal taxable income plus nonallocable additions (Enter the sum of line 1 through line 3.) |

.. . . . . |

4. |

|

|

|

.00 |

|

||||||||||||||||||||||||||||||||||

5. |

Fiduciary’s Share of Maryland Modifications (Enter the positive or negative number from Form 504 |

|

|

|

|

.00 |

|

|||||||||||||||||||||||||||||||||||

|

|

Schedule A line 8, 9d or 10f.) |

. . . . . . . . . |

|

. . . 對 |

5. |

|

|

|

|

||||||||||||||||||||||||||||||||

6. |

Line 4 plus or minus line 5 |

6. |

|

|

|

.00 |

|

|||||||||||||||||||||||||||||||||||

7. |

Nonresident beneficiary deduction from Form 504 Schedule A, line 13 |

|

|

|

|

|

|

|

|

7. |

|

|

|

.00 |

|

|||||||||||||||||||||||||||

.. |

. |

. . |

. . . . . . . . |

. . . |

|

. . . . . |

|

|

|

|

||||||||||||||||||||||||||||||||

8. |

.. . . . . . . .Maryland adjusted gross income (Subtract line 7 from line 6.) |

. . |

. . . . . . . . |

. . . |

|

. . . . . |

8. |

|

|

|

.00 |

|

||||||||||||||||||||||||||||||

9. |

. .. . .Maryland exemption. See Instruction 10 |

. |

. . . |

. . |

. . |

. . |

. |

|

. . . |

. |

. |

. . |

. |

. . |

. . . . . . . . |

. . . |

|

. . . . . |

9. |

|

|

|

.00 |

|

||||||||||||||||||

10. |

Fiduciary's Maryland taxable net income. (Subtract line 9 from line 8.) |

.. |

. |

. . |

. . . . . . . . |

. . . |

|

. . . . . |

10. |

|

|

|

|

.00 |

|

|||||||||||||||||||||||||||

|

|

NOTE: Nonresident fiduciary - see instruction for Form 504NR. |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||||||||||||||||||||||||

11. |

Maryland tax (Use rate schedule in instructions or enter amount from Form 504NR, line 21.) .. . . |

11. |

|

|

|

|

||||||||||||||||||||||||||||||||||||

|

|

MARYLAND |

FIDUCIARY INCOME |

2022 |

||

|

|

|

|

|

|

|

|

|

FORM |

TAX RETURN |

page 2 |

||

|

||||||

504 |

|

|

|

|

||

NAME |

|

|

FEIN |

|

|

|

12.Special nonresident tax Nonresidents: Enter the amount from Form 504NR, line 22.

(See Instruction 14.) Residents: Enter zero. .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12.

13. Total Maryland tax (Add lines 11 and 12.).. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13.

14.Credit for fiduciary income tax paid to another state and/or credit for preservation and conservation

easements from Part AA, line 1 and Part AA, line 6 of Form 502CR (Attach Form 502CR.).. . . . 14.

15. Enter the Nonrefundable Business Tax Credits from Part AAA of Form 504CR. . . . . . . . . . . . . . .  15.

15.

16. Total credits (Add lines 14 and 15).. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16.

17. Maryland Tax after credits (Subtract line 16 from line 13, if less than zero, enter zero)... . . . . . . 17.

18.Local tax (Multiply the fiduciary's Maryland taxable net income from line 10 by

19. |

.0 |

|

). See Instruction 15. |

. . . |

. . . . . . . . . . . |

18. |

|

|

|

|

|||||

Local Credit for fiduciary income tax paid to another state from Part BB of Form 502CR |

19. |

||||||

20. |

Local tax after credit. (Subtract line 19 from line 18.) If less than zero, enter zero |

20. |

|||||

21. |

Total Maryland and local tax. (Add lines 17 and 20.) |

. . . |

. . . . . . . . . . . |

21. |

|||

22. |

Contribution to Chesapeake Bay and Endangered Species Fund |

22. |

|

|

.00 |

||

23. |

. . . .Contribution to Developmental Disabilities Services and Support Fund |

23. |

|

|

.00 |

||

24. |

Contribution to Maryland Cancer Fund |

24. |

|

|

.00 |

||

25. |

.. . . . . . . . . . . . . . . . . . . .Contribution to Fair Campaign Financing Fund |

25. |

|

|

.00 |

||

26. |

Total Maryland income tax, local income tax and contributions (Add lines 21 through 25.). |

26. |

|||||

27. |

Maryland and local tax withheld. See Instruction 17 |

. . . |

. . . . . . . . . . . |

27. |

|||

28.Estimated tax payments and payments made with extension request and

with Form MW506NRS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .  28.

