Maryland 505X PDF Template

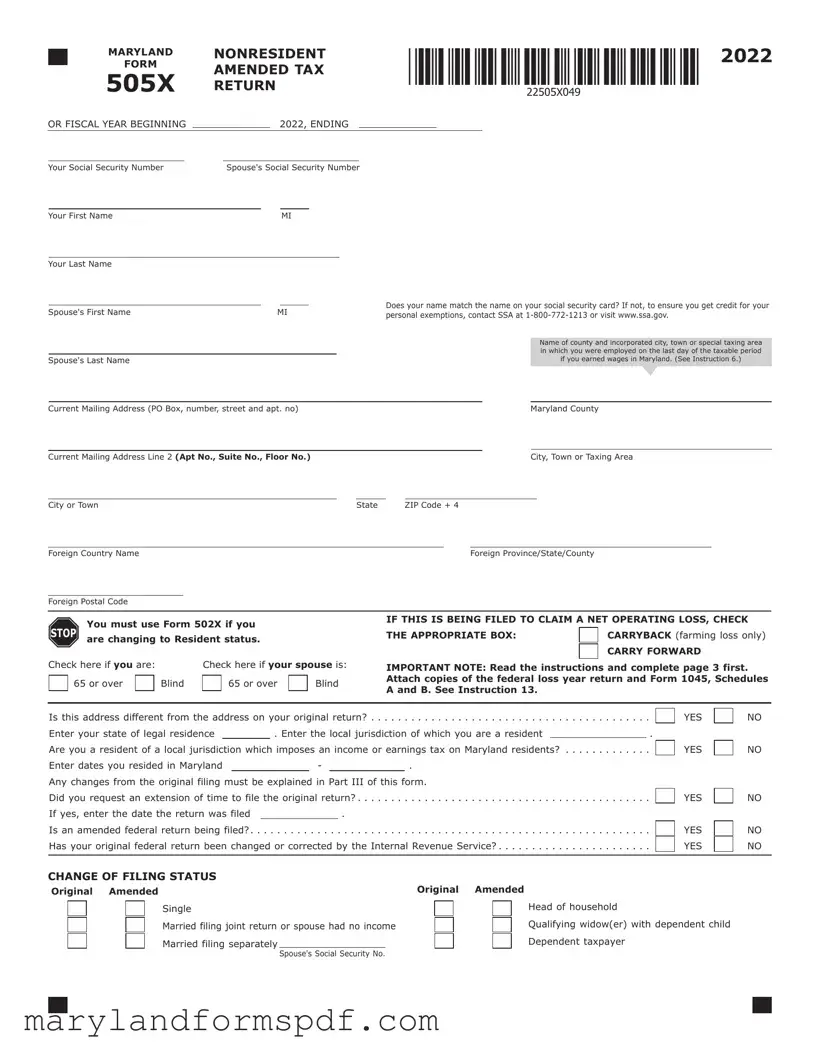

In Maryland, nonresidents who have had a change in their income, deductions, or credits, or who need to correct information on their originally filed tax return must use the Maryland Form 505X, the Amended Nonresident Tax Return. This form is crucial for those seeking to make adjustments for the tax year 2021 or for other fiscal years beginning in 2021. It covers a broad range of financial information, including wages earned, interest income, dividends, adjustments to income, and specifics about itemized or standard deductions, among others. The form also delves into details about exemptions, modifications in filing status, and any refund or balance due in light of these amendments. Taxpayers are prompted to thoroughly review and provide an explanation for each change, ensuring accuracy and compliance with Maryland tax laws. Additionally, it encompasses personal details such as name changes and residency status, ensuring credits and taxes are properly allocated. For those claiming net operating losses, the form provides options to carryback (specifically for farming losses) or carry forward the loss, with specific documentation requirements. The Form 505X serves as an essential tool for nonresidents to rectify their tax obligations in Maryland, hence guaranteeing tax fairness and accuracy for all parties involved.

Maryland 505X Sample

|

MARYLAND |

NONRESIDENT |

|

|

|

|

|

|

2022 |

||||||||||||||||||||

|

FORM |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

AMENDED TAX |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

505X |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

RETURN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

OR FISCAL YEAR BEGINNING |

|

|

|

|

|

2022, ENDING |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Your Social Security Number |

|

Spouse's Social Security Number |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Your First Name |

|

|

|

|

|

|

|

MI |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Your Last Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Does your name match the name on your social security card? If not, to ensure you get credit for your |

||||||||||

Spouse's First Name |

|

|

|

|

|

|

MI |

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

personal exemptions, contact SSA at |

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of county and incorporated city, town or special taxing area |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

in which you were employed on the last day of the taxable period |

|||

Spouse's Last Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

if you earned wages in Maryland. (See Instruction 6.) |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Current Mailing Address (PO Box, number, street and apt. no) |

|

|

|

|

|

|

|

|

|

|

|

Maryland County |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

Current Mailing Address Line 2 (Apt No., Suite No., Floor No.) |

|

|

|

|

|

|

|

|

|

|

|

City, Town or Taxing Area |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

City or Town |

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

ZIP Code + 4 |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Foreign Country Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign Province/State/County |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Foreign Postal Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

You must use Form 502X if you |

|

|

|

|

|

IF THIS IS BEING FILED TO CLAIM A NET OPERATING LOSS, CHECK |

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

STOP are changing to Resident status. |

|

|

|

|

|

THE APPROPRIATE BOX: |

|

|

|

CARRYBACK (farming loss only) |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CARRY FORWARD |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Check here if you are: |

|

|

|

Check here if your spouse is: |

IMPORTANT NOTE: Read the instructions and complete page 3 first. |

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

65 or over |

|

|

Blind |

|

65 or over |

|

|

Blind |

Attach copies of the federal loss year return and Form 1045, Schedules |

|||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

A and B. See Instruction 13. |

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Is this address different from the address on your original return? |

. . . . . . . . . . . . . . . |

|||||||||

Enter your state of legal residence |

|

. Enter the local jurisdiction of which you are a resident |

|

. |

||||||

Are you a resident of a local jurisdiction which imposes an income or earnings tax on Maryland residents? |

||||||||||

Enter dates you resided in Maryland |

|

|

- |

|

|

. |

|

|

||

Any changes from the original filing must be explained in Part III of this form. |

|

|||||||||

Did you request an extension of time to file the original return? |

. . . . . . . . . . . . . . . |

|||||||||

If yes, enter the date the return was filed |

|

|

. |

|

|

|

||||

Is an amended federal return being filed?. . . |

. . . . . . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . |

||||||

Has your original federal return been changed or corrected by the Internal Revenue Service? . . . . . . . . . . . . . . . . . . . . . . .

YES

YES

YES

YES YES

NO

NO

NO

NO NO

CHANGE OF FILING STATUS

Original Amended

Single

Married filing joint return or spouse had no income

Married filing separately

Original Amended

Head of household

Qualifying widow(er) with dependent child

Dependent taxpayer

Spouse's Social Security No.

