Maryland 510D PDF Template

Navigating the complexities of tax compliance can often seem like a daunting task for pass-through entities (PTEs) operating within Maryland. The Maryland 510D Form, known as the Pass-Through Entity Declaration of Estimated Income Tax, stands as a critical component in this landscape, especially from the fiscal year beginning in 2012. This form enables S corporations, partnerships, limited liability companies, and business trusts to declare and remit their estimated income tax. It's designed to ensure that all nonresident members of these entities are accounted for tax-wise, with specific rates applied to individuals and nonresident entities alike. For instance, nonresident individual members face a tax rate of 5.75%, in addition to a special nonresident tax of 1.25%, while nonresident entities are taxed at 8.25% of their distributive share of income. The form outlines a structured approach to calculating and paying these taxes, with quarterly payments required if the total estimated tax exceeds $1,000 for the year. Moreover, it details the importance of accurately reporting and paying to avoid penalties, provides guidelines for amending estimates, and emphasizes the issuance of tax paid statements to nonresident members. The document, accompanied by an instructional second page, also addresses filing deadlines, payment instructions, and the process for electronic submissions, highlighting Maryland's effort to streamline tax compliance for PTEs through the utilization of the 510D Form.

Maryland 510D Sample

FORMMARYLAND

510D

DECLARATION OF ESTIMATED INCOME TAX

Only |

OR FISCAL YEAR BEGINNING |

2012, ENDING |

|

|

|

|

|

|

|

Ink |

Federal employer identification number (9 digits) |

|

|

|

|

|

|

|

|

Black |

|

|

|

|

Name |

|

|

|

|

or |

|

|

|

|

Blue |

|

|

|

|

Number and street |

|

|

|

|

Using |

|

|

|

|

City or town |

|

State |

ZIP code |

|

|

|

|

|

|

Please |

|

|

|

|

|

|

|

|

|

ME

12

12

For Office Use Only

YE |

EC |

EC |

|

|

|

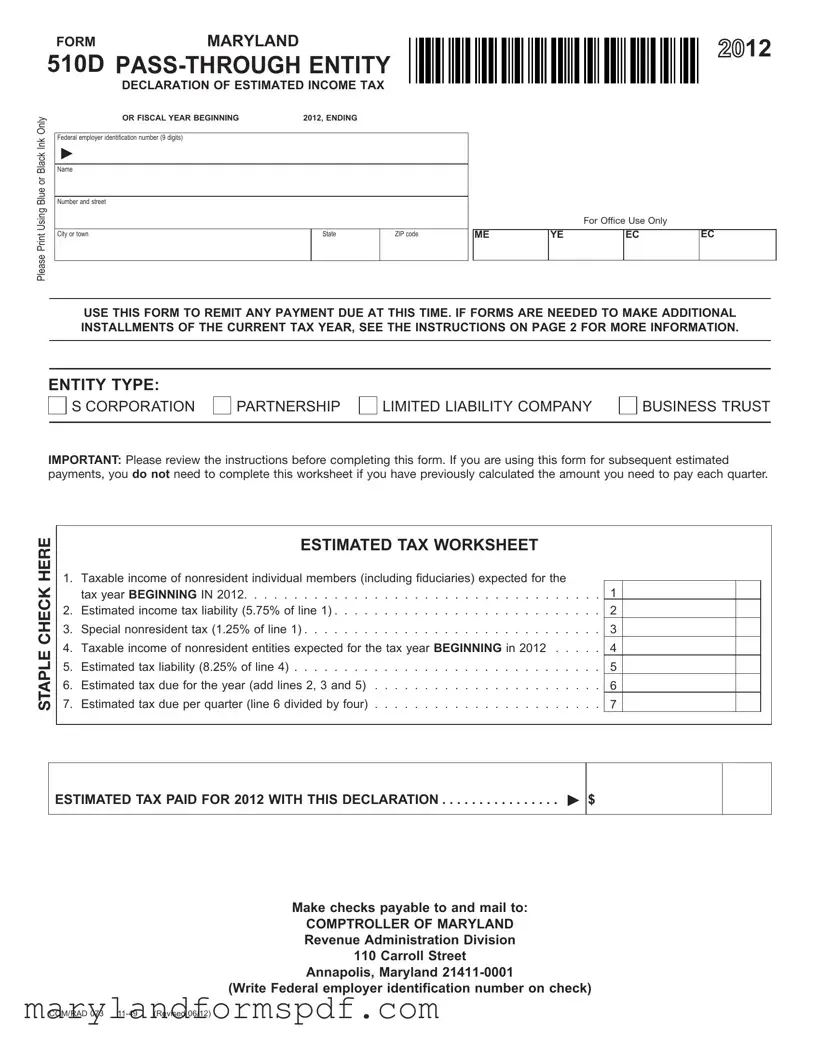

USE THIS FORM TO REMIT ANY PAYMENT DUE AT THIS TIME . IF FORMS ARE NEEDED TO MAKE ADDITIONAL INSTALLMENTS OF THE CURRENT TAX YEAR, SEE THE INSTRUCTIONS ON PAGE 2 FOR MORE INFORMATION .