28.

29.Nonresident tax paid by

(Attach Maryland Schedule  29.

29.

30.Refundable Business and/or Heritage Structure Rehabilitation tax credits

|

(Attach Form 504CR and/or Form 502S.) |

. . . . . . . . . . |

. |

. . . . . . . . . . |

|

30. |

||

31. |

Total payments and credits (Add lines 27 through 30.) |

. . . . . . . . . . |

|

31. |

||||

32. |

Balance due (If line 26 is more than line 31, enter the difference.) |

. . . . . . . . . . |

|

32. |

||||

33. |

Overpayment (If line 26 is less than line 31, enter the difference.) |

. . . . . . . . . . |

|

33. |

||||

34. Amount of overpayment to be applied to 2023 estimated tax |

34. |

|||||||

35. |

.. . . . . . .Amount of overpayment to be refunded (Subtract line 34 from line 33.) |

REFUND |

|

35. |

||||

36. |

Interest charges from Form 504UP |

|

or for late filing |

|

|

. . . . Total |

36. |

|

|

|

|||||||

37. |

TOTAL AMOUNT DUE (Add lines 32 and 36.) |

. . . . . . . . . . |

. |

. . . . . . . . . . |

|

37. |

||

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.

.

.

.

.

.

.

.

.

.

.

AMENDED RETURNS

If you are filing an amended fiduciary income tax return, check the applicable boxes and draw a line through any bar codes on the front. Explain the changes you are making in the space below. Attach a copy of the amended federal Form 1041 if the federal return is being amended, and any other required documentation.

________________________________________________________________________________________________________

________________________________________________________________________________________________________

________________________________________________________________________________________________________

________________________________________________________________________________________________________

________________________________________________________________________________________________________

________________________________________________________________________________________________________

|

|

MARYLAND |

FIDUCIARY INCOME |

2022 |

||

|

|

|

|

|

|

|

|

|

FORM |

TAX RETURN |

page 3 |

||

|

||||||

504 |

|

|

|

|

||

NAME |

|

|

FEIN |

|

|

|

|

|

|

|

|||

________________________________________________________________________________________________________

DIRECT DEPOSIT OF REFUND (see Instruction 18)

Verify that all account information is correct and clearly legible. If you are requesting direct deposit of your refund, com- plete the following. For Splitting Direct Deposit, use Form 588.

Check here if this refund will go to an account outside of the United States.

Check here if you authorize the State of Maryland to issue your refund by direct deposit.

38.For the direct deposit option, complete the following information clearly and legibly:

38a. |

Type of account: |

38a. |

|

Checking |

|

Savings |

||

38b. |

Routing Number |

38b. |

|

|

|

|

|

|

38c. |

Account number: |

38c. |

|

|

|

|

|

|

38d. |

Name(s) as it appears on the bank account |

. 38d. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

SIGNATURE AND VERIFICATION

Check here

if you authorize your preparer to discuss this return with us.

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements and to the best of my knowledge and belief it is true, correct and complete. If prepared by a person other than taxpayer, the declaration is based on all information of which the preparer has any knowledge.

Signature of Fiduciary or Officer representing Fiduciary |

Date |

Printed name of the Preparer / or Firm's name |

|

Street address of Preparer or Firm's address

City, State, ZIP Code + 4

Signature of preparer other than fiduciary (Required by Law) |

Date |

Telephone number of preparer |

Preparer’s PTIN (Required by Law) |

Daytime telephone number (Fiduciary)

CODE NUMBERS (3 digits per line)

Nonresidents must include Form 504NR.

Make checks payable to and mail to:

Comptroller Of Maryland

Revenue Administration Division

110 Carroll Street

Annapolis, Maryland

(Write Your Federal Employer Identification Number On Check Using Blue Or Black Ink.)