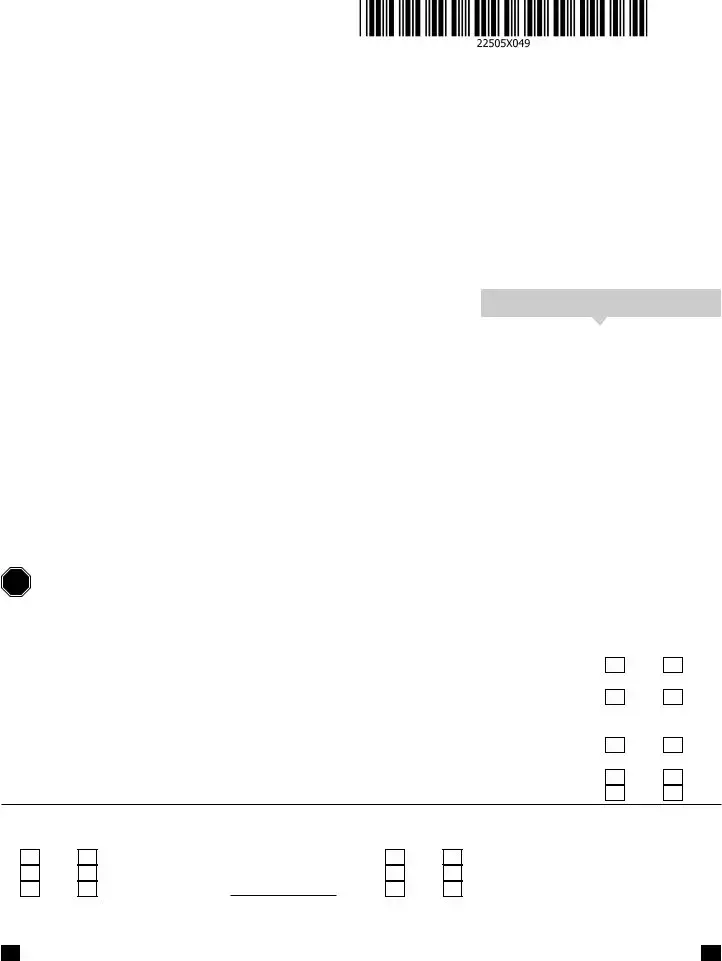

MARYLAND NONRESIDENT

FORM AMENDED TAX 505X RETURN

Last Name |

|

SSN |

|

|

|

|

|

|

|

|

|||

IMPORTANT NOTE: Read the instructions and |

A. As originally reported or |

B. Net change – increase |

||||

|

complete page 3 first. |

as previously adjusted |

or |

|||

|

|

|

(See instructions.) |

explain on page 4. |

||

1. Federal adjusted gross income . . . . . . . . . . . . . . . . . . 1.

2. Additions to income . . . . . . . . . . . . . . . . . . . . . . . . . . 2.

3. Total (Add lines 1 and 2.). . . . . . . . . . . . . . . . . . . . . . 3.

4. Subtractions from income . . . . . . . . . . . . . . . . . . . . . . 4.

5.Total Maryland adjusted gross income (Subtract line 4

from line 3.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.

6. CHECK ONLY ONE METHOD (See Instruction 5.)

STANDARD DEDUCTION METHOD

ITEMIZED DEDUCTION METHOD Enter total MD itemized deductions from Part II,

on page 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6. 7. Net income (Subtract line 6 from line 5.). . . . . . . . . . . 7.

8. Exemption amount (See Instruction 5.) . . . . . . . . . . . . 8.

9. Taxable net income (Subtract line 8 from line 7.) . . . . . 9.

10.Maryland tax from line 16 of revised

Form 505NR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10.

11.Special Nonresident tax from line 17 of

|

revised Form 505NR |

. . . . . . . . . . . . . . . |

. . . . 11. |

|

12. |

Total Maryland tax (Add lines 10 and 11.) |

. . . . 12. |

||

12a. |

Credits: |

|

|

|

|

Poverty Level Credit |

|

|

|

|

Personal Credit |

|

|

|

|

Business Credit |

X X X X X X X X X X |

|

|

|

Enter total credits |

. . . . . . . . . . . . . . . |

. . . 12a. |

|

12b. |

Maryland tax after credits (Subtract line 12a |

|

||

|

from line 12.) If less than 0, enter 0 |

. . . 12b. |

||

13.Contribution: 13a. 13b. 13c.

13d.

Enter total contributions (See Instruction 8.) . . . . . . . 13.

14.Total Maryland income tax and contribution (Add lines

12b and 13.) . . . . . . . . . . . . .. . . . . . . . . . . . . . . . 14.

15. Total Maryland tax withheld. . . . . . . . . . . . . . . . . 15.

16.Estimated tax payments and payments made

with Form PV and Form MW506NRS . . . . . . . . . . . . . 16.

17. Nonresident tax paid by

18.Refundable income tax credits

(Attach Form 502CR and/or 502S.) . . . . . . . . . . . . . 18.

19.Total payments and credits (Add lines 15

through 18.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19.

20. Balance due (If line 14 is more than line 19, subtract line 19 from line 14.) . . . . . . . . . . . . . . . . . . . . . . . . . 20.

21. Overpayment (If line 14 is less than line 19, subtract line 14 from line 19.) . . . . . . . . . . . . . . . . . . . . . . . . . 21.

22.Tax paid with original return, plus additional tax paid after it was filed

(Do not include any interest or penalty.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22.

23. Prior overpayment (Total all refunds previously issued.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23.

24.REFUND (If line 20 is less than line 22, subtract line 20 from line 22) (If line 23 is less than

line 21, subtract line 23 from line 21.) (Add line 21 to line 22.) (See Instruction 10.) . . . . . . . . . . REFUND 24.

2022

Page 2

C. Corrected amount.

MARYLAND NONRESIDENT

FORM AMENDED TAX 505X RETURN

Name |

|

SSN |

||

|

|

|

|

|

25.BALANCE DUE (If line 20 is more than line 22, subtract line 22 from line 20.) (Add line 20 to

line 23.) (If line 21 is less than line 23, subtract line 21 from line 23.) (See Instruction 10.) . . . . . . . . . . . . . 25.

26. Interest and/or penalty charges on tax due and/or from Form 502UP (See Instruction 11.) . . . . . . . . . . . . . . 26.

27. TOTAL AMOUNT DUE (Add line 25 and line 26.) . . . . . . . . . . . . . . . . .PAY IN FULL WITH THIS RETURN 27.

2022

Page 3

I. INCOME AND ADJUSTMENTS TO INCOME: You must complete the following using the amounts from your federal income tax return including any supporting schedules. If there are no changes to the amounts claimed on your original Maryland return, check here  and complete Column A and line 17 of Column C.

and complete Column A and line 17 of Column C.

INCOME AND ADJUSTMENTS INFORMATION |

|

|

(See Instruction 4.) (Use a minus sign ( - ) to indicate a loss.) |

|

|

1. |

Wages, salaries, tips, etc |

1. |

2. |

Taxable interest income |

2. |

3. |

Dividend income |

3. |

4.Taxable refunds, credits or offsets of state and local

|

income taxes |

4. |

5. |

Alimony received |

5. |

6. |

Business income or loss |

6. |

7. |

Capital gain or loss |

7. |

8. |

Other gains or losses (from federal Form 4797) |

8. |

9.Taxable amount of pensions, IRA distributions,

and annuities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9.

