Maryland 505Nr PDF Template

The Maryland 505Nr form, designed for nonresident income tax calculation for the year 2013, is an essential document for individuals who have earned income in Maryland but do not reside within the state. This form requires the filer to attach it to their tax return, ensuring that income earned within Maryland by nonresidents is reported accurately and taxed correctly. It guides filers through a detailed calculation process, beginning with the taxable net income and concluding with the Maryland tax owed, after adjustments and deductions. Part I of the form focuses on calculating tax without certain modifications, asking for taxable net income figures from associated forms and the tax amount based on provided schedules or tables. In Part II, filers calculate their Maryland tax, taking into account federal adjusted gross income, additions, subtractions, and specific non-Maryland income, which leads to the determination of Maryland adjusted gross income and eventually the Maryland tax due. Filers are instructed on how to adjust their standard or itemized deductions based on calculated income factors. Additionally, the form includes provisions for special nonresident tax rates and instructions for nonresidents employed in Maryland who are subject to local taxes. It is meticulously designed to ensure nonresidents comply with Maryland's tax laws, highlighting the complex nature of state tax regulations and the importance of accurate tax filing.

Maryland 505Nr Sample

|

|

MARYLAND |

NONRESIDENT INCOME |

2013 |

||

|

|

FORM |

||||

|

|

TAX CALCULATION |

|

|||

|

|

505NR |

|

|||

|

|

ATTACH TO YOUR TAX RETURN |

|

|||

|

|

|

|

|

|

|

Only |

|

Social Security Number |

|

|

Spouse's Social Security Number |

|

|

|

|

|

|

|

|

PrintUsing Blackor Ink |

|

|

|

|

|

|

|

Spouse’s first name |

|

Initial |

Last name |

|

|

|

|

Your first name |

|

Initial |

Last name |

|

Blue |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

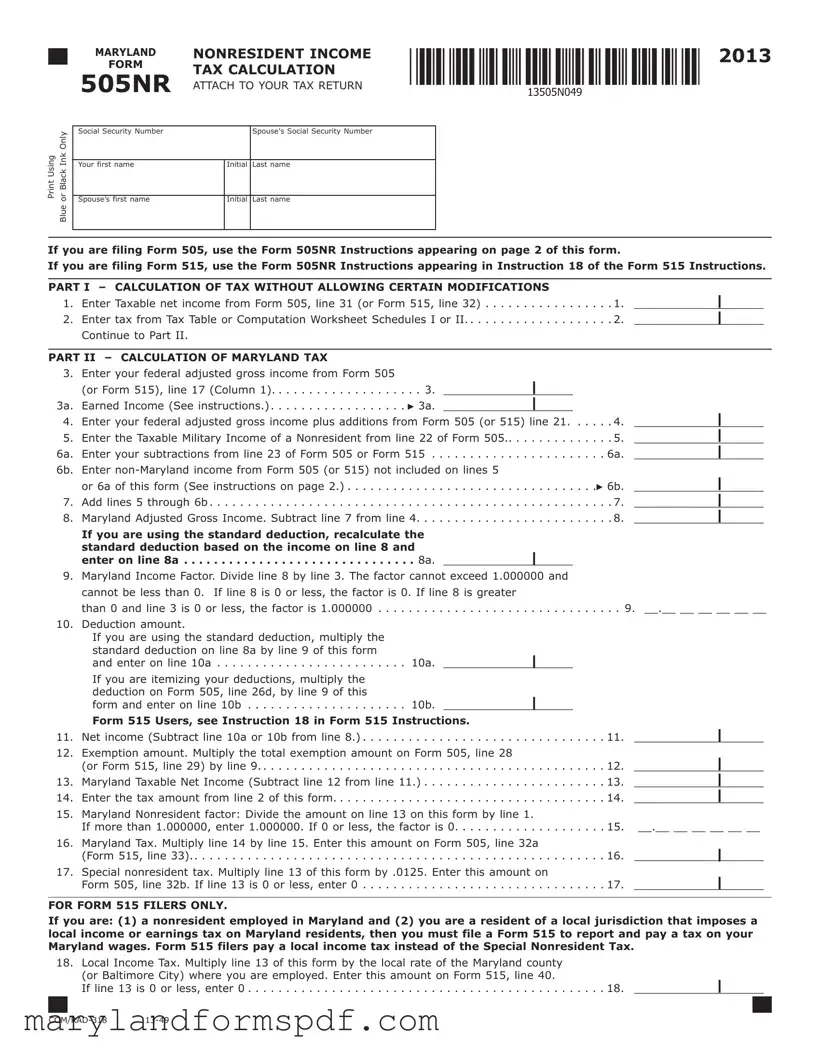

If you are filing Form 505, use the Form 505NR Instructions appearing on page 2 of this form.

