Maryland 504E PDF Template

The Maryland 504E form stands as a crucial document for fiduciaries overseeing estates or trusts, guiding them through the process of requesting an extension to file their fiduciary income tax return. This application enables a six-month delay, provided that it’s accurately completed, submitted by the return's due date, and accompanied by the due tax amount indicated in the tax payment worksheet. Fiduciaries may find it necessary to request an extension beyond six months, which is allowed under specific circumstances such as being outside the United States, albeit such extensions will not surpass one year from the original filing deadline. It's important to note this form doesn’t grant an extension for tax payment; taxes are due by the regular deadline to avoid interest and penalties. Whether filed for a calendar year or on a fiscal basis, the deadline for submitting this form aligns with the return due date, ensuring fiduciaries manage their financial responsibilities timely. The instructions provided emphasize the importance of correct form completion, timely filing, and the necessity of paying the calculated tax amount on line 6 to benefit from the extension. Failure to comply with these requirements results in interest charges and penalties, reinforcing the imperative of diligent tax management. The venue for submission, Maryland Revenue Administration Division in Annapolis, stands ready to receive this crucial documentation, marking a pivotal step in the fiscal management of estates and trusts within Maryland.

Maryland 504E Sample

FORM |

MARYLAND |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2011 |

APPLICATION FOR |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

504E EXTENSION TO FILE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

FIDUCIARY INCOME TAX RETURN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

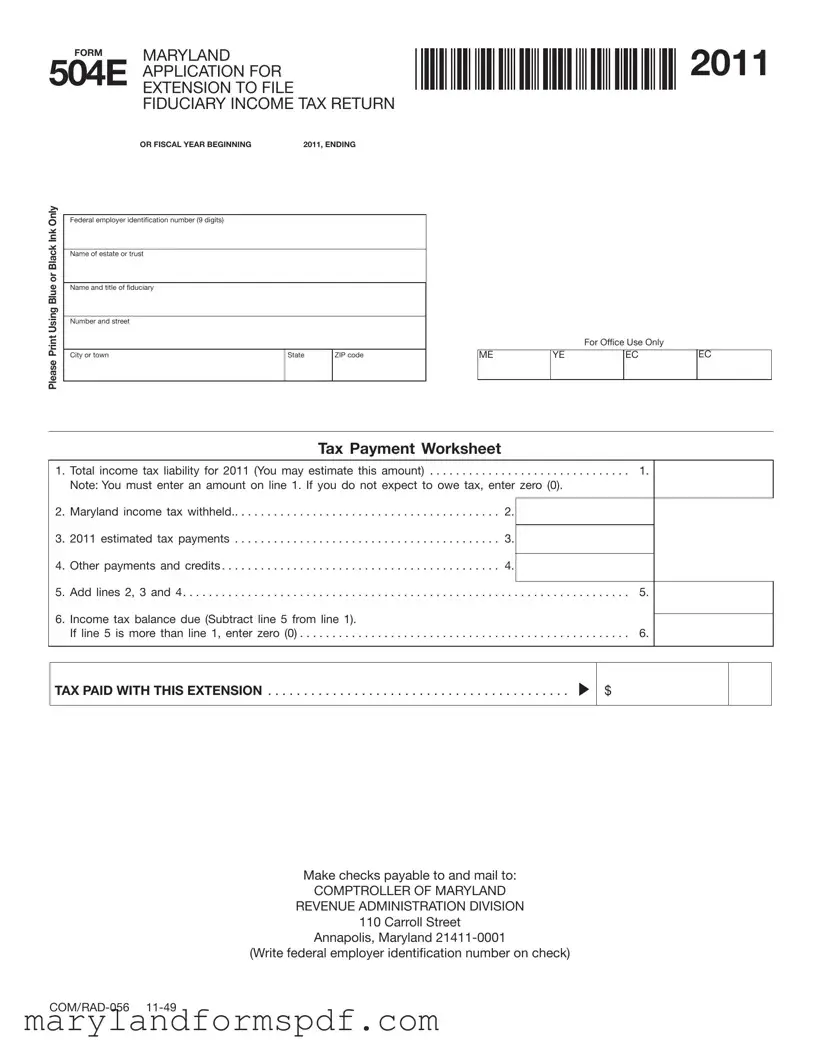

OR FISCAL YEAR BEGINNING |

2011, ENDING |

OnlyInk |

|

|

|

|

|

Federal employer identification number (9 digits) |

|

|

|

|

|

|

|

|

Blackor |

|

|

|

|

|

Name of estate or trust |

|

|

|

|

|

|

|

|

Blue |

Name and title of fiduciary |

|

|

|

|

|

|

||

UsingPrint |

|

|

|

|

Number and street |

|

|

||

|

|

|

|

|

|

|

|

|

|

Please |

City or town |

State |

ZIP code |

|

|

|

|

||

|

|

|

||

ME

For Office Use Only

YE |

EC |

EC |

|

|

|

Tax Payment Worksheet

1. |

Total income tax liability for 2011 (You may estimate this amount) |

. . . . . . . . . . . . . . . . .. . .1. |

|

|

|

Note: You must enter an amount on line 1. If you do not expect to owe tax, enter zero (0). |

|

||

2. |

Maryland income tax withheld |

2. |

|

|

|

|

|||

3. |

2011 estimated tax payments |

3. |

|

|

|

|

|||

4. |

Other payments and credits |

4. |

|

|

|

|

|||

|

|

|

|

|

5. |

Add lines 2, 3 and 4 |

. . .5 |

|

|

6. |

Income tax balance due (Subtract line 5 from line 1). |

|

|

|

|

|

|

||

|

If line 5 is more than line 1, enter zero (0) |

. . .6 |

|

|

|

|

|

|

|

TAX PAID WITH THIS EXTENSION |

|

|

$ |

|

. |

|

|

||

|

|

|

|

|

Make checks payable to and mail to:

COMPTROLLER OF MARYLAND

REVENUE ADMINISTRATION DIVISION

110 Carroll Street

Annapolis, Maryland

(Write federal employer identification number on check)

INSTRUCTIONS FOR

FORM 504E 2011

MARYLAND

APPLICATION FOR EXTENSION TO FILE FIDUCIARY INCOME TAX RETURN

PAGE 2