10.Rents, royalties, partnerships, estates, trusts, etc. (Circle

appropriate item.) . . . . . . . . . . . . . . . . . . . . . . . . . . 10.

11. Farm income or loss. . . . . . . . . . . . . . . . . . . . . . . . . 11.

12. Unemployment compensation . . . . . . . . . . . . . . . . . . 12.

13.Taxable amount of Social Security and Tier 1 Railroad

Retirement benefits. . . . . . . . . . . . . . . . . . . . . . . . . 13.

14.Other income (including lottery or other gambling

winnings) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14.

15. Total income (Add lines 1 through 14.) . . . . . . . . . . . 15.

16.Total adjustments to income from federal return (IRA,

alimony, etc.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16.

17.Adjusted gross income (Subtract line 16 from 15.) (Carry

the amount from line 17, column A, to page 1, line 1, column C.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17.

A. Federal income |

B. Maryland income |

|

C. |

|||||||

or loss ( - ) as corrected |

or loss ( - ) as corrected |

|

or loss ( - ) as corrected |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

II.ITEMIZED DEDUCTIONS: If you itemized deductions on your Maryland return, you must complete the following. If there are no changes to the

amounts claimed on your original Maryland return, check here  and complete Column A and line 11 of Column C.

and complete Column A and line 11 of Column C.

A. As originally reported |

B. Net increase |

C. Corrected amount |

or as previously adjusted |

or decrease ( - ) |

|

1. Medical and dental expense . . . . . . . . . . . . . . . . . . . . 1.

2.Taxes.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.

3. Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.

4. Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.

5. Casualty or theft losses. . . . . . . . . . . . . . . . . . . . . . . 5.

6. Miscellaneous . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.

7.Enter total itemized deductions from federal Schedule A 7.

8.Enter state and local income taxes included on

line 2 or from worksheet (See Instruction 4.) . . . . . . . 8.

9. Net deductions (Subtract line 8 from line 7.). . . . . . . . 9.

10.AGI factor (See Instruction 14 of the

nonresident instructions.) . . . . . . . . . . . . . . . . . . . . 10.

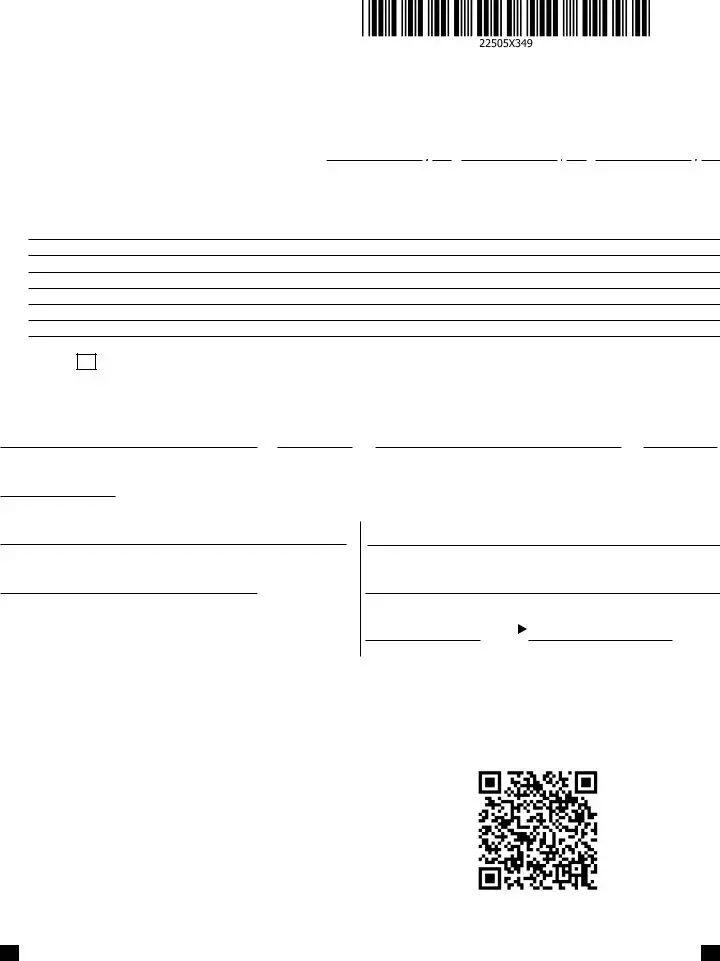

|

|

MARYLAND |

NONRESIDENT |

|

2022 |

|||

|

|

FORM |

|

|||||

|

|

AMENDED TAX |

|

Page 4 |

||||

|

|

505X |

|

|||||

|

|

RETURN |

|

|

||||

Name |

|

|

SSN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A. As originally reported |

B. Net increase |

C. Corrected amount |

|

|

|

|

|

|

or as previously adjusted |

or decrease ( - ) |

|

|

11.Total Maryland deductions (Multiply line 9 by line 10.) (Enter on page 2, in each appropriate column of line 6.) 11.

III.EXPLANATION OF CHANGES TO INCOME, DEDUCTIONS AND CREDITS: Enter the line number from page 1 and 2 for each item you are changing and give the reason for each change. Attach any required supporting forms and schedules for items changed.

Check here

if you authorize your preparer to discuss this return with us.

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief it is true, correct and complete. If prepared by a person other than taxpayer, the declaration is based on all information of which the preparer has any knowledge.

Your signature |

Date |

Spouse’s signature |

Date |

Taxpayer(s)' Daytime telephone no.

Printed name of the Preparer/Firm's name

Signature of preparer other than taxpayer (Required by Law)

Street address of preparer or Firm's address

City, State, ZIP Code + 4 |

|

Telephone number of preparer |

Preparer’s PTIN (Required by Law) |

Make checks payable to and mail to:

Comptroller of Maryland

Revenue Administration Division

110 Carroll Street

Annapolis, MD

It is recommended that you include your Social Security Number on check in blue or black ink.

To make an online payment, scan the QR code below and follow instructions.

MARYLAND |

NONRESIDENT |

|

FORM |

AMENDED TAX RETURN |

|

505X |

||

INSTRUCTIONS |

You must file your Amended Form 505X electronically to claim, or change information related to, business income tax credits from Form 500CR.

Changes made as part of an amended return are subject to audit for up to three years from the date that the amended return is filed.

WHEN AND WHERE TO FILE

Generally, Form 505X must be filed within three years from the date the original return was due (including extensions) or filed. The following exceptions apply.

•A claim filed after three years, but within two years from the time the tax was paid is limited to the amount paid within the two years immediately before filing the claim.

•A claim for refund based on a federal net operating loss carryback must be filed within 3 years after the due date (including extensions) of the return for the tax year of the net operating loss.

•If the claim for refund or credit for overpayment resulted from a final determination made by an administrative board or an appeal of a decision of an administrative board, that is more than three years from the date of filing the return or more than two years from the time the tax was paid, the claim for refund must be filed within one year of the date of the final decision of the administrative board or final decision of the highest court to which an appeal of the administrative board is taken.

