Maryland 505 PDF Template

Understanding the nuances of state-specific tax forms is essential for nonresidents who earn income across state lines, and the Maryland Form 505 stands as a critical document in this process for those with income sources in Maryland. Tailored for nonresidents, the form meticulously guides taxpayers through the complexities of reporting income earned within the state for the 2005 fiscal year. It covers various income sources, including wages, dividends, and business income, adjusting for state-specific exclusions and exemptions. Recognizing the diverse nature of taxpayer circumstances, it also delineates options for filing status, such as single or married filing jointly, and accommodates exemptions for oneself, a spouse, dependents, and other qualifiers like age or blindness. Furthermore, it encompasses sections for deductions, either standard or itemized, gearing towards a precise calculation of taxable income. Maryland's approach, encapsulated in Form 505, illustrates the state's attempt to streamline tax filing for nonresidents, ensuring proper tax collection while considering the intricacies of individual taxpayer situations.

Maryland 505 Sample

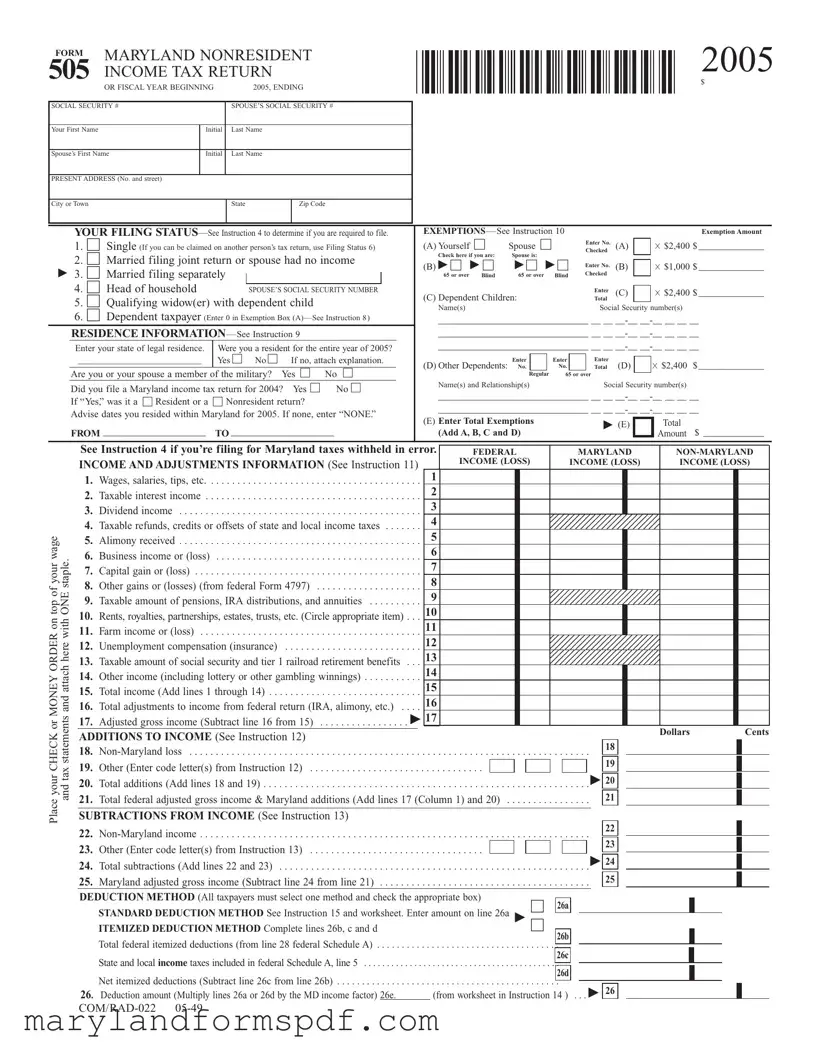

FORM MARYLAND NONRESIDENT 505 INCOME TAX RETURN

OR FISCAL YEAR BEGINNING |

2005, ENDING |

2005

$

SOCIAL SECURITY # |

|

SPOUSE’S SOCIAL SECURITY # |

|

|

|

|

|

Your First Name |

Initial |

Last Name |

|

|

|

|

|

Spouse’s First Name |

Initial |

Last Name |

|

|

|

|

|

PRESENT ADDRESS (No. and street) |

|

|

|

|

|

|

|

City or Town |

|

State |

Zip Code |

|

|

|

|

|

YOUR FILING |

|

EXEMPTIONS — See Instruction 10 |

|

|

|

|

|

|

Exemption Amount |

|

||||||||||||

|

1. ☐ Single (If you can be claimed on another person’s tax return, use Filing Status 6) |