GENERAL INSTRUCTIONS

Purpose of Form

Use Form 504E to receive an automatic six month extension to file Form 504.

To get the extension you MUST:

1.fill in Form 504E correctly AND

2.file it by the due date of your return AND

3.pay ALL of the amount shown on line 6.

Fiduciaries requesting an extension of more than six months must enter on this application the reason for the request. No extension request will be granted for more than six months, except in the case of a fiduciary who is out of the United States. In no case will an extension be granted for more than one year from the due date for submitting the fiduciary tax return. See Administrative Release 4.

When to File Form 504E

File Form 504E by April 15, 2012. If you are filing on a fiscal year basis, file by the regular due date of your return.

Where to File

Mail this form to the Maryland Revenue Administra- tion Division, 110 Carroll Street, Annapolis, MD

Filing Your Tax Return

You may file Form 504 at any time before the end of the extension period. Remember, Form 504E does not extend the time to pay taxes. If you do not pay the amount due by the regular due date, you will owe interest and be subject to a penalty.

Interest

You will owe interest on tax not paid by the regular due date of your return. The interest will accrue until you pay the tax. Even if you had a good reason not to pay on time, you will still owe interest.

Penalty

If tax and interest is not paid promptly, a penalty will be assessed on the tax.

How to Claim Credit for Payment Made with This Form

When you file your return, show the amount of any payment (line 6) sent with Form 504E on line 31 of your return.

File Breakdown

| Fact Name | Description |

|---|---|

| Purpose | The Maryland 504E form is used to apply for an automatic six-month extension to file the fiduciary income tax return (Form 504). |

| Requirements for Extension | To qualify for the extension, filers must correctly complete Form 504E, submit it by the original due date of the return, and pay the total amount due indicated on the form. |

| Extended Deadline for Fiduciaries Outside the U.S. | Fiduciaries residing outside the United States may request an extension exceeding six months, but not more than one year from the original due date for filing the fiduciary tax return. |

| Due Date | Form 504E must be filed by April 15, 2012, or by the regular due date of the return if filing on a fiscal year basis. |

| Filing Location | The form should be mailed to the Maryland Revenue Administration Division at 110 Carroll Street, Annapolis, MD 21411-0001. |

| Interest and Penalty | Interest accrues on unpaid taxes after the regular due date, and penalties apply for late payment of tax and interest, regardless of the reason for delay. |

Steps to Filling Out Maryland 504E

Completing the Maryland 504E form is a necessary step for obtaining an extension for filing a fiduciary income tax return. This form is used specifically for estates or trusts that need more time to gather the required information to accurately file their tax returns. Filling out this form correctly and submitting it on time, along with the necessary payment, ensures that the estate or trust can avoid penalties associated with late filing. It's important to remember, however, that this extension only applies to the filing of the tax return, not to any taxes owed. Following these steps will guide you through the process of filling out the Maryland 504E form.