•If the Internal Revenue Service issues a final determination of adjustments that would result in a decrease to Maryland taxable income, file an amended return within one year after the final adjustment report or the final court decision if appealed.

•If the Internal Revenue Service issued a final determination of adjustments that would result in an increase to Maryland taxable income, file the amended return within ninety days after the final determination.

Do not file an amended return until sufficient time has passed to allow the original return to be processed. For current year returns, allow at least six weeks. Note that no refund for less than $1.00 will be issued.

The amended return must be filed with the

Comptroller of Maryland

Revenue Administration Division

110 Carroll Street

Annapolis, MD

For more information regarding refund limitations, see Administrative Release 20.

PROTECTIVE CLAIMS

A protective claim is a claim for a specific amount of refund filed on an amended return with a request that the Comptroller delay acting on the refund request. The claim for refund may not be based on a federal audit. The delay requested must be due to a pending decision by a state or federal court which will affect the outcome of the refund, or for reasonable cause. The protective claim must be filed in accordance with the limitations outlined in the section WHEN AND WHERE TO FILE. The Comptroller may accept or reject a protective claim. If rejected, the taxpayer will be informed of a right to a hearing. We cannot accept a protective claim unless an original return has been filed.

PENALTIES

There are severe penalties for failing to file a tax return, failing to pay any tax when due, filing false or fraudulent returns or making a false certification. The penalties include criminal fines, imprisonment and a penalty on your taxes. In addition, interest is charged on amounts not paid when due.

2022

Page 1

To collect unpaid taxes, the Comptroller is directed to enter liens against the salary, wages or property of delinquent taxpayers.

PRIVACY ACT INFORMATION

The Revenue Administration Division requests information on tax returns to administer the income tax laws of Maryland, including determination and collection of correct taxes. If you fail to provide all or part of the requested information, the exemptions, exclusions, credits, deductions or adjustments may be dis- allowed and you may owe more tax. In addition, the law provides penalties for failing to supply information required by law or regulations.

You may look at any records held by the Revenue Administration Division which contain personal information about you. You may inspect such records, and you have certain rights to amend or correct them.

As authorized by law, information furnished to the Revenue Administration Division may be given to the Internal Revenue Service, a proper official of any state that exchanges tax information with Maryland and to an officer of this state having a right to the information in that officer’s official capacity. The information also may be obtained with a proper legislative or judicial order.

USE OF FEDERAL RETURN

Most changes to your federal return will result in changes on your Maryland return and you will need the information from your federal amendment to complete your Maryland amended return. Therefore, complete your federal return first. Maryland law requires that your income and deductions be entered on your Maryland return exactly as they were reported on your federal return and schedules. However, all items reported on your Maryland return are subject to verification, audit and revision by the Comptroller’s Office.

If you are amending your federal return, attach a photocopy of the federal Form 1040X and any revised schedules to your Maryland Form 505X. If your tax has been increased by the Internal Revenue Service, you must report this increase to the Revenue Administration Division within 90 days from the final IRS determination.

1NAME AND ADDRESS INFORMATION.

Enter the Social Security number, correct name and cur- rent address on the lines. Be sure to check the appropriate box if you or your spouse are 65 or over or blind on the last day of the tax year. If your address is different from the address on your original return, be sure to answer “Yes” to the first question.

If using a foreign address, complete the lines indicated for Country Name, Province/State/County, and Postal Code.

2QUESTIONS.

Answer all of the questions and attach copies of any fed- eral notices, amended forms and schedules. If filing your amended return for a Net Operating Loss Carryback or Carryforward, check the appropriate box. Provide the dates you resided in Maryland for the tax year and explain any changes from your original filing in Part III of Form 505X.

3FILING STATUS.

Enter the filing status you used on your original return and show any change of filing status. Your filing status should

correspond to the filing status used on your federal return.

Generally, you may not change from married filing joint to mar- ried filing separately after the original due date of the return. Any change in filing status to or from married filing joint requires the

2022

Page 2

LINE 6 – Method of computation.

Standard deduction method. The standard deduction is 15% of the Maryland adjusted gross income with the following mini- mums and maximums.

signature of both spouses. Enter a complete explanation in Part III of Form 505X.

4COMPLETE PAGES 3 AND 4 OF FORM 505X.

PART I

Enter the amount of income (or loss) from your federal return as corrected in Column A. Enter the amount of your Maryland income (or loss) as corrected in Column B. Enter the amount of your

PART II

Filing Status

Single

Married filing separately

Dependent taxpayer

Filing Status

Married filing joint or spouse had no income

Head of household

Qualifying widow(er) with dependent child

–Minimum of $1,600 and maximum of $2,400

–Minimum of $3,200 and maximum of $4,850

If you itemized deductions, enter your original or previously adjusted amounts in Column A. Enter any increase (or decrease) in Column B and enter the corrected amounts in Column C.

Any amount deducted as contributions of Preservation and Conservation Easements for which a credit is claimed on Form 502CR must be included on line 8. On line 10, enter the adjusted gross income factor from the worksheet in Instruction 5.

PART III

Use this section to provide a detailed explanation of the changes being made on the amended return. A filing status change must be fully explained here.

Enter the line number from pages 1 and 2 for each item you are changing and state the reason for the change. Be sure to attach revised Form 505NR and any other required schedules or forms.

NOW COMPLETE PAGES 1 AND 2 OF FORM 505X.

COLUMNS

In Column A, enter the amounts from your return as originally filed or as previously adjusted or amended.

In Column B, enter the net increase or net decrease for each line you are changing. Use a minus sign ( - ) to indicate a decrease. Explain each change in Part III of Form 505X and attach any related schedule or form. If you need more space, show the required information on an attached statement. For Column C, add the increase in Column B to the amount in Column A, or subtract the Column B decrease from Column A. For any item you do not change, enter the amount from Column A in Column C.

5FIGURE YOUR MARYLAND AND SPECIAL NONRESIDENT TAX.

LINE 1 – Income and adjustments from federal return. Copy the amounts from your federal amended return or as cor- rected by the IRS. Be sure to reconcile this figure to Part 1 of Form 505X and enter a complete explanation of the changes in Part III.

LINE 2 – Additions to income. For decoupling and tax prefer- ence items and amounts to be added when credits are claimed, include corrected Form(s) 500DM, 502TP, 502CR or 500CR. In addition, enter the amount equal to a tax credit claimed for tax paid on distributive or

LINE 4 – Subtractions from income. Enter items such as child care expenses and any other subtractions as shown in the 2022 Nonresident Income Tax Return Instructions. Enter an explana- tion of the changes in Part III and attach any corrected forms.

Itemized deduction method. Check the box and enter your total Maryland itemized deductions.

LINE 8 – Exemptions. The personal exemption is $3,200. This exemption amount is reduced once the taxpayer's federal adjust- ed gross income exceeds $100,000. ($150,000 if filing Joint, Head of Household or Qualifying Widow(er) with Dependent Child). If you are subject to this reduction, see the exemption chart in the 2022 Nonresident Income Tax Return Instructions. Taxpayers 65 years or over or blind get an additional exemption of $1,000.