|

(A) Yourself ☐ |

Spouse ☐ |

|

|

Enter No. |

(A) |

|

× $2,400 |

$ ______________ |

|

|||||||||||

|

|

|

|

Checked |

|

|

|||||||||||||||||

|

2. ☐ Married filing joint return or spouse had no income |

|

Check here if you are: |

Spouse is: |

|

|

|

|

|

|

|

|

|

||||||||||

|

|

(B) ▶ ☐ ▶ ☐ |

▶ ☐ ▶ ☐ |

Enter No. |

(B) |

|

× $1,000 |

$ ______________ |

|

||||||||||||||

▶ 3. ☐ Married filing separately |

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

65 or over |

Blind |

65 or over |

Blind |

Checked |

|

|

|

|

|

|

||||||

|

4. ☐ Head of household |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

SPOUSE’S SOCIAL SECURITY NUMBER |

|

|

|

|

|

|

|

|

|

Enter |

|

|

|

× $2,400 |

$ ______________ |

|

||||||

|

|

|

(C) Dependent Children: |

|

|

(C) |

|

|

|||||||||||||||

|

5. ☐ Qualifying widow(er) with dependent child |

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

Name(s) |

|

|

|

|

|

|

Social Security number(s) |

|

|

|||||||||

|

6. ☐ Dependent taxpayer (Enter 0 in Exemption Box |

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

________________________________ __ __ |

|

||||||||||||||||||||

|

RESIDENCE |

|

|

|

|

________________________________ __ __ |

|

||||||||||||||||

|

Enter your state of legal residence. |

Were you a resident for the entire year of 2005? |

|

________________________________ __ __ |

|

||||||||||||||||||

_____________________________ |

Yes ☐ No ☐ |

If no, attach explanation. |

|

(D) Other Dependents: |

Enter |

|

|

Enter |

|

Enter |

(D) |

|

× $2,400 |

$ ______________ |

|

||||||||

|

|

|

|

|

|

|

|

|

No. |

|

|

No. |

|

Total |

|

|

|||||||

|

Are you or your spouse a member of the military? Yes ☐ |

No ☐ |

|

|

|

||||||||||||||||||

|

|

|

|

|

Regular |

65 or over |

|

|

|

|

|

|

|||||||||||

|

Did you file a Maryland income tax return for 2004? |

Yes ☐ |

No ☐ |

|

Name(s) and Relationship(s) |

|

|

Social Security number(s) |

|

|

|||||||||||||

|

|

________________________________ __ __ |

|

||||||||||||||||||||

|

If “Yes,” was it a ☐ Resident or a ☐ Nonresident return? |

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

________________________________ __ __ |

|

|||||||||||||||||

|

Advise dates you resided within Maryland for 2005. If none, enter “NONE.” |

|

|

||||||||||||||||||||

|

|

(E) Enter Total Exemptions |

|

|

▶ (E) |

|

|

Total |

|

|

|||||||||||||

|

FROM _____________________ |

TO _____________________ |

|

|

|

|

|

$ _____________ |

|

||||||||||||||

|

|

(Add A, B, C and D) |

|

|

|

|

|

|

Amount |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See Instruction 4 if you’re filing for Maryland taxes withheld in error. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

FEDERAL |

|

MARYLAND |

|

||||||||||||||||||

|

INCOME AND ADJUSTMENTS INFORMATION (See Instruction 11) |

|

INCOME (LOSS) |

|

INCOME (LOSS) |

INCOME (LOSS) |

|

||||||||||||||||

|

|

1. |

Wages, salaries, tips, etc |

|

1 |

|

|

|

|

. . |

|

|

|

||

|

|

2. |

Taxable interest income |

|

2 |

|

|

|

|

. . |

|

|

|

||

|

|

3. |

Dividend income |

|

3 |

|

|

|

|

. . |

|

|

|

||

|

|

4. |

Taxable refunds, credits or offsets of state and local income taxes . . . . |

|

4 |

|

|

|

|

. . |

|

|

|

||

wageyouroftop |

staple.ONE |

5. |

Alimony received |

|

5 |

|

|

|

|

. . |

|

|

|

||

|

|

6. |

Business income or (loss) |

|

6 |

|

|

|

|

. . |

|

|

|

||

|

|

7. |

Capital gain or (loss) |

|

7 |

|

|

|

|

. . |

|

|

|

||

|

|

8. |

Other gains or (losses) (from federal Form 4797) |

|

8 |

|

|

|

|

. . |

|

|

|

||

|

|

9. |

Taxable amount of pensions, IRA distributions, and annuities |

|

9 |

|

|

|

|

. . |

|

|

|

||

ORDERMONEYorCHECKyourPlaceon |

hereattachandstatementstaxandwith |

10. |

Rents, royalties, partnerships, estates, trusts, etc. (Circle appropriate item) |

