Maryland 510E PDF Template

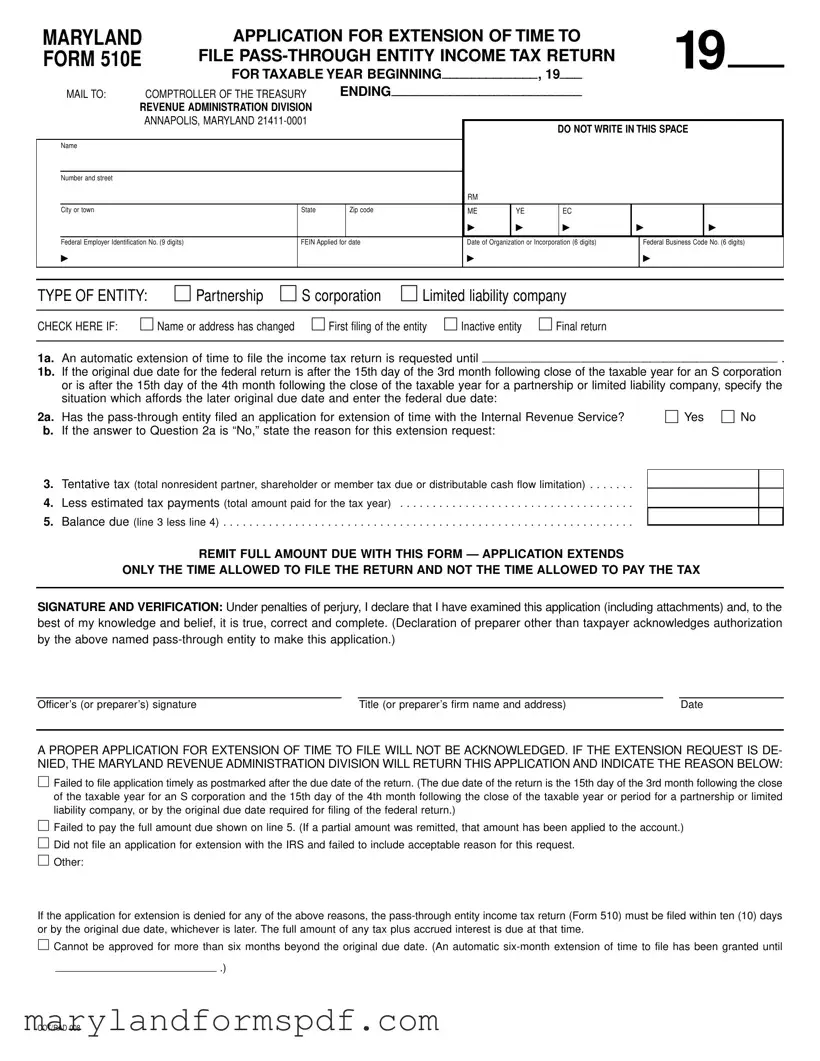

Understanding the intricacies of Maryland's 510E form is crucial for pass-through entities seeking an extension on their income tax return filings. This document, intended for partnerships, S corporations, and limited liability companies, serves as an application to push back the filing deadline. It's important to note that while the form can extend the filing due date, it does not grant additional time to pay any taxes due; this means that accurate estimation and timely payment of taxes are paramount to avoid penalties. Submitted to the Comptroller of the Treasury, Revenue Administration Division in Annapolis, Maryland, the form requires detailed information about the entity, including its name, address, and Federal Employer Identification Number (FEIN). Applicants must indicate whether it's their first filing, if there have been any changes to their name or address, or if the entity has become inactive or is filing a final return. The process involves stating whether an extension has also been requested with the IRS, outlining the tax due, subtracting estimated tax payments made, and calculating any balance due. The form emphasizes the significance of a proper and timely application—highlighting the automatic extensions granted, the conditions under which additional extensions may be considered, and the consequences of a denied request. Compliance with these requirements ensures that pass-through entities remain in good standing while managing their tax obligations.