ENTITY TYPE:

S CORPORATION

PARTNERSHIP

LIMITED LIABILITY COMPANY

BUSINESS TRUST

IMPORTANT: Please review the instructions before completing this form. If you are using this form for subsequent estimated payments, you do not need to complete this worksheet if you have previously calculated the amount you need to pay each quarter.

STAPLE CHECK HERE

ESTIMATED TAX WORKSHEET

1.Taxable income of nonresident individual members (including fiduciaries) expected for the

tax year BEGINNING IN 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1. . BEGINNING in 2011

2.Estimated income tax liability (5.75% of line 1) . . . . . . . . . . . . . . . . . . . . . . . . . . . .2. .

3.Special nonresident tax (1.25% of line 1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3. .

4.Taxable income of nonresident entities expected for the tax year BEGINNING in 2012 . . . . . .4. .

5.Estimated tax liability (8.25% of line 4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5. .

6.Estimated tax due for the year (add lines 2, 3 and 5) . . . . . . . . . . . . . . . . . . . . . . . .6. .

7.Estimated tax due per quarter (line 6 divided by four) . . . . . . . . . . . . . . . . . . . . . . . .7. .

ESTIMATED TAX PAID FOR 2012 WITH THIS DECLARATION |

$ |

|

|

|

|

Make checks payable to and mail to:

COMPTROLLER OF MARYLAND Revenue Administration Division 110 Carroll Street

Annapolis, Maryland

(Write Federal employer identification number on check)

COM/RAD 073

INSTRUCTIONS MARYLAND

FOR |

DECLARATION OF ESTIMATED INCOME TAX |

|

FORM 510D |

||

|

||

2012 |

|

Purpose of Form Form 510D is used by a pass- through entity (PTE) to declare and remit estimated tax.

General Requirements PTEs are required to pay tax on behalf of all nonresident members. For nonresident members that are individuals or nonresident fiduciaries, the tax is 5.75% in addition to the special nonresident tax of 1.25% of the nonresident member’s distributive or pro rata share of income. For nonresident entity members, the tax is 8.25% of the nonresident member’s distributive or pro rata share of income. A nonresident entity is an entity that is not formed under the laws of Maryland; and is not qualified by, or registered with the Department of Assessments and Taxation to do business in Maryland. The amount of tax due may be limited based on the distributable cash flow limitation. The Distributable Cash Flow Limitation worksheet is available in our PTE income tax booklet, which can be downloaded at www . marylandtaxes .com.

Certain PTEs meeting certain reporting requirements are exempt from the requirement to pay nonresident tax on behalf of its nonresident members. See instructions for Form 510 for more information.

When the tax is expected to exceed $1,000 for the tax year, the PTE must make quarterly estimated payments. The total estimated tax payments for the year must be at least 90% of the tax developed for the current tax year or 110% of the tax that was developed for the prior tax year to avoid interest and penalty.

In the case of a short tax period the total estimated tax required is the same as for a regular tax year: 90% of the tax that was developed for the current (short) tax year or 110% of the tax that was developed for the prior tax year. The minimum estimated tax for each of the installment due dates is the total estimated tax required divided by the number of installment due dates occurring during the short tax year. However, if the

Maryland law provides for the accrual of interest and imposition of penalty for failure to pay any tax when due.

If it is necessary to amend the estimate, recalculate the amount of estimated tax required using the estimated tax worksheet provided. Adjust the amount of the next installment to reflect any previous underpayment or overpayment. The remaining installments must be at least 25% of the amended estimated tax due for the year.

The PTE must issue a statement to each nonresident member showing the amount of tax paid on their behalf. Nonresident members must include the statement with their own income tax returns (Form 500, 504, 505 or 510) to claim credit for taxes paid on their behalf.

Tax Rate The current 2012 tax rate for nonresident individual members is 5.75% at the time this form was created. It is possible that the Maryland Legislature may change this tax when in session. Please check our Web site for updates at www .marylandtaxes .com.