Multiply the exemption amount by the AGI factor in the ADJUSTED GROSS INCOME FACTOR WORKSHEET to calculate the amount of the exemption to enter in column C. Use the exemption amount that you had claimed on your original return (or as previously adjusted) in Column A of line 8. The difference between these two figures should be entered in Column B of line 8.

Attach amended Form 502B if you are changing dependent infor- mation.

Adjusted Gross Income (AGI) Factor. You must adjust your standard or itemized deductions and exemptions using the AGI factor calculated in the worksheet below. Carry this amount to six decimal places. NOTE: If Mary- land adjusted gross income before subtractions (line 2) is 0 or less, use 0 as your factor. If your federal adjusted gross income (line 1) is 0 or less and line 2 is greater than 0, use 1 as your factor.

ADJUSTED GROSS INCOME FACTOR WORKSHEET (5)

1.Enter your federal adjusted gross

income (from line 17, column 1) . . . . .1 _____________

2.Enter your Maryland adjusted gross income before subtraction of

3. AGI factor. Divide line 2 by line 1 . . . .3 .

LINE 10 – Computing the tax. Complete Form 505NR follow- ing the instructions in the nonresident booklet using corrected figures to determine the tax. Line 16 of the revised Form 505NR is entered on line 10 of Form 505X. Line 17 of the revised Form 505NR is entered on line 11 of Form 505X.

6POVERTY LEVEL CREDIT, CREDITS FOR INDIVIDUALS AND BUSINESS TAX CREDITS.

Enter each credit being claimed on the appropriate line on line 12a.

You may claim a credit on line 12a equal to 5% of your earned income. If your income is less than the poverty level guidelines, refer to the nonresident instructions and worksheet to compute the allowable credit. You must prorate the poverty level credit using the Maryland income factor.

Personal income tax credits from Form 502CR and business tax credits from Form 500CR should be entered in the appropriate field on line 12a. If these amounts are different from the original return, be sure to attach the completed Form 502CR and/or Form 500CR with appropriate documentation or certifications.

If the total credits on line 12a are greater than the tax on line 12, enter zero on line 12b. The credits entered on line 12a are nonrefundable. For information concerning refundable credits, see Instruction 9.

You must file your amended return electronically to claim a business tax credit from Form 500CR.

7SPECIAL NONRESIDENT INCOME TAX.

The special nonresident tax is calculated on line 17 of revised Form 505NR.

8CONTRIBUTIONS TO THE CHESAPEAKE BAY AND ENDANGERED SPECIES FUND, DEVELOPMENTAL DISABILITIES SERVICES AND SUPPORT FUND, MARYLAND CANCER FUND AND FAIR CAMPAIGN FINANCING FUND.

Enter the amounts of your contribution in 13a for the Chesapeake Bay and Endangered Species Fund, 13b for the Developmental Disabilities Services and Support Fund, 13c for the Maryland Cancer Fund and 13d for the Fair Campaign Financing Fund. Any contribution will increase your balance due or reduce your refund. Enter the total of your contributions in the appropriate columns. Additional information concerning the funds is con- tained in the Maryland tax instructions for the tax year of the amended return.

9TAXES PAID AND CREDITS.

Write your taxes paid and credits on lines

Enter the correct amounts on lines 15 through 18 and attach any additional or corrected

Refundable Income Tax Credits. Enter the total of your refundable income tax credits on line 18. Attach Form 502CR and/or 502S.

1.STUDENT LOAN DEBT RELIEF TAX CREDIT. If you have incurred at least $20,000 in undergraduate or graduate stu- dent loan debt, you may qualify for this credit. A copy of the required certification from the Maryland Higher Education Commission must be included with Form 502CR.

2.HERITAGE STRUCTURE REHABILITATION TAX CREDIT. A credit is allowed for a percentage of qualified rehabilitation expenditures as certified by the Maryland Historical Trust. Attach a copy of Form 502S and certification.

2022

Page 3

3.REFUNDABLE BUSINESS INCOME TAX CREDIT. Form 500CR Instructions are available online at www.maryland- taxes.gov. You must file Form 500CR electronically to claim a business income tax credit.

4.IRC SECTION 1341 REPAYMENT. If you repaid an amount this year reported as income on a prior year federal tax return that was greater than $3,000, you may be eligible for an IRC Section 1341 repayment credit. See Administrative Release 40.

5.CATALYTIC REVITALIZATION PROJECTS AND HISTORIC REVITALIZATION TAX CREDIT. If you are an individual, business entity, or nonprofit organization, you may claim a tax credit in an amount equal to 20% of the amount stated in the final tax credit certificate issued by the Secretary of this sub- title for 5 consecutive taxable years beginning with the Catalytic Revitalization Projects is completed. See Form 502CR instructions.

7.CREDIT FOR CHILD AND DEPENDENT CARE EXPENSES If your Maryland credit for child and dependent care expenses exceeds your Maryland Tax, you may qualify for this credit.

9.PTE TAX PAID ON MEMBERS’ DISTRIBUTIVE OR PRO RATA SHARES OF INCOME TAX CREDIT If you are the ben- eficiary of a trust or a Qualified Subchapter S Trust which elected to pay the tax imposed with respect to members’ dis- tributive or pro rata shares, you may be entitled to a credit for your share of that tax. Enter the amount on this line and attach the Maryland Schedule

If you are a member of a PTE

10 BALANCE DUE OR OVERPAYMENT.

Calculate the balance due or overpayment by subtracting the total on line 19 from the amount on line 14 and enter the result on either line 20 or line 21.

Enter the tax paid with the original return plus any additional tax paid after filing on line 22 (do not enter interest or penalty paid) OR enter the overpayment from your original return plus any additional overpayments from prior amendments or adjustments on line 23.

If there is an amount on line 20:

•and line 20 is more than line 22, you owe additional tax. Enter the difference on line 25 and compute the interest due using the interest rates in Instruction 11.