Maryland 510E Sample

MARYLAND |

APPLICATION FOR EXTENSION OF TIME TO |

|

|

19 |

|

|||||||||||

FORM 510E |

FILE |

|

|

|

||||||||||||

|

|

FOR TAXABLE YEAR BEGINNING_____________, 19___ |

|

|

|

|||||||||||

|

MAIL TO: |

COMPTROLLER OF THE TREASURY |

ENDING__________________________ |

|

|

|

|

|

||||||||

|

REVENUE ADMINISTRATION DIVISION |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

ANNAPOLIS, MARYLAND |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

DO NOT WRITE IN THIS SPACE |

|||||||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Number and street |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RM |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or town |

|

|

State |

|

Zip code |

|

ME |

YE |

|

EC |

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

▶ |

|

▶ |

▶ |

|

▶ |

||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Federal Employer Identification No. (9 digits) |

|

FEIN Applied for date |

|

Date of Organization or Incorporation (6 digits) |

|

Federal Business Code No. (6 digits) |

|||||||||

|

▶ |

|

|

|

|

|

|

▶ |

|

|

|

|

▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||||||||

TYPE OF ENTITY: ☐ Partnership |

☐ S corporation |

☐ Limited liability company |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

||||||||||

CHECK HERE IF: ☐ Name or address has changed ☐ First filing of the entity ☐ Inactive entity |

☐ Final return |

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1a. |

An automatic extension of time to file the income tax return is requested until ____________________________________________ . |

|

1b. |

If the original due date for the federal return is after the 15th day of the 3rd month following close of the taxable year for an S corporation |

|

|

or is after the 15th day of the 4th month following the close of the taxable year for a partnership or limited liability company, specify the |

|

|

situation which affords the later original due date and enter the federal due date: |

|

2a. |

Has the |

☐ Yes ☐ No |

b.If the answer to Question 2a is “No,” state the reason for this extension request:

3.Tentative tax (total nonresident partner, shareholder or member tax due or distributable cash flow limitation) . . . . . . .

4.Less estimated tax payments (total amount paid for the tax year) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5. Balance due (line 3 less line 4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

REMIT FULL AMOUNT DUE WITH THIS FORM — APPLICATION EXTENDS

ONLY THE TIME ALLOWED TO FILE THE RETURN AND NOT THE TIME ALLOWED TO PAY THE TAX

SIGNATURE AND VERIFICATION: Under penalties of perjury, I declare that I have examined this application (including attachments) and, to the best of my knowledge and belief, it is true, correct and complete. (Declaration of preparer other than taxpayer acknowledges authorization by the above named

Officer’s (or preparer’s) signature |

Title (or preparer’s firm name and address) |

Date |

A PROPER APPLICATION FOR EXTENSION OF TIME TO FILE WILL NOT BE ACKNOWLEDGED. IF THE EXTENSION REQUEST IS DE- NIED, THE MARYLAND REVENUE ADMINISTRATION DIVISION WILL RETURN THIS APPLICATION AND INDICATE THE REASON BELOW:

☐Failed to file application timely as postmarked after the due date of the return. (The due date of the return is the 15th day of the 3rd month following the close of the taxable year for an S corporation and the 15th day of the 4th month following the close of the taxable year or period for a partnership or limited liability company, or by the original due date required for filing of the federal return.)

☐Failed to pay the full amount due shown on line 5. (If a partial amount was remitted, that amount has been applied to the account.)

☐Did not file an application for extension with the IRS and failed to include acceptable reason for this request.