If you are filing Form 515, use the Form 505NR Instructions appearing in Instruction 18 of the Form 515 Instructions.

PART I – CALCULATION OF TAX WITHOUT ALLOWING CERTAIN MODIFICATIONS |

|

||||

1. |

Enter Taxable net income from Form 505, line 31 (or Form 515, line 32) |

. . . . . . . . . . .1. |

| |

||

2. |

Enter tax from Tax Table or Computation Worksheet Schedules I or II |

. . . . . . . . . . . 2. |

| |

||

|

Continue to Part II. |

|

|

|

|

|

|

|

|

|

|

PART II – CALCULATION OF MARYLAND TAX |

|

|

|

|

|

3. |

Enter your federal adjusted gross income from Form 505 |

|

|

|

|

|

(or Form 515), line 17 (Column 1) |

3. |

|

| |

|

|

___________________ |

|

|||

3a. |

Earned Income (See instructions.) |

3a. |

|

| |

|

___________________ |

|

||||

4. |

Enter your federal adjusted gross income plus additions from Form 505 (or 515) line 21. . . . . .4. |

| |

|||

___________________ |

|||||

5. |

Enter the Taxable Military Income of a Nonresident from line 22 of Form 505.. . . . . . . . . . . . . .5. |

| |

|||

___________________ |

|||||

6a. |

Enter your subtractions from line 23 of Form 505 or Form 515 |

|

. . . . . . . . . . 6a. |

| |

|

. . . . . . . . . . . |

___________________ |

||||

6b. |

Enter |

|

|

||

|

or 6a of this form (See instructions on page 2.) |

|

. . . . . . . . . 6b. |

| |

|

|

. . . . . . . . . . . |

___________________ |

|||

7. |

Add lines 5 through 6b |

|

. . . . . . . . . . .7. |

| |

|

. . . . . . . . . . . |

___________________ |

||||

8. |

Maryland Adjusted Gross Income. Subtract line 7 from line 4 |

|

|

. . . . . . . . . . .8. |

| |

. . . . . . . . . . . |

___________________ |

||||

|

If you are using the standard deduction, recalculate the |

|

|

|

|

|

standard deduction based on the income on line 8 and |

|

|

| |

|

|

enter on line 8a |

8a. |

|

|

|

9.Maryland Income Factor. Divide line 8 by line 3. The factor cannot exceed 1.000000 and cannot be less than 0. If line 8 is 0 or less, the factor is 0. If line 8 is greater

than 0 and line 3 is 0 or less, the factor is 1.000000 . . . . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . 9. __.__ __ __ __ __ __ |