|

10 |

|

|

. . |

|

|

|

||||

11. |

Farm income or (loss) |

|

11 |

|

|

||

. . |

|

|

|

||||

12. |

Unemployment compensation (insurance) |

|

12 |

|

|

||

|

|

. . |

|

|

|

||

|

|

13. |

Taxable amount of social security and tier 1 railroad retirement benefits |

|

13 |

|

|

|

|

. . |

|

|

|

||

|

|

14. |

Other income (including lottery or other gambling winnings) |

|

14 |

|

|

|

|

. . |

|

|

|

||

|

|

15. |

Total income (Add lines 1 through 14) |

|

15 |

|

|

|

|

. . |

|

|

|

||

|

|

16. |

Total adjustments to income from federal return (IRA, alimony, etc.) . . . . |

16 |

|

|

|

|

|

17. |

Adjusted gross income (Subtract line 16 from 15) |

▶ 17 |

|

|

|

|

|

|

|

|

|

||

|

|

ADDITIONS TO INCOME (See Instruction 12) |

|

|

Dollars |

Cents |

|

|

|

|

|

|

|

||

|

|

18. |

|

|

18 |

|

|

|

|

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

|

||

|

|

19. |

Other (Enter code letter(s) from Instruction 12) |

|

|

19 |

|

|

|

. . . |

. . . . . . . . . . . |

|

|

||

|

|

20. |

Total additions (Add lines 18 and 19) |

|

▶ |

20 |

|

|

|

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

|

||

|

|

21. |

Total federal adjusted gross income & Maryland additions (Add lines 17 (Column 1) and 20) |

21 |

|

||

|

|

SUBTRACTIONS FROM INCOME (See Instruction 13) |

|

|

|

|

|

|

|

|

22 |

22. |

|

|

|

|

|

|

23 |

23. |

Other (Enter code letter(s) from Instruction 13) |

|

|

|

|

▶ |

24 |

24. |

Total subtractions (Add lines 22 and 23) |

|

|

25. |

Maryland adjusted gross income (Subtract line 24 from line 21) |

|

25 |

DEDUCTION METHOD (All taxpayers must select one method and check the appropriate box)

☐ 26a

STANDARD DEDUCTION METHOD See Instruction 15 and worksheet. Enter amount on line 26a ▶

ITEMIZED DEDUCTION METHOD Complete lines 26b, c and d☐

26b

Total federal itemized deductions (from line 28 federal Schedule A) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

26c

State and local income taxes included in federal Schedule A, line 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

26d

Net itemized deductions (Subtract line 26c from line 26b) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

26. Deduction amount (Multiply lines 26a or 26d by the MD income factor) 26e. |

(from worksheet in Instruction 14 ) . . . |

▶ |

|

|

|

|

|

26

FORM |

MARYLAND NONRESIDENT |

||

505 |

|||

INCOME TAX RETURN |

|||

|

2005 |

|

|

|

|

Name ___________________________________________ SS# ____________________________________________ |

|

27. |

Net income (Subtract line 26 from line 25) |

||

28. |

Total exemption amount (from EXEMPTIONS area, page 1) See Instruction 10 |

||

29. |

Enter your Maryland income factor (from worksheet in Instruction 14) |

||

30. |

Maryland exemption allowance (Multiply line 28 by line 29) |

||

31. |

Taxable net income (Subtract line 30 from line 27) Figure tax on this amount |

||

MARYLAND TAX COMPUTATION

32a. Maryland tax (from Tax Table or Computation Worksheet) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

32b. Special nonresident tax. Multiply line 31 by .0125 (1.25%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

32c. Total Maryland tax. (Add lines 32a and 32b) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