☐Other:

If the application for extension is denied for any of the above reasons, the

☐Cannot be approved for more than six months beyond the original due date. (An automatic

___________________________ .)

COT/RAD 008

INSTRUCTIONS FOR MARYLAND FORM 510E (Revised 1999)

APPLICATION FOR EXTENSION OF TIME

TO FILE

INCOME TAX RETURN

GENERAL INSTRUCTIONS

Purpose of Form Form 510E is used by a

General Requirements Maryland law provides for an extension of time to file, but in no case can an extension be granted for more than six months beyond the original due date. A request for exten- sion of time to file will be granted auto- matically for six months for S corporations and three months for partnerships and limited liability companies if:

1)Form 510E is properly filed and submitted by the original due date (S corporation: 15th day of the 3rd month following close of the tax year or period. Partnerships and limited liability companies: 15th day of the 4th month following close of the tax year or period.);

2)full payment of any balance due is submitted with Form 510E; and

3)an application for extension of time has been filed with the Internal Revenue Service or an acceptable reason has been provided with Form 510E.

An additional

A proper application for extension of time to file will not be acknowledged. If the extension request is denied, the

Form 510E does not extend the time allowed a

When and Where to File File Form 510E by the 15th day of the 3rd month following the close of the taxable year or period if an S corporation; by the 15th day of the 4th month following the close of the taxable year or period if a partnership or limited liability company. The return must be filed with the Comptroller of the Treasury, Revenue Administration Division, Annapolis, Maryland

SPECIFIC INSTRUCTIONS

Taxable Year or Period Enter the beginning and ending dates of the tax- able year in the space provided at the top of Form 510E.

Name, Address and Other Information

Type or print the required information in the designated area. DO NOT USE THE LABEL FROM THE TAX BOOKLET COVER.

Enter the exact

Enter the Federal Employer Identifica- tion Number (FEIN). If a FEIN has not been secured, enter “APPLIED FOR” followed by the date of application. If a FEIN has not been applied for, do so immediately.

Be sure to check the applicable box to indicate the type of

Check the applicable box if: (1) the name or address has changed; (2) this is the first filing of the

(3)this is an inactive

Tentative Tax Enter the total amount of income tax liability expected for the tax year on line 3.

Estimated Tax Payments Enter on line 4 the total amounts paid with Form 510D - Declaration of Estimated Pass- Through Entity Nonresident Tax for the taxable year or period.

Balance Due Enter the amount of tax due on line 5 and remit full payment with this form.

Signature and Verification An author- ized officer or the paid preparer must sign and date Form 510E indicating the officer’s title or preparer firm name and address.

Payment Instructions Include a check or money order made payable to the Comptroller of the Treasury for the full amount of any balance due. All payments must indicate the Federal Employer Identi- fication Number, type of tax and tax year beginning and ending dates. DO NOT SEND CASH.

Mailing Instructions Use the enve- lope provided in the tax booklet and place an “X” in the appropriate box in the lower left corner to indicate the type of document enclosed. Also, be sure to read and follow the reminders listed on the back of the envelope.

File Breakdown

| Fact Name | Description |

|---|---|

| Purpose of Form 510E | Used by a pass-through entity to request an extension of time to file the pass-through entity income tax return (Form 510). |

| Maximum Extension Duration | Maryland law limits the extension to no more than six months beyond the original due date. |

| Automatic Extension Criteria | Automatically granted for six months for S corporations and three months for partnerships and limited liability companies if the form is properly filed by the original due date with full payment and an IRS extension application is filed or an acceptable reason is provided. |

| Extension Denial Conditions | The application will be denied if it's postmarked after the due date, if the full amount due is not paid, or if no IRS extension was filed without an acceptable reason. |

| Filing Locations | Form 510E must be filed with the Comptroller of the Treasury, Revenue Administration Division, Annapolis, Maryland. |

| Governing Law | Maryland income tax law governs the requirements for filing, payments, and the imposition of penalties and interest for late payments. |

Steps to Filling Out Maryland 510E

Filing the Maryland 510E form is a necessary step for pass-through entities like partnerships, S corporations, or limited liability companies that need more time to prepare and submit their income tax returns. This form helps request an extension, ensuring entities comply with state tax obligations without rushing through their financial documents. Proper completion and timely submission of this form can prevent penalties or issues with tax filings. Here's how to fill it out:

- Identify the taxable year's beginning and ending dates at the top of the form, in the spaces provided.