File Breakdown

| Fact Number | Fact Detail |

|---|---|

| 1 | The form is designated for the Fiscal Year beginning 2008. |

| 2 | It accommodates various types of entities, including decedent’s estate, simple trust, complex trust, grantor type trust, bankruptcy estate, qualified funeral trust, and others. |

| 3 | Requires the federal employer identification number at the top of the form. |

| 4 | Asks for detailed information about the name of the estate or trust, name and title of fiduciary, and the fiduciary's address. |

| 5 | Includes sections for Decedent’s Estate Information if applicable, such as date of death, domicile of decedent, and decedent's Social Security number. |

| 6 | Enables the option to mark the return as amended and provides space for explaining the amendments. |

| 7 | Includes direct deposit option for refunds, requiring the type of account, routing number, and account number. |

| 8 | Governed by Maryland state law and aimed to be filed with the Comptroller of Maryland, Revenue Administration Division. |

Steps to Filling Out Maryland 504

Filling out the Maryland 504 Fiduciary Income Tax Return can seem daunting at first, but with a step-by-step guide, the process becomes straightforward. This form is designed for fiduciaries to report income, losses, and other financial information for a trust or estate. Let's break down the steps to complete this form accurately.

- At the top of the form, write the fiscal year beginning and ending dates.

- Enter the Federal Employer Identification Number (FEIN) of the estate or trust.

- Fill in the name of the estate or trust, followed by the name and title of the fiduciary.

- Provide the address of the fiduciary, including the number, street, city or town, state, and zip code.

- Indicate the type of entity by checking the appropriate box for decedent’s estate, simple trust, complex trust, grantor type trust, bankruptcy estate, qualified funeral trust, or other.

- If applicable, for decedent’s estates, enter the date of death, domicile of the decedent, and the decedent’s Social Security Number. Check the box if it is a final return.

- Mark the resident status and amended return information if it applies. If a subdivision code or explanation for the amended return is necessary, include it.

- Enter the Federal taxable income of the fiduciary as shown on line 22 of the federal Form 1041.

- Record the exemption claimed on the federal return.

- Add lines 21 and 22, then enter the total.

- Detail the fiduciary’s share of Maryland modifications on page 2, then include the result on line 24.

- Calculate the line item 23 plus or minus line 24, and enter the result.

- If there are nonresident beneficiaries, complete the nonresident beneficiary deduction section and enter the result on line 26.

- Subtract line 26 from the result of line 25 to calculate the Maryland adjusted gross income.

- Enter the Maryland exemption amount.

- Subtract the Maryland exemption from the Maryland adjusted gross income to find the Maryland taxable net income.

- Calculate and enter the Maryland tax, using the rate schedule or Form 504NR for nonresident fiduciaries.

- If applicable, calculate and enter the local or special nonresident tax.

- Add the total Maryland and local tax.

- Decide on contributions to various funds if applicable and enter the amounts.

- Add the total Maryland income tax, local income tax, and contributions.

- Enter the amount of Maryland and local tax withheld, estimated tax payments, and any credits.

- Calculate the balance due or overpayment, and decide on the allocation of any overpayment.

- If opting for direct deposit, fill in the type of account, routing number, and account number.

- Sign and date the form. If prepared by someone other than the fiduciary, include the preparer’s information.

After completing the form, review it thoroughly to ensure all information is accurate and complete. Mail the completed form along with any necessary attachments to the Comptroller of Maryland, Revenue Administration Division at the address provided on the form. This step is crucial for the timely processing of your fiduciary income tax return.

More About Maryland 504

What is the Maryland 504 Form?

The Maryland 504 Form, also known as the Fiduciary Income Tax Return, is a document filed by the fiduciaries of estates and trusts. It reports income, deductions, gains, losses, and taxes due or refundable to the state. This form applies to decedent’s estates, simple trusts, complex trusts, grantor type trusts, bankruptcy estates, qualified funeral trusts, among others.

Who needs to file a Maryland 504 Form?

This form must be filed by fiduciaries of estates and trusts that have Maryland income tax filing requirements. The responsibility generally falls on executors, administrators, or trustees who manage assets on behalf of another.

What information do I need to fill out Form 504?

To accurately complete the form, you'll need:

- Federal employer identification number

- Name and title of the fiduciary

- Address of the fiduciary

- Date of death and domicile of decedent, if applicable

- Federal taxable income of the fiduciary

- Details of any nonresident beneficiary deductions

- Details of any credits, deductions, and taxes paid to other states or for preservation and conservation easements

- Information on direct deposit for refunds if applicable

What are the different types of trusts and estates mentioned in the form?