▶

33. |

Earned income credit from worksheet in Instruction 20 |

. |

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||

34. |

Poverty level credit from worksheet in Instruction 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

|

|||

. |

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||||

35. |

Other income tax credits for individuals from Part G, line 8 of Form 502CR. (Attach Form 502CR) |

|

|

|

|

|

|

||||||||||||

36. |

Business tax credits (Attach Form 500CR) |

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

|

|||

. |

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||||

37. |

Total credits (Add lines 33 through 36) |

. |

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||

38. |

Maryland tax after credits (Subtract line 37 from line 32c) If less than 0, enter 0. . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

|

39. |

Contribution to Chesapeake Bay and Endangered Species Fund (See Instruction 21) |

|

|

|

|

|

|

|

|

|

|||||||||

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

||||||||||||

40. |

Contribution to Fair Campaign Financing Fund (See Instruction 21) |

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

|

||||

. |

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||||

41. |

Contribution to Maryland Cancer Fund (See Instruction 21) |

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

|

||||

. |

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||||

42. |

Total Maryland income tax and contributions (Add lines 38 through 41) |

|

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

|

43. |

Total Maryland tax withheld (Enter total from and attach your |

|

|

|

|||||||||||||||

|

. . |

|

|

||||||||||||||||

44. |

2005 estimated tax payments, amount applied from 2004 return and payment made with an extension request Form 502E |

|

|

|

|

▶ |

|

||||||||||||

|

. . |

|

|

||||||||||||||||

45. |

Refundable earned income credit from worksheet in Instruction 20 |

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

|

||||

. |

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||||

46. |

Nonresident tax paid by |

|

|

|

▶ |

|

|||||||||||||

|

|

||||||||||||||||||

47. |

Refundable income tax credits from Part H, line 5 of Form 502CR (Attach Form 502CR. See Instruction 22) |

|

. . |

|

|

||||||||||||||

48. |

Total payments and credits (Add lines 43 through 47) |

. |

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

|

49. |

Balance due (If line 42 is more than line 48, subtract line 48 from line 42) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

. |

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||||

50. |

Overpayment (If line 42 is less than line 48, subtract line 42 from line 48) |

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

|

||||

. |

. . . |

. . . . . |

. . . |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . |

|

|

|||||||||

51. |

Amount of overpayment TO BE APPLIED TO 2006 ESTIMATED TAX |

|

|

|

▶ |

51 |

|

|

|

|

|

|

|

|

|

||||

. |

. . . . |

. |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

52. |

Amount of overpayment TO BE REFUNDED TO YOU (Subtract line 51 from line 50) |

REFUND ▶ |

|

||||||||||||||||

|

|

|

|

|

|

||||||||||||||

53. |

Interest charges from Form 502UP |

|

|

or for late filing |

|

|

|

|

|

|

|

(See Instruction 23) Total |

|

|

▶ |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

54. |

TOTAL AMOUNT DUE (Add line 49 and line 53) |

IF $1 OR MORE, PAY IN FULL WITH THIS RETURN. |

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

For credit card payment check here |

|

|

and see Instruction 25. Direct debit is available only if you file electronically. |

|

|

|

|

|

|

||||||||||

DollarsCents

27

28

29

30

31

32a

32b

32c

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

52

53

54

DIRECT DEPOSIT OF REFUND (See Instruction 23) Please be sure the account information is correct.

55. To choose the direct deposit option, complete the following information: |

55a. Type of account: ▶ |

Checking

Savings

55b. Routing number ▶

55c. Account number ▶

-

-

-

-

Daytime telephone no. |

Home telephone no. |

CODE NUMBERS (3 digits per box) |

||

|

|

|||

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and |

Make checks payable to: COMPTROLLER OF MARYLAND. |

|||

statements and to the best of my knowledge and belief it is true, correct and complete. If prepared by a person |

It is recommended that you include your social security no. on |

|||

other than taxpayer, the declaration is based on all information of which the preparer has any knowledge. Check |

check using blue or black ink. Mail to: Comptroller of Maryland, |

|||

here |

|

if you authorize your preparer to discuss this return with us. |

Revenue Administration Division, Annapolis, Maryland |

|

|

|

|

|

|

Your signature |

Date |

▶

Preparer’s SSN or PTIN |

Signature of preparer other than taxpayer |

Spouse’s signature |

Date |

Address and telephone number of preparer

File Breakdown

| Fact Number | Fact Name | Detail |

|---|---|---|

| 1 | Form Purpose | The Maryland Form 505 is designed for nonresidents to file their state income tax return for the fiscal year beginning and ending in 2005. |

| 2 | Filing Status Options | The form includes various filing status options such as Single, Married filing jointly, Married filing separately, Head of household, Qualifying widow(er) with dependent child, and Dependent taxpayer. |

| 3 | Exemptions and Deductions | Taxpayers can claim exemptions for themselves, their spouse, dependents, and other qualified individuals, and select between standard or itemized deduction methods. |

| 4 | Income Reporting | Taxpayers are required to report various types of income including wages, interest, dividends, business income, and more, along with adjustments to income. |

| 5 | Governing Law | This form is governed by Maryland state law, specifically tailored for nonresidents who need to file a Maryland state income tax return. |

Steps to Filling Out Maryland 505

Once you have all the necessary documents and information to complete the Maryland 505 form for nonresident income tax return, follow these instructions to properly fill out the form. Make sure to report accurately and double-check your entries to avoid any processing delays or potential penalties.