|

|

|

|

|

2022 Tax Rate Schedules |

|

|

|

|

|||

|

|

Tax Rate Schedule I |

|

|

Tax Rate Schedule II |

|||||||

For taxpayers filing as Single, Married Filing Separately, or as |

For taxpayers filing Joint, Head of Household, or for Qualifying |

|||||||||||

Dependent Taxpayers. This rate is also used for taxpayers filing as |

Widows/Widowers. |

|

|

|

||||||||

Fiduciaries. |

|

|

|

|

|

|

|

|

|

|

||

If taxable net income is: |

|

Maryland Tax is: |

If taxable net income is: |

|

Maryland Tax is: |

|||||||

|

At least: |

but not over: |

|

|

|

|

||||||

At least: |

but not over: |

|

|

|

|

|

|

|

|

|||

|

|

|

|

$0 |

$1,000 |

|

|

2.00% of taxable net income |

||||

$0 |

$1,000 |

|

|

2.00% |

of taxable net income |

|

|

|||||

|

|

$1,000 |

$2,000 |

$20.00 |

plus |

3.00% |

of excess over $1,000 |

|||||

$1,000 |

$2,000 |

$20.00 |

plus |

3.00% |

of excess over $1,000 |

|||||||

$2,000 |

$3,000 |

$50.00 |

plus |

4.00% |

of excess over $2,000 |

|||||||

$2,000 |

$3,000 |

$50.00 |

plus |

4.00% |

of excess over $2,000 |

|||||||

$3,000 |

$150,000 |

$90.00 |

plus |

4.75% |

of excess over $3,000 |

|||||||

$3,000 |

$100,000 |

$90.00 |

plus |

4.75% |

of excess over $3,000 |

|||||||

$150,000 |

$175,000 |

$7,072.50 |

plus |

5.00% |

of excess over $150,000 |

|||||||

$100,000 |

$125,000 |

$4,697.50 |

plus |

5.00% |

of excess over $100,000 |

|||||||

$175,000 |

$225,000 |

$8,322.50 |

plus |

5.25% |

of excess over $175,000 |

|||||||

$125,000 |

$150,000 |

$5,947.50 |

plus |

5.25% |

of excess over $125,000 |

|||||||

$225,000 |

$300,000 |

$10,947.50 |

plus |

5.50% |

of excess over $225,000 |

|||||||

$150,000 |

$250,000 |

$7,260.00 |

plus |

5.50% |

of excess over $150,000 |

|||||||

$300,000 |

|

$15,072.50 |

plus |

5.75% |

of excess over $300,000 |

|||||||

$250,000 |

|

$12,760.00 |

plus |

5.75% |

of excess over $250,000 |

|

||||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

•and there is also an amount on line 23, you owe additional tax. Add the two together and enter the total on line 25. Compute the interest due. See Instruction 11.

•and line 20 is less than line 22, you are due a refund. Enter the difference on line 24.

If there is an amount on line 21:

•and line 21 is more than line 23, you are due an additional refund. Enter the difference on line 24.

•and there is also an amount on line 22, you are due an addi- tional refund. Add the two together and enter on line 24.

•and line 21 is less than line 23, you owe additional tax. Enter the difference on line 25 and compute the interest due using the interest rates in Instruction 11.

Previous interest and penalty

Interest and/or penalty charges for the year you are amending, whether previously paid or still outstanding, may be adjusted as a result of your amendment. Any payments made on the account have been applied first to penalty, then to interest and lastly to tax due. These payments may require reallocation depending on the result of the amendment. We will notify you of the net bal- ance due or refund when we have completed processing your Form 505X.

NOTE: If all or part of the overpayment on your original return was credited to an estimated tax account for next year, we can- not reduce or remove this credit without specific authorization from you. If you have a balance due, and wish to apply monies credited to a 2023 estimated tax account, attach written autho- rization for the amount to be removed. Interest charges are assessed even if the balance due is removed from the 2023 account.

11 INTEREST ON TAX DUE AND INTEREST FOR

UNDERPAYMENT OF ESTIMATED TAX.

INTEREST ON TAX DUE

Interest must be computed and paid on any balance of tax due. Interest is due from the date the return originally was due to be filed until the date the tax is paid. The annual interest rate is 9.5% through 12/31/22. The annual interest rate will change after 12/31/22.

For additional information, visit www.marylandtaxes.gov.

INTEREST ON UNDERPAYMENT OF ESTIMATED TAX

If you do not meet the requirement for avoidance of interest for underpayment of estimated tax, obtain Form 502UP online at www.marylandtaxes.gov or from any office of the Revenue Administration Division. Complete and attach it to your amended return. Enter any interest due on line 26 of Form 505X.

If you calculated and paid interest on underpayment of esti- mated tax with your original return, recalculate the interest based on your amended tax return, and attach a copy of a revised Form 502UP showing your recalculation.

12 SIGNATURE, ATTACHMENTS AND PAYMENT INSTRUCTIONS.

Sign and date your return on page 4 and attach all required forms, schedules and statements.

SIGNATURES

You must sign your return. Both spouses must sign a joint return. Your signature(s) signify that your return, including all attachments, is, to the best of your knowledge and belief, true, correct and complete, under the penalties of perjury.

TAX PREPARERS

If another person prepared your return, that person must also

2022

Page 4

print name, sign the return and enter their preparer’s tax identi- fication number (PTIN). The preparer declares that the return is based on all information required to be reported of which the preparer has knowledge, under the penalties of perjury. Penalties may be imposed for tax preparers who fail to sign the tax return and provide their preparers tax identification number.

ATTACHMENTS

Be sure to attach wage and tax statements (Forms

MAILING INSTRUCTIONS

Mail your return to:

Comptroller of Maryland

Revenue Administration Division

Amended Return Unit

110 Carroll Street

Annapolis, MD

PAYMENT INSTRUCTIONS

Make your check or money order payable to “Comptroller of Maryland.” Write the type of tax and year of tax being paid on your check. It is recommended that you include your Social Security Number on check using blue or black ink.

DO NOT SEND CASH.

13 NET OPERATING LOSS (NOL).

To claim a deduction for a federal NOL on the Maryland return, you must first calculate the NOL for federal pur- poses. A deduction will be allowed on the Maryland return for the amount of the loss actually utilized on the federal return. The amount of loss utilized for federal purposes is generally equal to the federal taxable income (before loss is used) or the federal modified taxable income as calcu- lated for the year of carryback or carryforward.

An addition or subtraction modification may be required in a car- ryback or carryforward year when the federal NOL, or the year to which the NOL is carried, includes items included in certain provisions of the Internal Revenue Code from which the State of Maryland has decoupled, including certain special depreciation allowances and

An NOL generated when an individual or a business entity is not subject to Maryland income tax law, in a tax year beginning on or after October 22, 2007, cannot be used as a deduction to offset Maryland income. For acquisitions or liquidations occurring on or after October 22, 2007, the acquiring business entity which is subject to Maryland income tax law cannot use the acquired or liquidated business entity’s NOL as a deduction to offset Maryland income, if the acquired or liquidated business entity was not subject to Maryland income tax law when its NOL was generated. An NOL being carried forward from tax years beginning before October 22, 2007 can be used until exhausted.

An addition to income may be required in a carryback or carry- forward year if the total Maryland additions to income exceeds the total Maryland subtractions from income in the loss year. The required addition to income represents a recapture of the excess additions over subtractions. The addition to income required is generally equal to the lesser of the NOL deduction in the carryback year or the net addition modification (NAM) in the loss year unless the loss year includes a decoupling modification. For more information regarding NAM, refer to Administrative Release 18.

If an election to forgo a carryback is made, a copy of the federal

2022

Page 5

election for the loss year must be attached with the Maryland amended return.

You must attach copies of federal Form 1045 or 1040X, whichever was used for federal purposes, and a copy of the federal income tax return for the year of the loss. Also include Schedules A and B of Form 1045 or the equivalent worksheets used to develop the federal NOL and show the amounts utilized on the federal return in the carryback or carryforward years. Check the appropriate box on the front of Form 505X located directly below the name and address.

14 INCOME TAX ASSISTANCE.

For more information, visit www.marylandtaxes.gov or email your question to: TAXHELP@marylandtaxes.gov. You may also call

REMINDER: Attach a revised Form 505NR to your 2022 Amended Nonresident Return.