10. Deduction amount. |

|

|

If you are using the standard deduction, multiply the |

|

|

standard deduction on line 8a by line 9 of this form |

___________________ |

| |

and enter on line 10a |

10a. |

|

If you are itemizing your deductions, multiply the |

|

|

deduction on Form 505, line 26d, by line 9 of this |

___________________ |

| |

form and enter on line 10b |

10b. |

|

Form 515 Users, see Instruction 18 in Form 515 Instructions. |

|

|

11. |

Net income (Subtract line 10a or 10b from line 8.) |

11. |

___________________| |

12. |

Exemption amount. Multiply the total exemption amount on Form 505, line 28 |

|

| |

|

(or Form 515, line 29) by line 9 |

12. |

|

|

___________________ |

||

13. |

Maryland Taxable Net Income (Subtract line 12 from line 11.) |

13. |

| |

___________________ |

|||

14. |

Enter the tax amount from line 2 of this form |

14. |

| |

___________________ |

|||

15. |

Maryland Nonresident factor: Divide the amount on line 13 on this form by line 1. |

|

|

|

If more than 1.000000, enter 1.000000. If 0 or less, the factor is 0 |

15. |

__.__ __ __ __ __ __ |

16. |

Maryland Tax. Multiply line 14 by line 15. Enter this amount on Form 505, line 32a |

|

___________________| |

|

(Form 515, line 33) |

16. |

|

17. |

Special nonresident tax. Multiply line 13 of this form by .0125. Enter this amount on |

|

___________________| |

|

Form 505, line 32b. If line 13 is 0 or less, enter 0 |

17. |

FOR FORM 515 FILERS ONLY.

If you are: (1) a nonresident employed in Maryland and (2) you are a resident of a local jurisdiction that imposes a local income or earnings tax on Maryland residents, then you must file a Form 515 to report and pay a tax on your Maryland wages. Form 515 filers pay a local income tax instead of the Special Nonresident Tax.

18. Local Income Tax. Multiply line 13 of this form by the local rate of the Maryland county (or Baltimore City) where you are employed. Enter this amount on Form 515, line 40.

If line 13 is 0 or less, enter 0 |

| |

|

18. ___________________ |

||

|

|

|

MARYLAND |

NONRESIDENT INCOME |

|

FORM |

TAX CALCULATION |

|

505NR |

||

INSTRUCTIONS |

||

2013 |

|

Using Form 505NR, Nonresident Income Tax Calculation, follow the

Line 1. Enter the taxable net income from Form 505, line 31.

Line 2. Find the income range in the tax table that applies to the amount on line 1 of Form 505NR. Find the Maryland tax corresponding to your income range. Enter the tax amount from the tax table. If your taxable income on line 1 is $50,000 or more, use the Maryland Tax Computation Worksheet schedules at the end of the tax table.

Line 3. Enter your federal adjusted gross income (FAGI) from Form 505, line 17 (column 1).

Line 3a. If you are claiming a federal earned income credit (EIC), enter the earned income you used to calculate your federal EIC.

Earned income includes wages, salaries, tips, professional fees and other compensation received for personal services you performed. It also includes any amount received as a scholarship that you must include in your federal AGI.

Line 4. Enter the amount from Form 505, line 21.

Line 5. Taxable Military Income of a nonresident, if applicable.

Line 6a. Enter the amount of your subtractions from line 23 of Form 505.

Line 6b. Enter any

Important Note: Make sure that you follow the instruction for line 6b above to arrive at the correct amount. The

Be sure to include the following items if not already included on line 5 or 6a.

•Maryland salaries and wages should be included if you are a resident of a reciprocal state.

•Income subject to tax as a resident when required to file both Forms 502 and 505 should be included.

•Line 17 of column 3 on Form 505 (or 515) should also include income for wages earned in Maryland by a nonresident rendering police, fire, rescue or emergency services in an area covered under a state of emergency declared by the Maryland Governor, if the wages are paid by a nonprofit organization not registered to do business in the state and not otherwise doing business in the state, or by a state, county or political subdivision of a state, other than the State of Maryland.

PAGE 2

Line 7. Add lines 5 through 6b.

Line 8. Subtract line 7 from line 4. This is your Maryland Adjusted Gross Income.

Line 8a. If you are using the standard deduction amount, recalculate the standard deduction (line 8) based on the Maryland adjusted gross income.