- Enter your Social Security Number and, if filing jointly, your spouse's Social Security Number at the top of the form.

- Fill in your names, including first names, initials, and last names as requested.

- Provide your current address, including the street number, city or town, state, and ZIP code.

- Under "YOUR FILING STATUS," check the box that applies to you based on Instruction 4 within the form to determine your filing requirement.

- For the "EXEMPTIONS" section, see Instruction 10. Check the appropriate boxes that apply to your situation for yourself and your spouse, if applicable, and enter the number of dependents. Multiply the number of exemptions by the specified exemption amount and fill in the total exemption amount.

- In the "RESIDENCE INFORMATION" section, enter your state of legal residence and specify if you were a resident for the entire year. If not, attach an explanation as instructed.

- Under "FEDERAL MARYSWORLD IN-LINE," report your income and adjustments as per instructions. This includes wages, interest income, dividends, and other listed income types. Also include any business or farm income, unemployment compensation, and other specified income types.

- Follow the instructions in section "ADDITIONS TO INCOME" and "SUBTRACTIONS FROM INCOME," entering the appropriate amounts. Add or subtract these from your income as specified in the form.

- Choose your deduction method under "DEDUCTION METHOD" by checking the appropriate box for either standard deduction or itemized deduction. Fill in the amounts as instructed.

- Calculate your net income, Maryland tax, special nonresident tax, and total credits as per the form instructions, filling in each line accordingly.

- Under "MARYLAND TAX COMPUTATION," enter your calculated Maryland tax and nonresident tax, if applicable. Add the total Maryland tax to your total contributions if you chose to make any.

- Report total Maryland tax withheld, estimated tax payments, and any refundable credits in the payments section. Calculate any balance due or overpayment.

- For direct deposit of your refund, fill in your banking details, including the type of account, routing number, and account number.

- Review the sworn statement at the bottom of the form, sign and date the form along with your spouse if filing jointly.

- Attach any required documents, such as W-2 or 1099 forms if Maryland tax was withheld. Make sure all social security numbers and other sensitive information are accurately reported.

- Mail the completed form to the Comptroller of Maryland at the provided address. Include your payment if you owe tax, following the payment instructions on the form.

After submitting the form, your tax return will be processed. Allow appropriate time for processing, especially during peak filing seasons. If you're expecting a refund and have opted for direct deposit, monitor your bank account for the deposit. For balances due, ensure your payment is processed to avoid interest and penalties. If you've provided an email or phone contact, you may receive updates regarding the status of your filing.

More About Maryland 505

What is the purpose of the Maryland Form 505?

The Maryland Form 505 is designed for nonresidents who need to file income tax returns in Maryland. This form is used to report income earned by nonresidents from Maryland sources during the tax year. It ensures that individuals pay the correct amount of taxes on income earned within the state, even if they don't live in Maryland.

Who is required to file a Maryland Form 505?

Nonresidents who have earned income from Maryland sources are required to file Form 505. This includes individuals who live in another state or country but earn money from employment, property, or business activities in Maryland. It's essential to check the filing requirements outlined in Instruction 4 of the form to determine if you're required to file.

What information do I need to provide on Form 505?

Form 505 requires a variety of information, including:

- Personal information such as your Social Security Number and your spouse's, if married.

- Your filing status and exemptions.

- Detailed income information from both Maryland and non-Maryland sources.

- Adjustments to income, additions, and subtractions specific to Maryland.

- Your chosen deduction method (standard or itemized).

- Information about any Maryland tax credits you're claiming.

Can I claim deductions and credits on Form 505?

Yes, filers can claim deductions and credits on Form 505. You must decide whether to take the standard deduction or itemize deductions based on expenses that Maryland law allows. Additionally, several tax credits are available for nonresidents, such as the Earned Income Credit, Poverty Level Credit, and others specific to Maryland tax law. These can be found in the instructions and require proper documentation to claim.

How do I submit Form 505, and when is it due?