File Breakdown

| Fact | Detail |

|---|---|

| Form Name | Maryland 505X Form |

| Purpose | Amended Tax Return for Nonresidents |

| Tax Year | 2021 |

| Key Features | Allows adjustments to income, deductions, and credits |

| Special Conditions | Includes options for claiming net operating loss |

| Governing Law | Maryland State Tax Law |

| Important Sections | Income and Adjustments to Income, Itemized Deductions, Explanation of Changes |

Steps to Filling Out Maryland 505X

When you need to amend a previously filed nonresident Maryland tax return, Form 505X is the document you seek. This process allows for corrections to income, deductions, or credits reported incorrectly on your original return. Filling out this form accurately ensures that your tax records with the state of Maryland are correct and up to date. Here is a step-by-step guide to help you through each part of the form with clarity.

- Begin with your personal information. This includes your Social Security Number, your spouse's Social Security Number if married filing jointly, and your full names. Ensure all this information matches what's on your Social Security card.

- Enter your current mailing address, including the county and the name of the incorporated city, town, or special taxing area in Maryland where you were employed at the end of the taxable period.

- Designate your legal state of residence and local jurisdiction.

- Indicate any changes in your filing status by selecting the appropriate box for your current and original filing statuses.

- Under Income and Adjustments to Income, complete the sections as instructed, using information from your federal tax return. Ensure you distinguish between federal, Maryland, and non-Maryland income or losses.

- If applicable, update your itemized deductions in the section provided. You should reflect any net increases or decreases from what was originally reported or as previously adjusted.

- Correct the amounts for exemptions, deductions, Maryland tax, special nonresident tax, credits, contributions, and Maryland income tax and contribution in the summary section. This will help determine if you owe more tax or are due a refund.

- Calculate the total Maryland tax withheld, estimated tax payments, payments made with specific Maryland forms, and any nonresident tax paid by pass-through entities. Also include any refundable income tax credits.

- Determine your overpayment or balance due, considering taxes paid with the original return and any adjustments for refunds or additional taxes paid afterward.

- Provide an explanation for each change you made on the form in Part III. Attach any required supporting documents for the changes.

- Complete the signature section with your signature and date. If you're filing jointly, ensure your spouse also signs the form. Include your daytime telephone number.

- If someone other than you prepared the form, that individual must also sign and provide their information at the bottom of the form.

- Finally, if you owe an additional amount, make your check payable to the Comptroller of Maryland and send it along with Form 505X to the provided address. Remember to write your Social Security Number on the check for identification purposes.

By following these steps carefully, you will be able to accurately complete and submit your Maryland Form 505X, ensuring your tax records are updated and accurate.

More About Maryland 505X

What is Form 505X, and who needs to file it?

Form 505X is the amended tax return form designed for nonresidents who need to make changes or corrections to their previously filed Maryland nonresident tax return for the year 2021. If a nonresident has already submitted a Maryland state tax return but needs to update their income, deductions, credits, or any other information, they should file Form 505X. This includes adjustments to federal adjusted gross income, changes in deductions or personal information, and corrections of errors or omissions on the original tax return. It is also applicable for those claiming a net operating loss.

How do I complete Form 505X?

To accurately complete Form 505X, you should follow these steps:

- First, gather your originally filed Maryland nonresident tax return and any supporting documents used for that filing.

- Next, review the instructions on page 3 of Form 505X, which guide you through adjustments in your income, deductions, and credits.

- Fill out your income and adjustments to income on the first page, making sure to detail any changes from your original return in the appropriate columns.

- If you itemized deductions, complete the section on itemized deductions as instructed, adjusting amounts as necessary.

- In Part III, provide a detailed explanation for each change you are making to your original return. Attach any necessary supporting documents or schedules for the changes.

- Review the entire form for accuracy, sign and date at the bottom, and prepare it for submission.

Can Form 505X be filed electronically?

As of the latest guidelines, Maryland does not universally allow the electronic filing of the Form 505X for nonresidents. Taxpayers are advised to check with the Comptroller of Maryland's official website or contact their tax professionals to determine if electronic filing options have become available for the 505X Form since this requirement may change over time. Therefore, in most cases, taxpayers will need to mail in the completed Form 505X along with any supporting documentation to the Comptroller of Maryland.

When should Form 505X be filed?

Form 505X should be filed as soon as the taxpayer realizes that their original nonresident Maryland tax return requires amendment. However, there are deadlines for when amendments can be made, typically within three years from the due date of the original return or two years from the date the Maryland tax was paid, whichever is later. If expecting a refund from the amendment, it is crucial not to delay the filing as this can affect your eligibility to receive that refund.

How do I calculate the refund or amount I owe after filing Form 2250X?

To calculate the refund or amount owed after filing Form 505X:

- Start by determining your corrected Maryland adjusted gross income, considering the changes to your federal adjusted gross income, additions or subtractions to income, and any modifications to itemized or standard deductions.

- Apply the corrected figures to calculate your taxable income, Maryland tax, and any applicable credits or special nonresident tax.

- Subtract the total Maryland tax after credits from the total payments and credits you have already made, including any Maryland tax withheld and estimated tax payments.

- If the result shows that the total payments and credits exceed the tax after credits, you have an overpayment and may be eligible for a refund. Alternatively, if the tax after credits exceeds your payments, you owe the difference to the state.

Common mistakes

When filling out the Maryland 505X form, which is used for amended nonresident tax returns, people often make mistakes that can delay processing or affect the accuracy of their tax assessment. Below are six common errors identified:

- Incorrect Social Security Numbers (SSNs): Putting down the wrong SSN or leaving it blank can lead to processing delays or incorrect tax assessments.

- Choosing the Wrong Tax Year: Filling out the form for the incorrect tax year can cause confusion and delays. It’s crucial to ensure that you are amending the return for the correct year.

- Not Attaching Required Documents: Failure to attach copies of the federal loss year return and Form 1045, Schedules A and B, as mentioned in the important note, can result in processing delays.

- Omitting Changes to Income or Deductions: Any changes from the original filing must be clearly explained in Part III of the form. Not doing so can result in discrepancies.

- Incorrect Calculation or Entry of Deductions: When it comes to entering deductions, such as itemized or standard deductions, mistakes in calculation or placement can affect your taxable income calculation.

- Not Updating Personal Information: If your current mailing address or personal information has changed since the original return, failing to update this information can lead to communication issues.

To avoid these issues, it's recommended to double-check all entries and required documentation before submitting the Maryland 505X form. Ensuring accuracy in every detail can help in the smooth processing of your amended tax return.

Documents used along the form

When filing an amended tax return with the Maryland 505X form, typically for nonresidents who need to adjust their previously filed tax information, various other forms and documents might need to be included to support the changes made. These documents and forms play a crucial role in ensuring that the amendment process is smooth and accurate. Each has its specific purpose and requirements.

- Form 502X: Used by residents who need to amend their Maryland tax returns. It's similar to the 505X but tailored for residents.

- Form 1045, Schedules A and B: This form is necessary for documenting any carryback of a net operating loss, showing detailed calculations that might affect tax obligations.

- Form PV: Maryland's Payment Voucher form is used when making a payment with the amended return if additional taxes are owed.