- Write the federal employer identification number in the designated space. This number should be nine digits long and identifies the estate or trust.

- Print the name of the estate or trust in the space provided.

- Enter the name and title of the fiduciary. This is the person responsible for managing the estate or trust.

- Provide the address of the fiduciary by filling in the number and street, city or town, state, and ZIP code fields.

- For the Tax Payment Worksheet:

- Line 1: Enter the total income tax liability for the year 2011. If you're unsure of the exact amount, provide an estimate. If no tax is due, write zero (0).

- Line 2: Note any Maryland income tax that has already been withheld here.

- Line 3: State the amount of any estimated tax payments made for 2011.

- Line 4: List any other payments and credits towards the tax liability.

- Line 5: Add lines 2, 3, and 4 together and write the sum.

- Line 6: Subtract line 5 from line 1 to find the income tax balance due. If the total of lines 2 through 4 is greater than line 1, enter zero (0).

- Write the total tax paid with this extension next to the dollar sign. Make sure to make the check payable to the Comptroller of Maryland and note the federal employer identification number on the check.

- Mail the completed form and any payment due to: COMPTROLLER OF MARYLAND REVENUE ADMINISTRATION DIVISION, 110 Carroll Street, Annapolis, Maryland 21411-0001.

After the form is submitted, focus can shift to gathering the necessary documentation and information to file a comprehensive and accurate fiduciary income tax return. Keep in mind that even with an extension, any taxes owed should be paid by the original due date to avoid interest and penalties. The extension provides additional time for filing the paperwork but does not extend the time for tax payment. Use the extension period wisely to ensure all information is correct and complete for submission.

More About Maryland 504E

What is the purpose of Form 504E?

Form 504E serves to provide an automatic six-month extension for filing Form 504, the Fiduciary Income Tax Return in Maryland. To qualify for this extension, fiduciaries must accurately complete Form 504E, submit it by the due date of the original return, and pay the total tax amount due as indicated on line 6 of the form. Fiduciaries who require an extension beyond six months, including those outside the United States, must specify their reasons on the application, though no extension can exceed one year from the original return's due date.

When should Form 504E be filed?

Form 504E must be filed by April 15, 2012, for the tax year beginning in 2011. If filing on a fiscal year basis, it should be submitted by the regular due date of your return. Filing by these deadlines ensures eligibility for the six-month extension.

Where do I file Form 504E?

This form should be mailed to the Maryland Revenue Administration Division at 110 Carroll Street, Annapolis, MD 21411-0001. Ensure to include the federal employer identification number on the check if making a payment.

Does Form 504E extend the deadline to pay taxes?

No, filing Form 504E does not extend the time to pay any taxes due. The form only extends the deadline for filing Form 504. Taxes owed should still be paid by the original due date to avoid additional interest or penalties.

What happens if I don't pay the tax by the due date?

If taxes are not paid by the original due date, interest will accrue on the unpaid amount from the due date until the tax is fully paid. Additionally, failure to pay taxes promptly may result in penalties on the owed tax amount.

How is interest calculated on unpaid taxes?

Interest on any unpaid tax is calculated from the original due date of the return until the tax is paid in full. This interest is due even if there was a reasonable cause for not paying on time.

What penalties may apply if tax and interest are not paid timely?

If tax and accrued interest are not paid promptly, a penalty will be assessed on the unpaid tax amount. This is in addition to any interest charges.

How do I claim credit for payment made with this form?

When you file your Form 504, indicate the payment made with Form 504E (as shown on line 6) on line 31 of your return. This ensures that your payment is credited correctly towards your tax liability.

Common mistakes

Filling in incorrect information: Often, people might accidentally enter incorrect details such as the wrong Federal employer identification number, or they might misspell the name of the estate or trust. It's essential to double-check all information before submission to ensure accuracy.

Estimating tax liability inaccurately: On line 1 of the Tax Payment Worksheet, you are required to enter your total income tax liability for the year. A common mistake is either overestimating or underestimating this amount. It's crucial to make this estimation as accurate as possible to avoid future penalties or an unexpected tax bill.