- Clearly type or print the pass-through entity's name, address, city or town, state, and zip code in the designated area. Do not use the label from the tax booklet cover.

- Enter the Federal Employer Identification Number (FEIN) in the provided space. If the FEIN has been applied for but not received, write "APPLIED FOR" and include the date of the application.

- Select the type of entity by checking the appropriate box: Partnership, S corporation, or Limited liability company.

- Check the appropriate box if there has been a change in name or address, if it's the first filing, if the entity is inactive, or if it's the final return.

- Under "Signature and Verification," an authorized officer or the tax preparer must sign and date the form, indicating their title or the preparer’s firm name and address.

- For line 1a, enter the date until which an extension is requested.

- If applicable, specify in 1b the reason the federal return due date allows for a later filing and enter the federal due date.

- Answer question 2a regarding whether the entity has filed for a federal extension, and if not, provide a reason in 2b.

- Calculate the tentative tax due (total nonresident partner, shareholder, or member tax due or distributable cash flow limitation) and enter it on line 3.

- Enter the total estimated tax payments made for the tax year on line 4.

- Subtract line 4 from line 3 and enter the balance due on line 5. Include full payment of this amount when submitting the form.

Payment Instructions: Make a check or money order payable to the Comptroller of the Treasury for any balance due. Ensure the Federal Employer Identification Number, the type of tax, and the tax year beginning and ending dates are indicated on the payment. Do not send cash.

Mailing Instructions: Use the provided envelope in the tax booklet, placing an "X" in the appropriate box in the lower left corner to indicate the type of document enclosed. Follow any additional reminders listed on the back of the envelope to ensure proper submission.

More About Maryland 510E

What is the purpose of the Maryland 510E form?

The Maryland 510E form is designed for use by pass-through entities such as partnerships, S corporations, and limited liability companies to request an extension of time to file their pass-through entity income tax return (Form 510). It is important to note that this form extends only the filing deadline, not the deadline for tax payment.

Who needs to file a Maryland 510E form?

Any pass-through entity, including partnerships, S corporations, and limited liability companies, that needs more time to prepare their Maryland income tax return must file a Maryland 510E form. The requirement applies if the entity cannot file by the original deadline due to various reasons.

When is the Maryland 510E form due?

The due date for filing the Maryland 510E form depends on the type of pass-through entity:

- For an S corporation, the form should be filed by the 15th day of the 3rd month following the close of the taxable year or period.

- For partnerships and limited liability companies, the due date is the 15th day of the 4th month following the close of the taxable year or period.

How does an entity file for an extension using Form 510E, and what information is needed?

To file for an extension using Form 510E, the entity must:

- Complete the form with the beginning and ending dates of the taxable year, name and address of the entity, Federal Employer Identification Number (FEIN), and the type of entity.

- Specify the length of the extension being requested.

- Indicate whether an application for an extension of time has been filed with the Internal Revenue Service.

- Calculate and enter any tentative tax due along with estimated tax payments already made.

- Sign and date the form, providing the preparer’s information if applicable.

- Submit the form to the Comptroller of the Treasury, Revenue Administration Division in Annapolis, Maryland, by the due date along with full payment of any balance due.

What happens if the Maryland 510E form is denied?

If the extension request is denied due to reasons such as not filing the application on time, failing to pay the full amount due, not filing an application for an extension with the IRS without an acceptable reason, or other issues, the pass-through entity will be notified. The pass-through entity must then file Form 510 within ten days or by the original due date, whichever is later. At this point, the full amount of any tax plus accrued interest becomes due.

Are there penalties for not filing or paying taxes on time even if an extension is granted?

Yes, while Form 510E extends the deadline to file the income tax return, it does not extend the deadline to pay taxes. Entities are still required to estimate and pay any tax due with their extension request. Failure to pay taxes by the original due date will result in the accrual of interest and possible imposition of penalties on the unpaid tax amount.