When to File File Form 510D on or before the 15th day of the 4th, 6th, 9th and 12th months following the beginning of the tax year or period for S corporations or by the 4th, 6th, 9th and 13th months following the beginning of the tax year for partnerships, LLCs and business trusts.

Tax Year or Period The tax year is shown at the top of Form 510D. The form used for filing must reflect the preprinted tax year in which the PTE’s tax year begins.

If the tax year of the PTE is other than a calendar year, enter the beginning and ending dates of the fiscal year in the space provided at the top of Form 510D.

Name, Address, and Other Information Type or print the required information in the designated area.

Enter the exact PTE name with any “Trading As” (T/A) name if applicable.

Enter the federal employer identification number (FEIN). If the FEIN has not been secured, enter “APPLIED FOR” followed by the date of application. If a FEIN has not been applied for, do so immediately.

Filing electronically using Modernized Electronic Filing method (software provider must be approved by the IRS and Revenue Administration Division). If filed electronically, do not mail 510D; retain it with company’s records .

If you need to make additional payments for the current tax year you may file electronically, or you can go to

www.marylandtaxes .comand download another Form 510D. We have discontinued the use of preprinted quarterly estimated tax vouchers for PTEs.

Payment Instructions Include a check or money order made payable to Comptroller of Maryland. All payments must indicate the FEIN, type of tax and tax year beginning and ending dates. DO NOT SEND CASH.

Mailing Instructions Mail the completed Form 510D and payment to:

Comptroller of Maryland

Revenue Administration Division

110 Carroll Street

Annapolis, MD

COM/RAD 073

File Breakdown

| Fact Name | Detail |

|---|---|

| Purpose and Use | The purpose of Form 510D is for pass-through entities to declare and remit estimated income tax. |

| Governing Law | Form 510D is governed by Maryland state law which requires taxes to be paid on behalf of all nonresident members of pass-through entities. |

| Payment Timelines | Payments must be made quarterly by the 15th day of the 4th, 6th, 9th, and 12th months following the beginning of the tax year for S corporations; for partnerships, LLCs, and business trusts, it's by the 4th, 6th, 9th, and 13th months. |

| Tax Rate Information | For nonresident individual members, the 2012 tax rate at the time of publication is 5.75%, in addition to a special nonresident tax of 1.25%. |

Steps to Filling Out Maryland 510D

Fulfilling your tax responsibilities accurately is crucial for any pass-through entity (PTE) in Maryland. Form 510D helps entities like S corporations, partnerships, limited liability companies, and business trusts declare and pay estimated income tax on behalf of their nonresident members. Properly completing and submitting this form ensures compliance with Maryland tax laws and can help avoid penalties. Here's a step-by-step guide to filling out the Maryland 510D form correctly.

- Begin by determining the fiscal year dates for your entity. Write the beginning and ending dates for the tax year at the top of Form 510D.

- Enter your entity's complete name and address, including the number and street, city or town, state, and ZIP code in the designated sections.

- Clearly provide the entity's Federal Employer Identification Number (FEIN) in the designated space. If you've applied for but not yet received your FEIN, write "APPLIED FOR" and the date of application.

- Choose the type of your entity by marking the appropriate box: S Corporation, Partnership, Limited Liability Company, or Business Trust.

- Move on to the Estimated Tax Worksheet section. Calculate the taxable income of nonresident individual members (including fiduciaries) expected for the tax year. Enter this amount on line 1.

- Calculate the estimated income tax liability, which is 5.75% of the amount on line 1. Write this on line 2.

- Determine the special nonresident tax, which is 1.25% of the amount on line 1, and enter it on line 3.

- If applicable, calculate the taxable income of nonresident entities expected for the tax year and enter it on line 4.

- Compute the estimated tax liability for nonresident entities, which is 8.25% of the amount on line 4. Place this figure on line 5.

- Add the amounts from lines 2, 3, and 5 to find the total estimated tax due for the year. Write this total on line 6.

- Divide the total estimated tax due by four to find the estimated tax due per quarter and enter this on line 7.

- If making a payment with this declaration, write the amount of estimated tax paid for 2012 in the provided space.

- Review the form for accuracy. Make sure all necessary information is complete and correct.

- Prepare a check or money order for the amount due, made payable to Comptroller of Maryland. Write the FEIN on the check or money order.

- Mail the completed Form 510D along with your payment to the Comptroller of Maryland at the address provided: Revenue Administration Division, 110 Carroll Street, Annapolis, MD 21411-0001.