Form 505 can be submitted either electronically through Maryland's official tax website or by mail. To ensure timely processing, it's encouraged to file electronically. The due date for filing Form 505 aligns with the federal tax return deadline, typically April 15th of the year following the reported tax year. If the 15th falls on a weekend or holiday, the due date is the next business day.

What do I do if I owe taxes and can't pay by the deadline?

If you find yourself unable to pay the full amount of taxes owed by the deadline, it's important not to ignore the problem. Maryland offers options for taxpayers in this situation, including the possibility of setting up a payment plan. You should still file Form 505 by the deadline to avoid late filing penalties and contact the Comptroller of Maryland as soon as possible to discuss your payment options.

Common mistakes

When it comes to filling out the Maryland 505, the Nonresident Income Tax Return form, there are common mistakes that can lead to delays in processing or even result in an incorrect determination of tax liability. Being aware of these pitfalls can help individuals avoid unnecessary headaches and ensure their tax filing is accurate.

- Not verifying residency information: Individuals often mistake their residency status or fail to correctly report the periods they resided in or out of Maryland. This mistake can significantly impact tax calculations.

- Selecting the wrong filing status: The Maryland 505 form requires the filer to choose a filing status that matches their situation. Choosing the wrong status can lead to an incorrect tax computation.

- Incorrectly calculating exemptions: Exemptions reduce your taxable income, but they need to be calculated accurately. Misunderstanding which exemptions you’re eligible for, or miscalculating the exemption amount, is a common error.

- Failing to report all sources of income: Maryland requires reporting of various income types. Taxpayers sometimes omit parts of their income, such as dividends or interest income, which leads to an incomplete return.

- Omitting non-Maryland income: For nonresidents, accurately reporting income from non-Maryland sources is crucial. This income still influences the overall tax liability to Maryland, despite not originating from the state.

- Choosing the wrong deduction method: Taxpayers can choose between the standard deduction and itemizing deductions. The choice affects the tax owed, and selecting the inappropriate method for your situation can result in overpayment or underpayment of taxes.

- Miscalculating Maryland income factor: Nonresidents must apply the Maryland income factor to determine their tax liability based on the amount of income attributable to Maryland sources. Incorrect calculation of this factor can lead to an erroneous amount of tax owed.

Addressing these mistakes involves carefully reviewing the Maryland 505 instructions, verifying all information, and double-checking calculations. Doing so can help ensure the accuracy of the tax return and the proper determination of tax liability.

Documents used along the form

The Maryland Form 505, intended for nonresidents to file income tax returns for the state, serves as a crucial component of tax documentation. However, to complete the filing process accurately, additional forms and documents are often required to support or provide further details regarding an individual's tax situation. Understanding these supplementary documents helps ensure compliance with Maryland tax laws and aids in the efficient processing of nonresident income tax returns.

- Form 502CR - Tax Credits for Individuals: This form is used to claim various income tax credits that are available to Maryland taxpayers, including credits for taxes paid to other states, heritage structure rehabilitation, and child and dependent care expenses.

- Form 502E - Application for an Extension to File: This document allows taxpayers to request an extension of time to file their Maryland income tax return. It is important to note that this is an extension to file, not an extension to pay any taxes due.

- Schedule K-1 - Pass-Through Entity Income: This schedule reports income from partnerships, S corporations, or other pass-through entities. It is necessary for individuals who receive income from these sources to accurately report their Maryland state income.

- W-2 - Wage and Tax Statement: Employers issue this form to their employees, detailing the total wages paid and taxes withheld for the year. It is crucial for verifying income and tax withholding to the state of Maryland.

- 1099 Forms - Miscellaneous Income: These forms report various types of income other than wages, such as independent contractor income (1099-MISC), interest and dividends (1099-INT and 1099-DIV), and retirement distributions (1099-R), among others.

- Form 500CR - Business Tax Credits: This form is for claiming business-related tax credits. Although primarily utilized by businesses, individuals participating in business activities that qualify for certain credits may need to include this form with their return.

- Form 502 - Resident Income Tax Return: For nonresidents who need to file as part-year residents, this form may also be required to accurately report income earned while residing in Maryland.

- Form 505NR - Nonresident Income Tax Calculation: This form is a schedule that must be completed and attached to Form 505 to calculate the amount of Maryland income tax on nonresident income.

- Form 502UP - Underpayment of Estimated Maryland Income Tax: Individuals who did not pay enough tax through withholding or estimated tax payments must use this form to calculate any underpayment penalty.