Common mistakes

Completing the Maryland 510E form, which is the Application for Extension of Time to File Pass-Through Entity Income Tax Return, is a critical process for many businesses. A misstep in this process can lead to unwanted delays, penalties, or even the rejection of the extension request. Here, we outline four common mistakes that are made during this process:

Incorrect or Incomplete Information: The basics can sometimes trip people up. For instance, if the Federal Employer Identification Number (FEIN) is not correctly entered—such as missing or transposing numbers—or if the entity type is not correctly checked, it can lead to the application being processed incorrectly or not at all. Moreover, if a FEIN has been applied for but not yet received, stating "APPLIED FOR" followed by the date is essential. Ensuring accuracy in these areas is paramount.

Filing Under the Wrong Entity Type: The form provides options to identify as a Partnership, S Corporation, or Limited Liability Company. Mistakes occur when the person filling out the form does not properly identify the legal structure of their entity or misunderstands the definitions of these categories. This misunderstanding can lead to incorrect processing times and requirements, as the deadlines and obligations can vary considerably among different entity types.

Failure to Indicate Changes: If there have been any changes in name or address, or if it's the first filing of the entity, this needs to be indicated on the form. Likewise, indicating whether the entity is inactive or filing a final return is crucial. Neglecting to check the appropriate box can lead to confusion and miscommunication, potentially causing the entity to miss important notices about tax obligations.

Not Enclosing the Correct Payment: The extension application extends the filing deadline, not the payment deadline. Therefore, the estimated tax due must be paid with the extension request. A common error is not including the check or money order for the balance due, or miscalculating the amount. Such an oversight can result in the denial of the extension request and the accrual of interest and penalties on the unpaid tax.

When filling out the Maryland 510E form, attention to detail is crucial. Given that the purpose of this form is to request more time to gather comprehensive and accurate information to fulfill tax obligations, it's paradoxical that errors in completing this form can lead to more administrative and financial headaches. Thus, double-checking every entry, ensuring all necessary documentation is attached, and verifying the correct amount of payment included can safeguard against these common pitfalls.

Documents used along the form

When handling tax-related matters in Maryland, specifically for pass-through entities like S corporations, partnerships, and limited liability companies, it's not uncommon to need additional documentation along with the Maryland Form 510E. This application for extension of time to file the pass-through entity income tax return is just a part of the extensive documentation required for comprehensive tax compliance. Here are several important documents and forms often used in conjunction with Form 510E:

- Form 510: The Maryland Pass-Through Entity Income Tax Return is the primary document for reporting the income, deductions, and tax liability of pass-through entities. If an extension is granted via Form 510E, this form will be filed at a later date, accounting for the entity’s financial activities throughout the fiscal year.

- Form 510D: Known as the Declaration of Estimated Pass-Through Entity Nonresident Tax, this form is used to declare and pay estimated tax on income derived from Maryland sources that is attributable to nonresident members of the entity. It helps in managing tax obligations throughout the year and is essential for entities with nonresident members.

- Form MW506NRS: This is the Return of Income Tax Withholding for Nonresident Sale of Real Property. While not applicable to every pass-through entity, entities that deal with real estate transactions involving nonresidents must withhold and submit taxes due on these transactions using this form.

- Form 1: The Maryland Personal Property Return is necessary for limited liability companies and partnerships that own, lease, or use personal property located in Maryland or maintain a trader's license with a local unit of government within the state. Though it pertains more to property than income tax, it's a common form for businesses operating in Maryland.

- Form CRA: Combined Registration Application for business owners wishing to obtain a tax identification number, register for certain tax accounts, or register a new business with the Comptroller of Maryland. It is a foundational document for new or restructured pass-through entities preparing to conduct business in Maryland.

Each of these documents serves a unique purpose in the realm of tax preparation and compliance for pass-through entities in Maryland. From declaring estimated taxes to reporting income, these forms ensure that entities can accurately fulfill their tax obligations while taking advantage of the extension provided by Form 510E. Understanding how and when to effectively use these documents can significantly ease the process of tax preparation for businesses and their consultants.