Line 9. Compute your Maryland income factor by dividing line 8 by line 3. Carry the factor to six decimal places. The factor cannot exceed 1.000000 and cannot be less than 0. If line 8 is 0 or less, the factor is 0. If line 8 is greater than 0 and line 3 is 0 or less, the factor is 1.000000.

Line 10a. If you are using the standard deduction, multiply the standard deduction on line 8a by the Maryland Income Factor (line 9) and enter on line 10a.

Line 10b. If you are itemizing your deductions, multiply the deduction on Form 505 line 26d by the Maryland Income Factor (line 9) and enter on line 10b.

Line 11. If you are using the standard deduction, subtract line 10a from line 8. If you are using itemized deductions, subtract line 10b from line 8.

Line 12. Multiply the total exemption amount |

on |

Form |

|

|

505, line 28 by the factor on line 9. |

|

|

Line 13. Subtract line 12 from line 11. This |

is |

your |

|

|

Maryland taxable net income. |

|

|

Line 14. |

Enter the tax from line 2 of this form. |

|

|

Line 15. |

Divide the amount on line 13 of this form by the |

||

|

amount on line 1. Carry this Maryland nonresident |

||

|

factor to six decimal places. If more than |

||

|

1.000000, enter 1.000000. If 0 or less, enter 0. |

||

Line 16. |

Multiply line 14 by line 15 to arrive at your |

||

|

Maryland tax. Enter this amount on line 16 and |

||

|

on Form 505, line 32a. |

|

|

Line 17. |

Multiply line 13 by .0125. Enter this amount on |

||

|

line 17 and on Form 505, line 32b. If line 13 is |

||

|

0 or less, enter 0. |

|

|

On Form 505, add lines 32a and 32b and enter the total on line 32c.

Note: If you are using Form 505NR with Form 505, follow the instructions above. If you are using Form 505NR with

Form 515, please follow Instruction 18 in the Form 515 instructions.

File Breakdown

| Fact Name | Detail |

|---|---|

| Purpose | The Maryland Form 505NR is specifically designed for calculating nonresident income tax. |

| Applicable Forms | Form 505NR must be attached to either Form 505 or Form 515, depending on the filer's circumstances. |

| Special Tax Instructions | Nonresidents employed in Maryland and residents of jurisdictions imposing a local income tax on Maryland residents must file Form 515 and calculate local income tax instead of the special nonresident tax. |

| Governing Law | This form is governed by Maryland Tax-General Article, which outlines state tax responsibilities for residents and nonresidents. |

Steps to Filling Out Maryland 505Nr

Filling out the Maryland 505NR form is necessary for nonresidents who need to calculate their state income tax. This step-by-step guide simplifies the process, ensuring accuracy and compliance with Maryland state tax requirements. The form is divided into two parts: the calculation of tax without allowing certain modifications and the calculation of Maryland tax. It's important to follow the instructions closely to correctly determine your tax liability.

- Begin by entering your taxable net income from Form 505, line 31 (or Form 515, line 32), on line 1 of the 505NR form.

- Refer to the tax table or Computation Worksheet Schedules I or II to find your applicable tax based on the income entered in step 1. Enter this tax amount on line 2.

- On line 3, enter your federal adjusted gross income from Form 505 (or Form 515), as shown on line 17 (Column 1).

- For line 3a, if claiming a federal earned income credit (EIC), enter the earned income used for the federal EIC calculation.

- Enter the sum of your federal adjusted gross income plus all additions from Form 505 (or 515), line 21, on line 4.

- If applicable, enter the taxable military income of a nonresident from line 22 of Form 505 on line 5.

- Subtract your allowed subtractions from line 23 of Form 505 or Form 515 and enter this on line 6a.

- For line 6b, enter any non-Maryland income not previously included on lines 5 or 6a, as specified in the instructions.

- Add the amounts from lines 5 through 6b and enter the total on line 7.