Omitting necessary payments: Lines 2 through 4 on the worksheet ask for specifics about Maryland income tax withheld, estimated tax payments for 2011, and other payments and credits. Neglecting to include these payments can lead to inaccuracies in calculating the income tax balance due on line 6, which, in turn, affects the amount that should accompany the extension request.

Missing the deadline: Form 504E must be filed by April 15, 2012, or by the due date of the return if filing on a fiscal year basis. Waiting until the last minute can lead to missed deadlines primarily due to overlooked details or unforeseen circumstances. To avoid penalties and interest for late filing and payment, it's advisable to prepare and submit this form well before the deadline.

Documents used along the form

When preparing for tax submissions, particularly concerning the Maryland Form 504E for fiduciary income tax extensions, it's crucial to be aware of and gather other essential documents and forms that may need to be filed in conjunction. The following list provides a snapshot of additional forms and documents often utilized alongside the Maryland 504E form to ensure thorough and compliant tax filing practices for estates or trusts.

- Form 504 - Maryland Fiduciary Income Tax Return: This is the main form for which Form 504E provides an extension. It reports income, deductions, and credits of estates and trusts.

- Form 502 - Maryland Resident Income Tax Return: Used by residents of Maryland to file personal income taxes. This form might be necessary if the fiduciary or estate also involves individual tax reporting requirements.

- Form 505 - Nonresident Income Tax Return: Required for income generated in Maryland by nonresidents, including fiduciaries or beneficiaries not residing in Maryland.

- Form 500 - Corporation Income Tax Return: Relevant for estates or trusts involved with business entities, this form reports income, losses, and taxes due for corporations.

- Form 510 - Pass-Through Entity Income Tax Return: Necessary for reporting income, losses, and other financial information for entities like partnerships or S corporations, which could be part of the estate or trust.

- Form MW506NRS - Nonresident Sale of Real Property: Required if the estate or trust sold real property during the tax year, to ensure proper tax withholding and reporting for nonresidents.

Each of these documents serves a specific function in conjunction with the Maryland 504E form, addressing various aspects of estate and trust taxation, as well as individual and business tax considerations. Properly identifying and completing the relevant forms ensures compliance with Maryland tax laws and facilitates the accurate and timely management of fiduciary responsibilities.

Similar forms

The Maryland 504E form is designed to grant an extension for filing fiduciary income tax returns. Its structure and purpose bear resemblance to other tax extension forms, such as the IRS Form 4868 and the IRS Form 7004, which offer extensions for individual and business tax filings, respectively.

IRS Form 4868 is the Application for Automatic Extension of Time To File U.S. Individual Income Tax Return. Like the Maryland 504E, Form 4868 does not extend the time to pay any tax due but grants additional time to file the tax return itself. Taxpayers are required to estimate their tax liability and should pay any amount due by the original filing deadline to avoid or minimize interest and penalties. The primary similarity lies in the forms' function: both are aimed at providing taxpayers extra time to gather necessary information and complete their returns accurately. However, while Form 4868 applies to individual income taxes, the Maryland 504E is specific to fiduciary income tax returns.

IRS Form 7004 is the Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns. This form, akin to the Maryland 504E, offers businesses and other entities the opportunity to receive an extension for filing their tax returns. Form 7004 is applicable to a wide range of tax returns, including corporate, partnership, and certain trust and estate returns. Both forms require the taxpayer to provide basic identifying information and to calculate the total tax liability expected for the year, emphasizing the necessity to pay all or an estimated portion of the owed tax by the due date. While Form 7004 caters to a broad spectrum of entities with varying tax obligations, the Maryland 504E specifically addresses fiduciaries responsible for managing estate or trust income tax filings.

Dos and Don'ts

When filling out the Maryland 504E form for an extension to file a fiduciary income tax return, it's important to follow certain guidelines to ensure the process goes smoothly. Here are some dos and don'ts:

Do:- Fill in the form correctly: Ensure all information is accurate and complete to avoid any processing delays.

- File by the due date: Submit Form 504E by April 15, 2012, or by the regular due date of your return if filing on a fiscal year basis to receive the automatic six-month extension.

- Pay the amount shown on line 6: To avoid interest and penalties, pay the entire balance due with the extension request.

- Include your federal employer identification number on the check: This ensures your payment is correctly applied to your account.

- Use black or blue ink: To ensure legibility and proper scanning of the form.

- Mail to the correct address: Send your completed form and payment to the Maryland Revenue Administration Division, 110 Carroll Street, Annapolis, MD 21411-0001.