The form categorizes entities into several types: decedent’s estates, simple trusts, complex trusts, grantor type trusts, bankruptcy estates, qualified funeral trusts, and others. Each category has different rules and taxation structures reflecting the nature of the entity.

How do I calculate Maryland taxable income for a fiduciary?

Calculate the Maryland taxable income by starting with the federal taxable income, adding specific modifications for income and deductions relevant to Maryland law, and then applying any allowable deductions for nonresident beneficiaries. This figure is adjusted by exemptions and rates specific to Maryland to determine the state taxable income.

Is it possible to file an amended Maryland 504 Form?

Yes, if you need to make changes after originally filing, you can submit an amended 504 Form. Remember to check the box indicating it's an amended return, provide an explanation for the changes, and attach any required documentation, including a copy of the amended federal Form 1041 if applicable.

What if a beneficiary is a nonresident of Maryland?

Special rules apply for nonresident beneficiaries. Fiduciaries must complete specific sections of the form to calculate income attributable to nonresidents and related expenses, potentially adjusting the taxable income and deductions accordingly.

How are contributions to Maryland funds reported on the form?

Fiduciaries can choose to contribute to funds like the Chesapeake Bay and Endangered Species Fund, the Fair Campaign Financing Fund, and the Maryland Cancer Fund. These contributions are reported in the relevant sections of the form and are added to the total tax or refund.

Where and how can fiduciaries file the Maryland 504 Form?

The completed form can be mailed to the Comptroller of Maryland. Fiduciaries are encouraged to ensure that all information is accurate and to include the fiduciary’s federal employer identification number on the check if a payment is due. For efficiency and security, consider direct deposit for refunds by supplying the correct account information on the form.

Common mistakes

When completing the Maryland 504 fiduciary income tax return, individuals often encounter pitfalls that can result in errors, misunderstandings, or even penalties. These mistakes can delay processing times, lead to incorrect tax calculations, and cause unnecessary stress. Recognizing and avoiding these common errors can streamline the filing process, ensuring accuracy and compliance with state regulations.

- Not correctly identifying the type of entity being reported. This misstep, such as confusing a simple trust with a complex trust, can impact the tax implications and the necessary documentation.

- Inaccurately reporting the decedent’s estate information, including the date of death and domicile of decedent, which are crucial for determining the tax base correctly.

- Failing to accurately indicate the resident status of the fiduciary or beneficiary, thereby miscalculating the portion of income subject to Maryland state tax.

- Incorrect calculation or reporting of the federal taxable income of the fiduciary from line 22 of federal Form 1041, which serves as the foundation for Maryland tax computations.

- Mishandling the completion of the nonresident beneficiary deduction section, when applicable, which could lead to overpaying or underpaying state taxes.

- Omitting or inaccurately reporting contributions to state funds such as the Chesapeake Bay and Endangered Species Fund, Fair Campaign Financing Fund, and Maryland Cancer Fund, potentially missing out on tax deductions or credits.

- Incorrectly calculating the total Maryland and local tax or misunderstanding the instructions related to local or special nonresident tax which impacts the final tax liability.

- Overlooking the declaration regarding the direct deposit of refunds, leading to delays in receiving owed funds or misrouting of funds due to incorrect account information.

- Improperly handling amended returns, including a failure to check the applicable boxes, not drawing a line through barcodes when filing an amended return, and not providing a comprehensive explanation of changes.

Ensuring the accuracy of these elements when filling out the Maryland 504 form can prevent delays, avoid potential fines or additional taxes, and guarantee the fiduciary meets their legal obligations.

Documents used along the form

When managing estates or trusts in Maryland, the FORM MARYLAND 504 FIDUCARY INCOME TAX RETURN is a crucial document for reporting income. However, it's often just the tip of the iceberg. Several other forms and documents are frequently used alongside this form to ensure comprehensive and compliant financial management. Understanding these documents can help in preparing for the complex task of fiduciary accounting and reporting. Here's a closer look at some of these essential forms.