- Calculate your Maryland Adjusted Gross Income by subtracting line 7 from line 4 and record on line 8.

- If using the standard deduction, recalculate based on the income on line 8 and enter on line 8a.

- Compute the Maryland Income Factor on line 9 by dividing line 8 by line 3, adhering to the constraints outlined in the instructions.

- If using the standard deduction, multiply the recalculated amount on line 8a by the Maryland Income Factor from line 9 and enter on line 10a. If itemizing deductions, multiply the deduction from Form 505, line 26d, by the factor from line 9 and enter on line 10b.

- Subtract line 10a or 10b from line 8 to find your net income and enter on line 11.

- Multiply the total exemption amount from Form 505, line 28 (or Form 515, line 29) by the Maryland Income Factor from line 9 and enter on line 12.

- Subtract line 12 from line 11 to determine your Maryland Taxable Net Income and enter this amount on line 13.

- Transfer the tax amount from line 2 of this form to line 14.

- Divide the amount on line 13 by the taxable net income entered in step 1 to calculate the Maryland Nonresident factor and enter on line 15.

- Multiply line 14 by the factor on line 15 to find your Maryland tax. Record this amount on line 16 and Form 505, line 32a (or Form 515, line 33).

- Multiply line 13 by .0125 to calculate the Special Nonresident Tax and enter this on line 17 and Form 505, line 32b.

- For Form 515 filers, compute the Local Income Tax by multiplying line 13 by the local rate of your Maryland employment area and enter on Form 515, line 40.

After completing these steps, double-check your calculations for accuracy. Missteps can result in errors in tax liabilities. If using Form 505NR with Form 505, ensure all the relevant sections are filled accurately. Form 515 filers should also refer to Instruction 18 in the Form 515 instructions to correctly complete the form. Upon finalizing, attach the 505NR form to your tax return for submission. Taking time to accurately complete the form can help avoid any potential issues with your tax filing.

More About Maryland 505Nr

What is the Maryland 505NR form?

The Maryland 505NR form is a tax document specifically designed for nonresidents to calculate their Maryland income tax. It is used in conjunction with Form 505 or Form 515, depending on the taxpayer's circumstances. This form helps to adjust a nonresident's taxable income based on Maryland sources and calculates the appropriate amount of tax owed to the state.

Who needs to fill out the Maryland 505NR form?

This form must be completed by nonresidents who earn income from Maryland sources and are required to file a Maryland income tax return (Form 505 or Form 515). It is particularly relevant for individuals who are not residents of Maryland but have earned income in the state, such as from employment or property ownership.

How do I determine my Maryland taxable net income using the 505NR form?

To determine your Maryland taxable net income using the 505NR form, follow these steps:

- Enter your taxable net income from Form 505, line 31 (or Form 515, line 32).

- Add any necessary subtractions and deductions as outlined in the form instructions.

- Adjust your income by applying the Maryland nonresident factor, which takes into account the portion of your income attributable to Maryland sources.

This process align hands your Maryland adjusted gross income, from which you can then subtract deductions and exemptions to find your Maryland taxable net income.

What are the specific modifications that must be made for nonresidents on the 505NR form?

Nonresidents must make specific adjustments to their income on the 505NR form, including:

- Subtracting income that is not sourced to Maryland.

- Adding back deductions and exemptions proportionally reduced by the Maryland income factor—a fraction that represents the portion of federal adjusted gross income derived from Maryland sources.

- Calculating a special nonresident tax, if applicable.

Can I file the Maryland 505NR form electronically?

Yes, taxpayers can file the Maryland 505NR form electronically as part of their Maryland nonresident income tax return. Electronic filing is encouraged as it is faster and reduces the risk of errors. Taxpayers can use authorized e-file providers or Maryland's official tax website to file their returns electronically.

What should I do if I made a mistake on my filed 505NR form?