- Form 502D - Declaration of Estimated Maryland Income Tax: For nonresidents who expect to owe $500 or more in Maryland income tax, this form allows them to make quarterly estimated tax payments.

These documents collectively form a comprehensive set of records that nonresident individuals may need when filing their Maryland Form 505. Each document serves a specific purpose, whether it's to claim a tax credit, report income from various sources, request additional time for filing, or make adjusted payments towards estimated taxes. A meticulous compilation and review of these forms is instrumental in the meticulous completion and submission of the Maryland income tax return for nonresidents.

Similar forms

The Maryland 505 form is similar to other state nonresident income tax returns in several key aspects, designed to calculate taxes owed to the state by individuals who earned income in the state but are not residents. Specific forms from other states share this purpose, each tailored to its respective state tax laws and regulations. While they all serve the same basic function, the details and specific requirements can vary significantly from one state to another.

California Form 540NR - This nonresident or part-year resident income tax return form is similar to the Maryland 505 form in its purpose of collecting state taxes from nonresidents who have earned income within the state's borders. Both forms require information about the taxpayer's income, both from within the state and from other sources, and they both allow for deductions and credits specific to the state's tax code. However, the California form may include different line items or calculations based on California's unique tax laws.

New York IT-203 Form - New York's nonresident and part-year resident income tax return form shares similarities with Maryland's 505 form in that it also serves nonresidents who must report income earned in New York. Both forms detail the income earned in the state, calculate the applicable taxes based on this income, and consider tax withholdings and estimated payments. Each form, however, is adapted to its own state’s regulations regarding income taxation and offers a set of instructions tailored to guide nonresidents through the filing process according to the specific tax rules of the state.

New Jersey NJ-1040NR Form - The New Jersey nonresident income tax return form is another example of a document similar to the Maryland 505 form, with both being designed to calculate and report state income taxes for individuals not residing within the state but who have earned income from sources within the state. The forms take into account various types of income, exemptions, and deductions specific to the state, aiming to accurately reflect the tax liability of nonresidents. Differences between the forms primarily stem from the individual tax policies and rates of Maryland and New Jersey.

Dos and Don'ts

Filling out the Maryland 505 form, a tax document for nonresidents, requires careful attention. This guide will highlight essential dos and don'ts to ensure a smooth process and avoid common pitfalls.

Dos:

- Double-check your Social Security Number (SSN) and your spouse’s SSN. Incorrect numbers can delay processing and may lead to issues with your tax return.

- Choose the correct filing status. Your filing status affects your tax rate and eligible deductions, so make sure to select the one that accurately represents your situation.

- Accurately report all income and adjustments. Ensure you include all sources of income, whether from Maryland, non-Maryland, or federal sources, and subtract any adjustments to income as permitted.

- Claim all eligible exemptions and deductions. Review the instructions carefully to ensure you are getting the exemptions and deductions for which you qualify.

- Fill in the residence information truthfully. This includes your state of legal residence and whether you were a resident for the whole year or part of the year.

- Use the correct tax computation. Apply the appropriate method to calculate your Maryland tax, ensuring you check whether you need to include special nonresident tax.

- Sign and date your return. An unsigned tax return is like an unsigned check – it’s not valid.

Don'ts:

- Don't neglect to attach all necessary documents. This can include W-2 forms, 1099 forms, schedules, and any other required documentation for credits or deductions claimed.

- Don't guess or estimate figures. Ensure all income, deductions, and credit amounts are accurate as per your financial documents.

- Don't overlook the Direct Deposit of Refund section if you expect a refund. Providing incorrect banking information can delay your refund significantly.

- Don't forget about Maryland-specific additions and subtractions to income. There are certain income modifications specific to Maryland tax law that may not apply on your federal return.

- Don't use ink colors other than blue or black when filling out the form. Other colors may not scan correctly, causing delays in processing.

- Don't send your return without reviewing it for errors. Even small mistakes can delay processing and impact your tax liability or refund.

- Don't miss the deadline for filing and payment. Late submission can result in penalties and interest charges.

Misconceptions

When navigating tax forms like the Maryland Form 505, a plethora of misconceptions can lead taxpayers astray. Here, we'll demystify ten common misunderstandings to ensure clarity and compliance.

- Form 505 is only for full-year nonresidents: This is incorrect. While primarily designed for nonresidents, Form 505 can also be relevant for part-year residents who need to report income earned during the period they were not residents of Maryland.

- Married individuals must file jointly on Form 505: This is misleading. Though many married couples choose to file jointly, Maryland law allows for married filing separately. Each option has its benefits and consequences, depending on the couple's specific financial situation.