- Form 504NR: This form is for non-residents of Maryland and accompanies the main 504 form if the fiduciary or the beneficiaries are not residents. It helps calculate the taxable income derived from Maryland sources.

- Schedule K-1 (504): Used to report each beneficiary's share of income, deductions, and credits from the estate or trust, this form ensures proper distribution of financial information for individual tax reporting purposes.

- Form 1041: The U.S. Income Tax Return for Estates and Trusts is a federal form required by the IRS. It serves as a reference for the 504 form, particularly in determining federal taxable income and deductions.

- Form 500CR: This form is used to claim business tax credits for estates or trusts eligible for various Maryland tax credits, often impacting the overall tax liability reported on the Maryland 504 form.

- Form 502H: Employed when an estate or trust is claiming a heritage structure rehabilitation credit, it's attached to the 504 to account for specific tax credits related to property maintenance and preservation.

- Form MW506NRS: Required for non-resident sale of property, this form is crucial if the estate or trust sells real estate during the tax year, affecting the overall income and deductions reported.

- Form 504UP: This underpayment of estimated tax form is needed if the estate or trust didn’t pay enough in taxes throughout the year, either through withholdings or estimated tax payments.

- Amended Federal Form 1041: If changes to the federal tax return are made after submitting the Maryland 504 form, an amended federal return must be filed alongside an amended Maryland 504 to reflect those corrections.

In conclusion, handling fiduciary accounting and tax reporting in Maryland requires a thorough approach, involving several forms beyond the Maryland 504. Familiarity with these documents can streamline the process, ensuring compliance and minimizing potential errors. Whether you're a professional fiduciary or managing a trust as a personal responsibility, understanding each form's role and requirements is essential for effective administration.

Similar forms

The Maryland 504 form is similar to the Federal Form 1041, U.S. Income Tax Return for Estates and Trusts, in several key aspects. Both forms serve the fundamental purpose of reporting income, deductions, and taxes for entities that are not individual taxpayers but operate to hold and manage the assets for the benefit of others. Specifically, they collect information on the type of entity, such as an estate or various types of trusts, and detail the taxable income generated, adjustments made to this income, and the tax liability due or refund owed. Each form requires the filer to indicate the type of entity being reported, such as a decedent's estate, simple trust, complex trust, or grantor trust, among others. Additionally, both necessitate detailed information on the fiduciary or officer responsible for the return, including name, title, and contact information. Thus, while tailored to their specific tax jurisdictions, Maryland's 504 and the Federal 1041 share a common structure and purpose in fiduciary tax reporting.

Another document related to the Maryland 504 form is Form 504NR, Nonresident Income Tax Return. Form 504NR allows fiduciaries of estates or trusts with nonresident beneficiaries to calculate the tax attributable to income derived from Maryland sources. This form complements the 504 by focusing on the allocation of income and tax liabilities to nonresidents, showing specific calculations for deductions and modifications related to nonresident income. It ensures that Maryland can accurately tax income distributed to beneficiaries living outside the state, similar to how the main 504 form manages tax responsibilities for resident entities. Both forms require detailed accounting of income, deductions, and beneficiary information, highlighting the state's interest in ensuring all eligible income is taxed appropriately, whether the beneficiary resides within Maryland or elsewhere.

Dos and Don'ts

When filling out the Maryland 504 form, there are certain practices that should be followed to ensure accuracy and compliance with state requirements. Here are five key do's and don'ts that can guide you through the process:

Do:- Review the entire form and its instructions carefully before beginning to fill it out to ensure you understand all requirements and avoid any oversights.

- Double-check the Federal employer identification number and all other identification information to ensure they are correct. Mistakes in identification numbers can lead to processing delays.

- Report all income and deductions accurately, using the instructions to correctly calculate figures such as the fiduciary's share of Maryland modifications and nonresident beneficiary deductions.

- Attach all required forms and documentation, such as the Federal Form 1041, Schedule K-1 for beneficiaries, and any forms related to credits for taxes paid to other states.

- Sign and date the form, and ensure it's mailed to the correct address provided by the Comptroller of Maryland. Also, include a daytime phone number in case the fiduciary needs to be contacted.

- Overlook the need to attach an explanation if this is an amended return. Failure to provide an adequate explanation of the changes can result in processing delays or inquiries.

- Forget to check the appropriate boxes for type of entity, resident status, and whether it's a final return. Incorrectly marking these boxes can lead to inaccurate processing.