If you discover an error on your filed 505NR form, you should amend your return as soon as possible. This involves completing an amended Maryland income tax return for nonresidents and including a corrected 505NR form. Be sure to explain the changes and provide any necessary documentation. Filing an amended return will help avoid penalties and ensure your tax obligations are correctly met.

Common mistakes

Completing the Maryland 505NR form, used for nonresident income tax calculation, can be complex. Here are eight common mistakes to avoid:

- Incorrect income reporting:

People often misreport their taxable net income by either entering the wrong amount from Form 505, line 31, or Form 515, line 32. It's crucial to double-check these numbers for accuracy.

- Failing to properly calculate tax:

Not using the tax table or the Computation Worksheet Schedules I or II correctly for line 2 can result in incorrect tax calculations.

- Overlooking federal adjusted gross income adjustments:

Forgetting to enter your federal adjusted gross income from Form 505 or 515, line 17, accurately impacts the entire calculation process negatively.

- Misinterpreting earned income:

On line 3a, claimants sometimes misunderstand what constitutes earned income for the federal EIC, leading to discrepancies.

- Incorrect addition and subtraction of income:

Errors in adding amounts from Form 505 or 515, line 21, and not properly including or excluding the right types of income or subtractions in lines 5 through 6b, affect the accuracy of Maryland Adjusted Gross Income (MAGI).

- Miscalculating deductions:

Both standard and itemized deductions calculations often encounter errors, especially when multiplying by Maryland Income Factor on line 9, affecting lines 10a or 10b.

- Failing to correctly apply exemptions:

Exemptions on line 12 must be multiplied by the Maryland Income Factor from line 9. A mistake here can skew the Maryland Taxable Net Income and, subsequently, the amount of tax owed.

- Special nonresident tax and local income tax calculation errors:

Special nonresident tax (line 17) and the local income tax for Form 515 filers (line 18) are sometimes calculated without considering the instructions properly, leading to incorrect entries.

Avoiding these mistakes can help ensure the accurate and prompt processing of Maryland nonresident income tax filings.

Documents used along the form

When individuals process their Maryland Nonresident Income Tax using Form 505NR, they often need to complement this document with other forms and documents to accurately calculate and report their taxes. Here is a detailed look at some of these essential companion documents.

- Form 505: The Maryland Nonresident Income Tax Return itself. This form is paramount as it is where individuals report their income, calculate their tax liability, and claim any deductions or credits they are eligible for.

- Form 515: For nonresidents employed in Maryland who reside in jurisdictions that impose a local income tax on Maryland residents. It is used to report and pay tax on Maryland wages. This form is specifically for those who must report local income tax instead of the special nonresident tax.

- Schedule I: Used to calculate Maryland tax adjustments. This schedule helps nonresidents adjust their federal adjusted gross income to reflect specific income sources or tax deductions relevant only to Maryland.

- Schedule II: Similar to Schedule I, this is used for additional tax calculations that might not be captured on the primary form or the first schedule, providing a more comprehensive tax profile.

- Form MW507: Employee's Maryland Withholding Exemption Certificate is critical for Maryland nonresidents working in Maryland as it determines the amount of state income tax to withhold from their pay.

- Form 502: Resident Income Tax Return. For individuals who need to file taxes both as a resident (possibly for part of the year) and as a nonresident, this form is relevant for the portion of the year they were considered Maryland residents.

- Form 500: Corporate Income Tax Return. This is applicable for nonresidents who own businesses in Maryland, as it reports the income, deductions, and credits of a corporation.

- Form 1099: Various types of Form 1099 may be necessary to accompany the 505NR, such as Form 1099-INT for interest earned or 1099-DIV for dividends, to report income from sources other than wages.

- W-2: Wage and Tax Statement. Nonresidents who earn salary or wages in Maryland will need this form to document their earnings and state and federal taxes withheld by their employer.

In conjunction with the Maryland 505NR form, these documents provide a comprehensive overview of an individual's tax scenario, ensuring all income is reported and taxed correctly. Understanding and preparing these forms accurately can help nonresidents comply with Maryland's tax laws and potentially optimize their tax situations.