- Form MW506NRS: A form used for nonresident sellers of real property located in Maryland to calculate and report withholding tax due.

- Form 502CR: This form is for claiming various credits that a filer might be eligible for, which can include income tax credits, poverty level credits, and more.

- Form 502S: Specifically used for sustainable communities tax credit, often accompanying amended returns when relevant adjustments are made.

- W-2 or 1099 forms: Wage and income statements that support any changes made to income, withholdings, or tax credits claimed on the amended return.

- Federal 1040X: If amending a federal tax return is necessary, the IRS requires Form 1040X. This may be needed alongside Maryland's 505X to ensure both state and federal records match.

- Schedule A: For those who itemize their deductions, an updated Schedule A may be necessary to reflect any changes to deductions claimed.

Filing an amended tax return can often be as complex as the initial filing process. Each of these forms and documents serves a specific purpose, whether it's adjusting income, claiming additional credits, or correcting deductions. Making sure to include the correct supporting documentation is key to accurately processing your amended return and avoiding delays or audits. As tax situations can greatly vary, consulting with a tax professional might be beneficial to navigate the specifics of your amendment needs.

Similar forms

The Maryland 505X form is similar to the federal Form 1040X, the Amended U.S. Individual Income Tax Return. Like the 1040X, the 505X allows individuals to make changes to a previously filed tax return. Both forms require the taxpayer to provide their original reported amounts, describe the changes being made, and calculate the net result of those changes. Taxpayers use these forms to correct errors or claim a more favorable tax status. The layout is designed to walk the taxpayer through the amendment process step by step, ensuring all necessary information is accounted for and correctly adjusted.

In addition, the Maryland 505X form parallels the Form 502X, Amended Maryland Tax Return for residents. While the 505X is specifically for nonresidents who need to amend their Maryland income tax returns, the 502X serves the same purpose for residents. Both demand detailed explanations for income, deductions, and credits adjustments, alongside necessary documentation. They share a common structure focused on recalculating tax obligations based on the corrected information, ensuring that taxpayers meet their legal requirements while adjusting for any potential refunds or additional liabilities.

Dos and Don'ts

When working on the Maryland 505X form, an amended tax return for nonresidents, navigating the process with both precision and caution is essential. Whether you're correcting a minor mistake, claiming a previously missed deduction, or updating your income information, understanding what to do, and what not to do, can be the key to a smoother process and potentially faster processing time. Here’s a helpful list of dos and don’ts:

- Do read the instructions carefully before beginning. The Maryland 505X form comes with detailed instructions designed to guide you through the process of amending your nonresident return correctly. Skipping this step can lead to errors and potentially delay the processing of your amendment.

- Don't use Form 505X if you are changing to resident status. If your status has changed, you must use Form 502X, as 505X is specifically designed for nonresidents who need to amend their Maryland tax returns.

- Do attach any required supporting forms and schedules for items you're changing. Proper documentation is crucial when making amendments to your tax return. This could include a revised W-2, 1099 forms, or any additional schedules that support the changes you are reporting.

- Don't forget to explain the changes you're making. Part III of the 505X form is where you'll provide a detailed explanation for each change to your income, deductions, and credits. It's important to be clear and concise in your explanations to avoid confusion or further inquiries from the Maryland Comptroller's Office.

- Do ensure your name matches the name on your Social Security card. If it doesn't, you should contact the Social Security Administration to update your records. This seemingly small detail can cause significant issues with your tax processing if overlooked.

- Don't hastily fill in your information. Slow down when completing your address, Social Security number, and other personal details. Mistakes here can lead to your amended return being misdirected or delayed.

Tackling the Maryland 505X form doesn't have to be a daunting task. By following these straightforward dos and don’ts, you can navigate the process more confidently. Remember, accuracy and thoroughness are your best allies in ensuring a successful amendment to your Maryland nonresident tax return.

Misconceptions

Many individuals have misconceptions about the Maryland 505X form, the amended tax return for nonresidents. Understanding these common errors can help taxpayers accurately complete their submissions, ensuring they meet their obligations while maximizing potential benefits. Here are seven key misconceptions explained:

- Only for correcting mistakes: While the 505X form is often used to correct errors, it's also necessary for reporting additional income, changing filing status, or claiming deductions or credits not previously claimed.

- Residency changes aren't applicable: Contrary to some beliefs, if a taxpayer's residency status changes, they cannot use Form 505X to reflect this change. A different form, Form 502X, is required for changing residency status.

- Availability for joint filers only: Some think the 505X is only for those who filed jointly. However, it can be used by any nonresident taxpayer who needs to amend a Maryland tax return, regardless of their original filing status.

- Amendments result in audits: Filing a 505X does not automatically trigger a state tax audit. While there's an inherent risk of audit with any tax return filing, amendments are a normal part of tax administration.

- No deadline for filing: There is a common misconception that the 505X form can be filed at any time. However, amendments must be submitted within three years from the date the original return was filed, or two years from the date the tax was paid, whichever is later.

- No verification needed: Some taxpayers mistakenly believe that amending a return with the 505X requires no further documentation. In reality, taxpayers must attach supporting documentation for any changes, including a copy of the federal amendment if applicable.

- Direct adjustment to tax due: Another misconception is that entering changes directly adjusts the tax due or refund owed on the 505X. Taxpayers must calculate the impact of the amendment on their tax liability, which can involve complex calculations, especially regarding deductions and credits.

Correcting these misconceptions is essential for ensuring the proper completion of the Maryland 505X form. Thoroughly reviewing instructions, understanding the requirements, and preparing necessary documentation can help taxpayers navigate the amendment process more effectively.

Key takeaways

Here are six key takeaways about filling out and using the Maryland 505X form, which is an amended tax return form for nonresidents:

- The Maryland 505X form is specifically designed for amending previously filed nonresident tax returns for the year 2021 or the fiscal year beginning in 2021.

- It is crucial for individuals to verify that the name on the form matches the one on their social security card. In case of discrepancies, contacting the Social Security Administration is necessary to ensure credit for personal exemptions.

- If there is a change of filing status from the original tax return, this form allows individuals to indicate such changes clearly, ensuring the accuracy of their revised tax obligations.

- Details about any federal adjustments, such as a changed or corrected federal return by the Internal Revenue Service, must be disclosed on the Maryland 505X. This ensures the state tax implications of federal adjustments are properly accounted for.

- Completing the income and adjustments to income section accurately requires using information from the federal income tax return, highlighting the interconnectedness of state and federal tax filings.

- If an individual itemized deductions on their original Maryland return, the 505X form requires detailed information on such deductions, ensuring that any corrections to itemized deductions are properly reflected in the amended state return.

Making sure that every detail is accurate and properly corrected on the Maryland 505X form is crucial for nonresidents who need to amend their tax return. Each step, from including social security numbers to detailing federal adjustments, plays a significant role in ensuring the amended tax return is both accurate and compliant with Maryland tax laws.

Common PDF Templates

Md Form 510 Instructions 2023 - A denied extension application will result in the requirement for the entity to file its income tax return within 10 days or by the original due date.

Maryland Concealed Carry Law Change - Date and time of the range qualification attempt must be recorded to provide context for performance.