- Miscalculate deductions and credits, such as the nonresident beneficiary deduction or the credit for fiduciary income tax paid to another state. Inaccuracies may result in underpayment or overpayment of taxes.

- Use incorrect tax rates or fail to use the rate schedule provided in the instructions for calculating Maryland tax and local or special nonresident tax. This could lead to incorrect tax liabilities being reported.

- Ignore instructions for direct deposit of refunds or inaccurately fill out the direct deposit information, which can delay or misdirect your tax refund.

Misconceptions

One common misconception is that the Maryland 504 form is only for large estates or trusts. Actually, this form is for all estates and trusts that have taxable income, assets, or conduct business in Maryland, regardless of their size.

Another misunderstanding is that this form is complicated and time-consuming to fill out. While it requires careful attention to details, the instructions provided with the form guide filers through the process, making it more manageable than some may assume.

Many people mistakenly believe that only a lawyer or professional accountant can correctly complete the Maryland 504 form. In reality, with the right information and careful reading of the instructions, a fiduciary can accurately complete the form without professional help.

Some think this form is only for filing annual income tax returns. However, it is also used to report changes in the estate or trust, such as a change in fiduciary or address, and to amend previously filed returns.

A common incorrect assumption is that the Maryland 504 form does not need to be filed if the estate or trust does not owe any taxes. Even if no tax is due, filing this form is necessary to comply with Maryland tax law and avoid potential penalties.

There's a false belief that direct deposit for refunds is not available through this form. On the contrary, filers can request a refund to be directly deposited into a bank account, a convenient option clearly indicated in the form's instructions.

Many assume that fiduciaries must pay taxes on out-of-state income. While Maryland taxes worldwide income, the form allows for a credit for taxes paid to other states, preventing double taxation of the same income.

Others believe that if an estate is not finalized by the end of the year, they cannot file a Maryland 504 form. This is not true; estates, in particular, may need to file returns for multiple years. The form has a checkbox indicating whether it is a final return, signaling that the estate has been closed.

Some people are under the impression that the form does not allow for deductions or modifications to income. However, the form provides sections for reporting additions and subtractions to income, as well as deductions for nonresident beneficiaries, ensuring that the taxable income is accurately reported.

Key takeaways

Filling out the Maryland Form 504, the Fiduciary Income Tax Return, is a detailed process that requires precision and understanding of the estate or trust’s financial activities over the fiscal year. Here are some key takeaways to help navigate the filing process effectively:

- Identify the type of entity correctly: It’s crucial to check the appropriate box that corresponds with the nature of the fiduciary entity, such as a decedent’s estate, simple trust, complex trust, or grantor type trust, among others. This classification affects the tax treatment and obligations of the entity.

- Report all necessary income and deductions accurately: Line 21 requires the fiduciary to report the federal taxable income, which is pivotal as it forms the basis for calculating the income subject to Maryland tax. Remember to include any exemptions claimed on the federal return, as noted on Line 22.

- Understand Maryland modifications: Maryland requires specific additions and subtractions to the income reported on the federal return to arrive at the Maryland taxable income. It’s important to carefully complete the Fiduciary’s Share of Maryland Modifications section to ensure compliance with state-specific tax laws.

- Manage nonresident beneficiary deductions properly: If the entity has beneficiaries who are nonresidents of Maryland, the fiduciary must complete the section for Nonresident Beneficiary Deduction. This ensures that income attributable to nonresidents is handled according to Maryland regulations, potentially affecting the entity’s tax liability.

By maintaining a thorough record of income and deductions while closely following the instructions provided with Form 504, fiduciaries can fulfill their tax obligations accurately. Additionally, understanding the nuances of Maryland’s modifications to federal taxable income and correctly accounting for nonresident beneficiaries can help avoid common mistakes and ensure the smooth processing of the return.

Common PDF Templates

Does Maryland Have Personal Property Tax - For businesses in Maryland, Form 4A is a critical document for declaring their financial status, ensuring compliance with state laws.

Maryland Credentialing Application - The application outlines specific documentation needed for various application types, from first-time applicants to those upgrading their credential.

Maryland Tax Withholding - Nonresident filers can allocate overpayments towards next year's estimated taxes or request a refund for the difference.