Similar forms

The Maryland 505Nr form is similar to other state-specific nonresident tax forms which are designed to calculate income tax for individuals who earn income in a state where they do not reside. These forms typically require the income earner to provide details on their total earned income within the state, their full-year income from all sources, and any state-specific adjustments to income. The goal is to accurately assess the amount of tax owed to the state by individuals who are not permanent residents but who have generated income within the state's borders.

One such document that shares similarities with the Maryland 505Nr form is the California Form 540NR, which caters to nonresidents or part-year residents who have earned income in California. Like the Maryland 505Nr, the California 540NR requires individuals to report income earned within the state and apply state-specific adjustments to determine the tax owed. Both forms distinguish between residents and nonresidents, adjust gross income based on state-specific rules, and calculate taxes owed in a similar step-by-step process. However, while Maryland 505Nr is specific to Maryland's tax codes and rates, California 540NR applies California's tax laws and calculations.

Similarly, the New York IT-203 form is designed for nonresidents and part-year residents earning income in New York State. Like the Maryland 505Nr form, the IT-203 form requires taxpayers to report their New York State income and calculate their tax based on specific rules for nonresidents. Both forms include calculations to modify the federal adjusted gross income (FAGI) to fit state-specific tax codes, require adjustments for specific types of income or deductions unique to the state, and lead to the calculation of state income tax owed by nonresidents. Though they serve the same purpose for different states, the structure and specific instructions reflect the unique tax laws of Maryland and New York, respectively.

Dos and Don'ts

When filling out the Maryland 505NR form, it's crucial to stay well-informed to ensure accuracy and compliance. Here are some guidelines to help you through the process:

Do:

- Use black or blue ink as instructed on the form to ensure that all information is legible and can be correctly scanned.

- Read the instructions carefully for either Form 505 or Form 515, depending on which one you are using, to avoid any mistakes.

- Enter your taxable net income accurately by referring to the correct line from Form 505 or Form 515.

- Check the tax table or Computation Worksheet Schedules I or II to find the correct tax rate that applies to you.

- Calculate your Maryland Adjusted Gross Income (MAGI) with utmost care by subtracting the relevant non-Maryland income and adjustments.

- Accurately compute your Maryland Income Factor to ensure you are not overpaying or underpaying your due tax.

- Recalculate your standard deduction based on your Maryland Adjusted Gross Income if you choose not to itemize deductions.

- Itemize deductions if it benefits you more than taking the standard deduction—make sure to calculate it based on the Maryland Income Factor.

- Report any special nonresident tax or local income tax accurately, especially if you are filing Form 515.

- Double-check every entry for completeness and accuracy before attaching the form to your tax return.

Don't:

- Don't rush through the instructions; each line has specific directives that must be followed correctly.

- Don't use pens with colors other than black or blue, as this can result in scanning errors.

- Don't overlook the specific income and deduction lines that apply to nonresidents; Maryland law provides for specific calculations for nonresidents.

- Don't forget to include all sources of income, including non-Maryland income, ensuring that it is accurately reflected and adjusted.

- Don't estimate figures. Ensure all numbers are exact to avoid issues with the tax authorities.

- Don't ignore the Maryland Income Factor calculation—it's crucial for determining the correct amount of tax owed by nonresidents.

- Don't choose the wrong deduction method without calculating which one (itemized or standard) benefits you the most.

- Don't skip any sections that apply to you; even if some sections seem not to apply, review them carefully to ensure nothing is missed.

- Don't miss out on specifics for Form 515 filers, especially related to local income tax if employed in Maryland.

- Don't submit the form without reviewing it thoroughly for mistakes that could lead to unnecessary delays or audits.

Misconceptions

Understanding the Maryland Form 505NR can sometimes be complex due to misconceptions about its purpose and how it should be filled out. Below are eight common misconceptions explained to provide clarity:

- It's only for residents. This is incorrect. Form 505NR is specifically designed for nonresidents who need to calculate their Maryland state tax on income earned within Maryland. It should be attached to either Form 505 or Form 515 as applicable.