Remember, accuracy and timeliness are key to fulfilling your tax obligations. Ensure all information is correct and submit your Form 510D and any accompanying payments by the due dates to avoid penalties. Keeping accurate records of your submissions is also advisable, helping to streamline any future tax-related processes.

More About Maryland 510D

What is Form 510D used for?

Form 510D is a tax document for pass-through entities (PTEs) in Maryland, such as S corporations, partnerships, limited liability companies, and business trusts. It's used to declare and remit estimated income tax on behalf of all nonresident members of the PTE. This includes paying a specific tax rate on the nonresident member's distributive or pro rata share of income.

Who needs to file Form 510D?

Any Maryland PTE with nonresident members must file Form 510D if the tax expected to be due exceeds $1,000 for the year. This requirement applies to entities that have to pay tax on behalf of individuals or entities that are not residents of Maryland.

When is Form 510D due?

The filing deadlines for Form 510D vary based on the type of entity:

- For S corporations, it's due on the 15th day of the 4th, 6th, 9th, and 12th months following the beginning of the tax year.

- For partnerships, LLCs, and business trusts, it's due on the 15th day of the 4th, 6th, 9th, and 13th months following the beginning of the tax year.

How is the estimated tax calculated?

Estimated tax is calculated based on the taxable income of nonresident individual and entity members expected for the tax year. The rates are:

- 5.75% of taxable income for nonresident individual members, plus a special nonresident tax of 1.25%.

- 8.25% of taxable income for nonresident entity members.

What are the tax rates for nonresident members?

For the 2012 tax year:

- Nonresident individual members are subject to a tax rate of 5.75%, plus a special nonresident tax of 1.25%.

- Nonresident entity members are taxed at a rate of 8.25%.

What happens if the estimated payments are not sufficient?

Insufficient estimated payments can lead to the accrual of interest and penalties. The total estimated tax payments for the year must be at least 90% of the tax for the current tax year or 110% of the tax for the prior tax year to avoid these charges. Adjustments can be made to increase future payments if initial estimates fall short.

How are payments made?

Payments can be made by including a check or money order with the Form 510D when mailed to the Comptroller of Maryland, Revenue Administration Division. Ensure the check includes the federal employer identification number (FEIN), the type of tax, and the tax year's beginning and ending dates. Electronic payments may also be an option; check the state's tax website for specifics.

Can Form 510D be filed electronically?

Yes, Form 510D can be filed electronically using the Modernized Electronic Filing method. Approved software by the IRS and Revenue Administration Division is necessary for electronic filing. When filing electronically, there's no need to mail in Form 510D; instead, retain it with the company’s financial records.

Common mistakes

When completing the Maryland 510D Form for Pass-Through Entity Declaration of Estimated Income Tax, individuals often encounter a few common pitfalls. It’s crucial to address these mistakes to ensure accurate and compliant tax filings.

- Not Reviewing Instructions: Failing to carefully read the instructions included with the form can lead to misunderstandings about how to properly fill out the required fields and calculate tax estimations.

- Incorrect Entity Type Selection: Misidentifying the type of entity (e.g., S corporation, partnership, limited liability company, or business trust) can lead to incorrect tax computations and filings.

- Inaccurate Calculation of Taxable Income: Errors in calculating the taxable income of nonresident individual members or entities can result in under or overestimated tax payments.

- Misapplication of Tax Rates: Applying the wrong tax rate—whether it’s for nonresident individuals or entities—can cause discrepancies in the estimated taxes due.

- Omission of Special Nonresident Tax: Overlooking the additional special nonresident tax required for nonresident members can result in underpayment of estimated taxes.

- Incomplete or Incorrect Details: Not providing complete or accurate name, address, and Federal Employer Identification Number (FEIN) may delay processing or lead to misfiled documents.

- Failure to Amend Estimates: Neglecting to amend estimated payments when financial projections change can result in penalties for underpayment.

- Incorrect Payment Information: Submitting the wrong amount or making the check payable to the incorrect entity can cause delays in crediting payments to the right account.

Becoming acquainted with these common errors and applying diligent attention to detail when completing the Maryland 510D can facilitate smoother processing and avoid unnecessary penalties. It's beneficial to refer to the instructions on the Maryland tax website for the most current information and tax rates.