Similar forms

The Maryland 510E form is similar to IRS Form 7004, which is the Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns. Both forms serve the purpose of requesting additional time to file income tax returns for entities. Specifically, the Maryland 510E form is used by pass-through entities such as partnerships, S corporations, and limited liability companies operating within Maryland. These entities use the form to request an extension for filing their pass-through entity income tax return. Similarly, IRS Form 7004 is utilized by a broad range of business entities, including partnerships, S corporations, and regular corporations, to request an extension of time to file their federal business income tax returns. Both forms require basic information about the entity, such as the name, address, and identification number, and detail the length of the extension being requested. However, the key difference lies in their jurisdiction; the Maryland 510E applies to state tax obligations in Maryland, whereas Form 7004 applies to federal tax obligations.

Another document that shares similarities with the Maryland 510E form is the IRS Form 4868, the Application for Automatic Extension of Time to File U.S. Individual Income Tax Return. Though Form 4868 is designated for individuals and not entities, the primary purpose is similar — to request additional time to file an income tax return. Form 4868 is used by individuals who need more time to file their personal income tax returns, which is comparable to how the Maryland 510E form is used by pass-through entities looking for more time to file their tax returns. Both forms are essentially requests for extensions and do not extend the time to pay any taxes due. They emphasize that while filers can obtain additional time to submit their returns, any owed taxes are still due by the original filing deadline to avoid penalties and interest. The significant difference between the two forms is their intended users: Form 4868 is for individual filers at the federal level, and the Maryland 510E form caters to pass-through entities needing extension for state tax filing in Maryland.

Dos and Don'ts

When filling out the Maryland 510E form, which is an application for extension of time to file the Pass-Through Entity Income tax return, there are several important do's and don'ts to keep in mind to ensure the process goes smoothly. Following these guidelines will help avoid common pitfalls and ensure that your extension request is processed efficiently by the Comptroller of the Treasury, Revenue Administration Division in Annapolis, Maryland.

Do's:

- Fill out the form on time: Make sure to submit Form 510E by the 15th day of the 3rd month following the close of the taxable year for S corporations, or by the 15th day of the 4th month following the close of the taxable year for partnerships and limited liability companies.

- Ensure accuracy: Double-check all the information provided on the form, including the Federal Employer Identification Number (FEIN) and the start and end dates of the taxable year, to ensure accuracy.

- Provide complete payment: If there is a balance due, include a check or money order for the full amount with the form to avoid penalties.

- Check the appropriate boxes: Clearly indicate the type of pass-through entity and mark any applicable boxes, such as if there has been a change in name or address, or if it is the first filing for the entity.

- Sign and date the form: The form must be signed and dated by an authorized officer or the paid preparer, indicating the officer’s title or preparer firm name and address.

- File an IRS extension if applicable: If an extension of time to file has also been requested with the Internal Revenue Service, make sure to indicate this on the form.

Don'ts:

- Wait until the last minute: Filing close to the deadline leaves little room for correcting mistakes and can lead to your extension request being denied due to late submission.

- Leave fields blank: Incomplete forms are more likely to be rejected. Provide all the requested information and write "N/A" in sections that do not apply to your situation.

- Forget to include payment for the balance due: Not including the required payment with your application extends only the time to file, not the time to pay any tax due.

- Use incorrect or outdated contact information: Ensure that the name, address, and FEIN on your form are current and correct.

- Ignore IRS requirements: The state extension does not replace the federal extension. If applicable, make sure you've also filed an extension request with the IRS.

- Miss sending required attachments: If additional documentation or attachments are needed to support your extension request, make sure to include them with your Form 510E.

By following these do's and don'ts, you can help ensure that your Maryland 510E Form is filled out correctly and submitted on time, reducing the chances of delays or issues with your extension request.

Misconceptions

Understanding the intricacies of tax forms can be daunting, especially when dealing with specific forms like the Maryland 510E, which is an Application for Extension of Time to File Pass-Through Entity Income Tax Return. Here are seven common misconceptions about this form, explained in a way to help demystify the process.