- Estimate tax liability inaccurately: While you may estimate your 2011 income tax liability, strive for accuracy to avoid underpayment or overpayment.

- Ignore the line 6 amount: Not paying the income tax balance due with the extension could result in added interest and penalties.

- Forget to claim your payment on your return: Remember to show the amount of any payment sent with Form 504E on line 31 of your return.

- Delay beyond the filing deadline: Filing Form 504E past the deadline will not secure an extension and may result in penalties.

- Overlook the purpose of the form: Understand that Form 504E is for an extension to file the return, not an extension to pay any tax due.

- Submit incomplete or illegible forms: Ensure all fields are completed and the form is readable to prevent processing issues.

Misconceptions

Understanding legal forms and their purposes can often seem daunting, and the Maryland 504E form is no exception. Myths and misconceptions about this specific form can lead to confusion and potentially costly mistakes. Here, we aim to dispel some of these misconceptions with clear, factual information.

- Misconception #1: The Maryland 504E form extends the time to pay taxes.

One common mistake is thinking that filing Form 504E gives you extra time to pay your fiduciary income taxes. However, the truth is that this form only extends the filing deadline for the fiduciary income tax return. Taxes due must still be paid by the original deadline to avoid interest and penalties, emphasizing the importance of planning your payments accordingly.

- Misconception #2: You can request an extension at any time.

Another misunderstanding is regarding the timing of the extension request. It's crucial to file Form 504E by the due date of your original tax return. Waiting until after this date to file for an extension will not be valid, and the request for an extension must be accompanied by the full payment of any taxes owed, showcased by line 6 of the form.

- Misconception #3: Filing Form 504E is optional if you don’t owe any taxes.

Even if you estimate that you won't owe any taxes, you're still required to fill out and submit Form 504E by the deadline if you seek an extension to file your fiduciary income tax return. Entering zero on line 1 is necessary when you believe no tax is due, ensuring compliance with Maryland tax filing requirements.

- Misconception #4: The form allows for an indefinite extension.

Some might think that extensions granted via Form 504E can be indefinite or for an arbitrary length of time. In actuality, the form grants a specific six-month extension period, with the possibility of more than six months but never exceeding one year, and only under certain circumstances like the fiduciary being outside the United States. This structured timeline helps in planning your fiscal responsibilities better.

In conclusion, understanding the purpose and proper use of the Maryland 504E form is vital for anyone responsible for managing fiduciary income tax filings. Dispelling these misconceptions aids in ensuring that these filings are both timely and compliant with state requirements, ultimately avoiding unnecessary fines and interest.

Key takeaways

Filing the Maryland 504E form is crucial for fiduciaries or trustees managing estates or trusts who need more time to prepare their fiduciary income tax returns. Understanding the core principles and deadlines regarding this form can help ensure compliance while avoiding unnecessary penalties or interest charges. Here are key takeaways to consider:

- The Maryland 504E form serves to grant an automatic six-month extension for filing Form 504, the Fiduciary Income Tax Return. This extension is vital for fiduciaries who require additional time to gather necessary information and complete their tax filings accurately.

- To qualify for this extension, fiduciaries must correctly fill out the form, file it by the original due date of the return, and pay the total amount of estimated tax due as indicated on line 6 of the form. This requirement underscores the importance of accurately estimating the tax liability to avoid underpayment penalties.

- The form must be submitted by April 15 following the tax year, or by the regular due date of the return if the estate or trust operates on a fiscal year basis. Timely submission is crucial to avoid late filing penalties and to ensure the extension is granted.

- While Form 504E extends the deadline for filing the fiduciary income tax return, it does not extend the time to pay the due taxes. Fiduciaries should note that interest and penalties may accrue on taxes not paid by the original due date, regardless of the extension to file. Additionally, when the actual tax return is filed, any payment made with Form 504E should be claimed on line 31 of the return to properly credit the estate or trust for payments made.

In summary, the Maryland 504E form is an essential tool for fiduciaries managing the affairs of estates or trusts, providing needed additional time to accurately complete their fiduciary income tax returns. Proper understanding and adherence to the guidelines for filling out and submitting this form can help avoid complications, ensuring that fiduciary responsibilities are met without incurring extra costs.

Common PDF Templates

Net Tangible Benefit Fannie Mae - Obtaining a lower interest rate or monthly payment, and other benefits, must be clearly substantiated on the worksheet.

Maryland Form 502 Instructions - Provides avenues for taxpayers to receive benefits for investments in Maryland’s future.