Documents used along the form

In preparing and managing the tax obligations of pass-through entities in Maryland, especially in regards to the Maryland Form 510D for the Declaration of Estimated Income Tax for Pass-Through Entities, it's crucial to be aware of and understand several other forms and documents that may need to be filed alongside or in addition to Form 510D. These documents aid in ensuring compliance with Maryland's tax laws and help orchestrate the intricate process of tax preparation for such entities.

- Maryland Form 510 - This is the Annual Pass-Through Entity Income Tax Return. It's used by pass-through entities to report their income, gains, losses, deductions, and credits for the year. It complements Form 510D by providing a comprehensive report of the entity's annual financial activities.

- Maryland Form 500 - The Corporation Income Tax Return. While not directly used by pass-through entities themselves for their pass-through operations, this form might be relevant for entities that are part of a larger corporate structure or for assessing the tax implications of their income distribution on their taxable income.

- Maryland Form 504 - Nonresident Income Tax Return. This form is particularly pertinent for nonresident members of Maryland pass-through entities, allowing them to file personal income taxes owed to the state, including distributions received from a pass-through entity.

- Maryland Form 505 - The Nonresident Income Tax Calculation Form is used alongside Form 504. It helps compute the amount of Maryland tax due, based on income derived from Maryland sources, which includes allocations from pass-through entities.

- Maryland Form MW506NRS - Declaration of Estimated Pass-Through Entity Nonresident Income Tax. This form is necessary for remittance of withheld taxes on behalf of nonresident members of the pass-through entity, complementing the process initiated by Form 510D for accurately estimating and remitting taxes due.

Understanding the role and requirements of each of these forms is essential for the proper tax planning and compliance of pass-through entities operating in Maryland. By staying informed about these documents, entities can better navigate the complexities of state tax regulations, avoid common pitfalls, and ensure timely and accurate tax filing. For any assistance or clarification on using these documents, it's advisable to consult with a tax professional who is familiar with Maryland tax laws.

Similar forms

The Maryland 510D form, designated for pass-through entities to declare and remit estimated income tax, mirrors several federal tax documents in its structure and purpose. Such forms include the IRS Form 1040-ES for individuals and the 1065-B form for partnerships. These documents are essential for the accurate and timely payment of estimated taxes, reducing the burden at the end of the fiscal year.

IRS Form 1040-ES is utilized by individuals to report and pay estimated quarterly taxes. Similar to Maryland's 510D form, the 1040-ES facilitates the advance payment of taxes based on the taxpayer's estimated income for the year. Both forms aim to help taxpayers manage their tax liability by spreading payments throughout the year, thus avoiding a large lump sum payment when filing their annual tax return. Additionally, they provide worksheets to calculate the estimated tax owed, ensuring that the taxpayer or entity pays at least 90% of the tax due for the current year or 110% of the prior year's tax, in alignment with federal and state guidelines to avoid penalties.

IRS Form 1065-B is another document that shares similarities with Maryland's 510D form, specifically tailored for partnerships. While 1065-B serves at a federal level to declare income, deductions, gains, losses, etc., for partnerships, the 510D form serves a similar purpose for pass-through entities at the state level in Maryland. Both documents require detailed financial information to ensure that entities appropriately report their income and calculate their tax obligations. The underlying principle uniting the 510D and 1065-B forms is the requirement for entities to make estimated tax payments if they anticipate owing more than a specific amount, reinforcing the practice of proactive financial management and tax compliance.

Dos and Don'ts

When filling out the Maryland 510D form for Pass-Through Entity Declaration of Estimated Income Tax, it's crucial to follow specific guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do when completing this form:

Things You Should Do:

- Review the instructions provided on the second page of the form thoroughly before filling it out.

- Ensure the name of the Pass-Through Entity (PTE) is exactly as registered, including any "Trading As" (T/A) names if applicable.

- Use black or blue ink and print clearly to avoid any confusion or misinterpretation of the information provided.

- Enter the federal employer identification number (FEIN) accurately. If the FEIN has not been secured, notate "APPLIED FOR" and the date of application.

- Calculate the estimated tax due carefully, using the estimated tax worksheet provided in the instructions, to determine the amount payable for each quarter.

- Make checks payable to the Comptroller of Maryland and include the FEIN, type of tax, and the tax year's beginning and ending dates on your payment.

- Retain a copy of the form and any related documentation for the company's records, especially if filing electronically.

Things You Shouldn't Do:

- Do not ignore the specific payment due dates outlined for S corporations, partnerships, limited liability companies, and business trusts.

- Do not overlook the requirement to issue a statement to each nonresident member showing the amount of tax paid on their behalf.