Extensions grant more time to pay taxes owed: A major misunderstanding is that filing a Form 510E gives you more time to pay the tax due. This extension only grants additional time to file the necessary paperwork, not an extension to pay any taxes that may be owed. Payment is still expected by the original due date to avoid penalties and interest.

Filing the form is complex: While tax forms can appear complicated, the 510E is straightforward in its purpose — to request more time to file your return. The key is ensuring all information is accurate, including the federal employer identification number and the beginning and ending dates of the tax year.

Automatic approval of extensions: It's commonly thought that submitting Form 510E guarantees an extension. However, the extension can be denied for reasons such as not filing the application timely or failing to pay the full amount due with the form.

Only partnerships can file this form: Another misconception is that the Form 510E is exclusively for partnerships. In truth, S corporations and limited liability companies can also use this form to request an extension.

No need to file if you've paid your taxes: Some believe if they've paid all taxes due, filing Form 510E isn't necessary. However, if you need more time to file, this form must be submitted regardless of your tax payment status, to avoid penalties for late filing.

Form 510E extends the time for all tax payments: This belief is incorrect. The 510E specifically extends the filing deadline for pass-through entity income tax returns. It does not extend the time to pay personal income tax for nonresident partners, shareholders, or members, which remains due by the original deadline.

Electronically filing the Form 510E is not an option: With the move towards digital for many tax-related tasks, it’s a common false assumption that the Maryland 510E cannot be submitted electronically. Checking the specific requirements and updates from the Maryland Comptroller's Office is crucial, as electronic submission options may be available and can simplify the process.

Understanding these common misconceptions can help ensure that filing the Maryland 510E form is as straightforward and error-free as possible, resulting in a smoother experience during tax season.

Key takeaways

- The Maryland Form 510E is designed for pass-through entities like S corporations, partnerships, and limited liability companies to request an extra time for filing their income tax returns.

- Entities must file Form 510E by the original due date: the 15th day of the 3rd month following the end of the taxable year for S corporations, and the 15th day of the 4th month for partnerships and limited liability companies.

- An automatic six-month extension can be granted to S corporations, whereas partnerships and limited liability companies are initially granted a three-month extension, with the possibility of an additional three months for reasonable causes.

- Full payment of any tax due must accompany the Form 510E to avoid the accrual of interest and penalty charges, highlighting that the extension applies only to filing, not to payment deadlines.

- It is imperative to check the appropriate box to indicate the entity type (partnership, S corporation, or limited liability company) and mark any applicable scenarios such as name or address change, first filing, inactivity, or the final return of the entity.

- The form requires the provision of key information such as the beginning and ending dates of the taxable year, the entity's name and address, Federal Employer Identification Number (FEIN), and the Federal Business Code Number.

- If a pass-through entity hasn't applied for a Federal Employer Identification Number (FEIN), the application must be promptly completed. If already applied for but not received, the form allows space to indicate this status.

- To compute the balance due or refund, entities must report the total estimated tax payments made throughout the year and the tentative tax due, calculated based on the nonresident partner, shareholder, or member tax due or distributable cash flow limitation.

- Payment instructions specify that checks or money orders should be made payable to the Comptroller of the Treasury, with clear indications of the FEIN, type of tax, and the tax year's beginning and ending dates.

- The application for an extension with the IRS is a separate process and entities are encouraged to file an extension request with both the IRS and the state of Maryland. If an extension has not been filed with the IRS, a viable reason for requesting an extension from Maryland must be provided.

- A properly filed Form 510E will not be acknowledged; however, if denied, the entity will receive the returned application indicating the reason for denial, which may include late filing, incomplete payment, or failure to seek IRS extension without an acceptable reason.

Common PDF Templates

What Does Claim Exemption From Withholding Mean - The Maryland W4 form, designed for state government employees, aids in determining state income tax withholding.

Mountains in Maryland - It's designed to streamline the process of making early withdrawals or transfers from your retirement account.