- You cannot claim exemptions if you file as a dependent: This is partially true. While individuals claimed as dependants on another person's return cannot take personal exemptions, they might still be eligible for other types of exemptions or deductions.

- Military income is always taxed by Maryland if you're a resident: This is a simplification. The taxation of military income depends on several factors, including residency status and where the income was earned. Special rules may apply to military personnel and their spouses.

- Form 505 doesn't allow for itemized deductions: Contrary to this belief, taxpayers using Form 505 can choose between standard and itemized deductions, much like the federal tax return process. Itemizing can be beneficial if allowable expenses exceed the standard deduction amount.

- All income must be reported on Form 505, regardless of its source: While it's essential to accurately report income, not all types are subject to Maryland state tax. Understanding which income sources are taxable or exempt under Maryland law can significantly affect your return.

- Non-Maryland income is always taxable: This is misleading. Non-Maryland income may be taxable by Maryland for residents, but nonresidents typically only owe tax on income derived from Maryland sources.

- Filing Form 505 automatically subjects you to Maryland taxes: Filing this form does not necessarily mean you owe taxes to Maryland. It determines your tax liability, if any, based on numerous factors including your income, deductions, and credits.

- You can't get a refund if you're a nonresident filing Form 505: Incorrect. Nonresidents who have overpaid their taxes through withholding or estimated payments are eligible for refunds, similar to Maryland residents.

- Form 505 is too complicated for individuals to complete without professional help: While tax forms can seem daunting, Maryland provides robust instructions and resources to assist taxpayers. With careful reading and preparation, many individuals can accurately complete Form 505 without hiring a professional.

Understanding the ins and outs of Maryland Form 505 smooths the path to compliance, ensuring that taxpayers meet their obligations without overpaying. Shedding light on these misconceptions allows individuals to navigate their tax situations with greater confidence and precision.

Key takeaways

Filling out and properly using the Maryland 505 form, which is the income tax return form for nonresidents, involves various critical steps and considerations to ensure compliance and accuracy. Here are key takeaways to guide individuals through the process:

- Determine your filing status carefully. The form allows for different statuses, which can impact your tax obligations and potential deductions. Understanding each status and selecting the one that accurately represents your situation is vital.

- Accuracy in exemptions is crucial. The form outlines different types of exemptions, including for oneself, a spouse, dependents, and others. Accurately calculating and entering the number of exemptions is essential for determining your taxable income correctly.

- Residency information matters. For nonresidents, providing detailed residency information, including whether you have lived in Maryland for the entire year, is necessary. If not, attaching an explanation is required.

- Include all income sources. The form requires detailed listing of various income types, from wages to business income, ensuring that all income, whether from Maryland or not, is reported.

- Understand adjustments and deductions. The form allows for adjustments to income and offers a choice between standard and itemized deductions, impacting the income subject to tax.

- Choosing between standard and itemized deductions is a crucial decision that can affect your tax outcome. Review the instructions carefully to see which option benefits you more.

- Compute Maryland and non-Maryland income accurately to determine your taxable income properly. Differentiating between incomes is essential for nonresidents.

- Calculating your Maryland tax involves understanding specific rates and possibly a special nonresident tax, which requires correct application for accurate tax computation.

- Explore available credits. The form includes options for tax credits, such as the earned income credit or contributions to various funds, which can reduce tax liability.

- Payment and refund options. Taxpayers should carefully review their payment options, including direct deposit for refunds, to ensure proper processing.

- Handling overpayments and determining whether to apply them to future taxes or request a refund requires careful consideration to align with your financial planning.

- Finally, signing and dating the form is a declaration under penalties of perjury that the information provided is accurate to the best of your knowledge. A preparer, if used, must also sign and provide their information.

Understanding these key elements can help individuals navigate the complexities of the Maryland 505 form, ensuring compliance and the potential for a favorable tax outcome. Being thorough and careful in completing the form is essential for all nonresidents who have earned income from Maryland sources.

Common PDF Templates

How Much Back Child Support Is a Felony in Maryland - Designed for use in either the Circuit Court or District Court of Maryland, tailored to address violations of court orders.

What Is a Certificate of Compliance Maryland - This form is specific to Maryland and adheres to the Labor & Employment Article §9-206 of the Annotated Code of Maryland, highlighting state-specific compliance.

Motion to Quash Warrant Form Maryland - Designed to meet the information needs of the Maryland Department of Assessments and Taxation (SDAT) and local finance offices.