- You must fill it out even if you don't have Maryland income. This is not true. Form 505NR is required only if you are a nonresident with Maryland-sourced income. Without such income, this form is not necessary for your tax filings in Maryland.

- It can be used by itself for tax filing. This is a misconception. Form 505NR must be attached to Form 505 or Form 515, depending on the nonresident's situation. It is not a standalone tax form and is part of a complete tax filing for nonresidents.

- The instructions are the same for Form 505 and Form 515 filers. Actually, while Form 505NR is used in conjunction with both forms, the instructions specify that certain lines and calculations differ depending on whether it's being attached to Form 505 or Form 515. Specific instructions for Form 515 filers are found in Instruction 18 of the Form 515 instructions.

- All income must be reported on Form 505NR. This statement is incorrect. Only certain types of income, deductions, and modifications applicable to Maryland nonresidents should be reported on Form 505NR. This includes Maryland-sourced income and specific subtractions and additions related to that income.

- Federal Adjusted Gross Income (FAGI) is irrelevant to this form. In fact, FAGIs are vital for filling out Form 505NR. It forms the basis for several calculations on the form, including the Maryland Income Factor and adjustments to income.

- No differentiation is made between types of income. This is not accurate. Form 505NR requires nonresidents to separate and specify types of income, such as military income or specific non-Maryland income, for accurate tax calculation.

- There's no provision for standard or itemized deductions. On the contrary, Form 505NR accommodates both standard and itemized deductions. Deductions are adjusted based on the Maryland Income Factor, which is calculated within the form, ensuring that nonresidents only take deductions proportional to their Maryland source income.

Correct understanding and filling out of Form 505NR ensure that nonresidents correctly calculate their Maryland state tax, helping to avoid common errors and misunderstandings in the process.

Key takeaways

Filling out and using the Maryland 505NR form is crucial for nonresidents who have income sourced from Maryland. Here are some key takeaways to ensure accurate completion and use of this form:

- Determine eligibility: The Maryland 505NR form is specifically designed for nonresidents. It must be attached to either Form 505 or Form 515, depending on your circumstances.

- Understand the purpose: This form calculates the amount of Maryland state tax due, factoring in specific adjustments for nonresidents.

- Accurately report income: Start by entering your taxable net income from Form 505 or Form 515. This figure is fundamental to calculating your Maryland tax.

- Consider all sources of income: Include all relevant forms of income, such as wages, salaries, and any applicable non-Maryland income.

- Subtract eligible deductions: The form allows for certain deductions and exemptions, which can reduce your taxable income. Be sure to accurately calculate and apply these.

- Calculate your Maryland Adjusted Gross Income (MAGI): Subtract your eligible deductions from your total income to find your MAGI, as this determines your tax liability.

- Understand the Maryland Income Factor: This factor adjusts your deductions based on the ratio of your Maryland income to your total income, ensuring nonresidents only pay tax on their Maryland-sourced income.

- Calculate your Maryland Tax: Use the Maryland nonresident factor to determine the portion of tax owed based on your Maryland-sourced income.

- Special considerations for certain filers: If you are a nonresident employed in Maryland but reside in a jurisdiction with a local tax, you may need to file Form 515 and pay a local income tax instead of the Special Nonresident Tax.

Proper completion and understanding of the Maryland 505NR form ensure that you comply with Maryland tax laws and only pay tax on income earned within the state. This careful approach helps avoid penalties and ensures that your tax liabilities are correctly calculated.

Common PDF Templates

Maryland State Sales Tax - This legal instrument encourages open and honest transactions between businesses and suppliers within Maryland's economic framework.

University of Maryland Admission Requirements - Highlighting non-discriminatory practices, the form aligns with broader health and civil rights laws to protect applicants.