- Do not submit the form without verifying that the estimated payments are at least 90% of the tax developed for the current tax year or 110% of the tax developed for the prior tax year to avoid penalties.

- Do not send cash. Always make payments via check or money order.

- Do not use outdated forms or information. Check the Marylandtaxes.com website for the most current form and tax rate information.

- Do not leave any required fields blank. If a field does not apply, clearly mark it as "N/A" (not applicable).

- Do not mail 510D if filed electronically. However, ensure it's retained with the company’s records.

Misconceptions

There are several misconceptions about the Maryland 510D form, which is used by pass-through entities (PTEs) to declare and remit estimated income tax. Understanding these misconceptions is vital for ensuring compliance and avoiding penalties.

- All entities must file Form 510D: Not all entities are required to file this form. Only pass-through entities, such as S corporations, partnerships, limited liability companies, and business trusts need to file Form 510D for declaring estimated taxes.

- Form 510D is only for nonresident members: While it is true that PTEs must pay tax on behalf of all nonresident members, Form 510D is used to declare estimated taxes for the entity as a whole, not just nonresident members.

- The form is complicated to fill out: Although tax forms can be intimidating, Form 510D comes with instructions that guide you through the calculation of estimated tax payments, making it more manageable.

- Payments are only due annually: Estimated taxes are not paid annually but quarterly. This misconception could lead to missed payments and penalties. The form outlines the specific due dates for these payments.

- Estimated payments are optional: If the total expected tax for the year exceeds $1,000, the PTE is required to make quarterly estimated payments. This is a requirement, not an option, to avoid penalties.

- PTEs must use preprinted vouchers to make payments: Maryland has discontinued the use of preprinted quarterly estimated tax vouchers for PTEs. Payments can now be made electronically or by downloading a form from the website.

- Any mistake requires refiling the entire form: If it's necessary to amend an estimate, you don't need to refile the entire form. Instead, recalculate the estimated tax and adjust the amount of your next installment accordingly.

- Failure to file Form 510D doesn't result in penalties: Maryland law imposes penalties and accrues interest for failure to make estimated tax payments when due. Ignoring the requirement to file and pay can lead to significant financial consequences.

Correcting these misconceptions is crucial for PTEs to fulfill their tax obligations accurately and on time. Remember, when in doubt, reviewing the instructions provided with the form or seeking professional tax advice can help ensure compliance and avoid penalties.

Key takeaways

Understanding and complying with tax requirements is essential for pass-through entities (PTEs) in Maryland. Focusing on the Maryland 510D form, designed for estimating and paying taxes, can make this process smoother. Here are some key takeaways for entities navigating this form:

- Who needs to file: The Maryland 510D form is specifically for pass-through entities, such as S corporations, partnerships, limited liability companies (LLCs), and business trusts. These entities are required to declare and remit estimated income tax for their nonresident members.

- Estimated payments are necessary when: If the total tax expected to be due from a PTE exceeds $1,000 for the tax year, quarterly estimated payments are mandated. This helps ensure that at least 90% of the tax for the current year or 110% of the previous year's tax is covered, thereby avoiding possible interests and penalties for underpayment.

- Calculating your estimated tax: The form includes a worksheet to help calculate taxable income for nonresident individual members and entities, thereby determining the estimated income tax liability and special nonresident tax. It's imperative to accurately forecast income and tax liability to avoid overpayment or underpayment.

- Filing and payment specifics: Filings are due on or before the 15th day of the 4th, 6th, 9th, and 12th months following the beginning of the tax year for S corporations. Meanwhile, partnerships, LLCs, and business trusts have slightly different deadlines—by the 4th, 6th, 9th, and 13th months. Payments should be made to the Comptroller of Maryland, and the entity's federal employer identification number must be included with each payment for proper identification and credit.

Moreover, it's important for pass-through entities to regularly review and, if necessary, amend their estimated tax calculations throughout the year. Adjustments may be required based on actual earnings and distributions. Ensuring that all nonresident members receive a statement of the tax paid on their behalf is also critical, as this allows them to claim credit for these payments on their personal tax returns. Staying informed about any legislative changes to tax rates or filing requirements via the Maryland Comptroller's website is advisable, as tax laws and rates can change.

Common PDF Templates

Maryland Confidential Morbidity Report - Aligns with state health department goals for maintaining high public health standards.

Addendum Meaning Real Estate - Environmental considerations and the presence of hazardous materials are covered, urging buyers to conduct thorough investigations.

Md State Tax Form - If your Maryland corporation is behind on tax prep, file Form 500E to get an extension.