Maryland Cof 85 PDF Template

Navigating the compliance landscape for nonprofits in Maryland requires familiarizing oneself with crucial forms such as the Maryland COF-85. Dictated by the Secretary of State of Maryland, this form serves as a pillar for organizations not filing the standard Form 990, ensuring that their financial activities remain transparent and accountable. The depth of the COF-85 form is notable, encompassing various key aspects of an organization's financial health, including revenues, expenses, and changes in net assets or fund balances. It meticulously breaks down sources of income, from donations and grants to program service revenue and membership dues, alongside expenses across program services, management, and fundraising efforts. Furthermore, it requires detailed reporting on balance sheets, functional expenses, and program service revenues, offering a comprehensive snapshot of an organization's fiscal operations. The form also extends to listing officers, directors, and trustees, shedding light on the governance structure behind the fiscal numbers. With penalties for perjury in cases of misinformation, the form underscores the importance of accuracy and completeness in disclosing financial information, exemplifying the state's commitment to financial transparency within the nonprofit sector.

Maryland Cof 85 Sample

Form

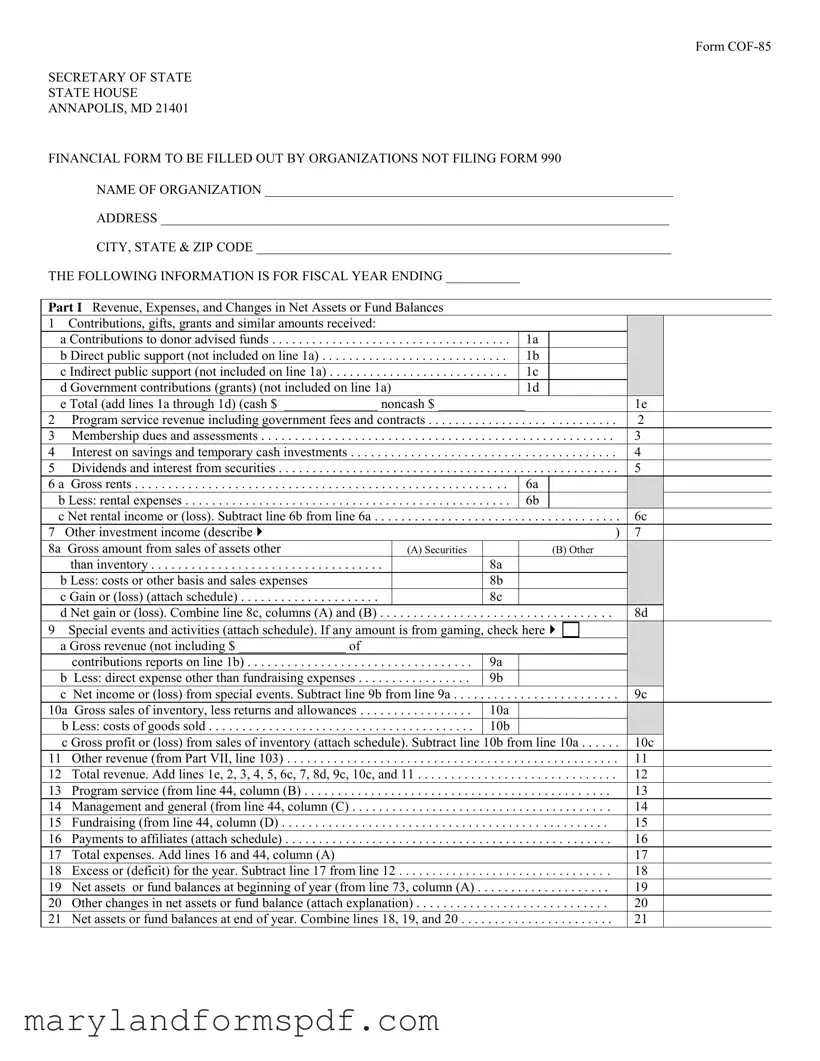

SECRETARY OF STATE

STATE HOUSE

ANNAPOLIS, MD 21401

FINANCIAL FORM TO BE FILLED OUT BY ORGANIZATIONS NOT FILING FORM 990

NAME OF ORGANIZATION _____________________________________________________________

ADDRESS ____________________________________________________________________________

CITY, STATE & ZIP CODE ______________________________________________________________

THE FOLLOWING INFORMATION IS FOR FISCAL YEAR ENDING ___________

Part I Revenue, Expenses, and Changes in Net Assets or Fund Balances

1 Contributions, gifts, grants and similar amounts received: |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||

a Contributions to donor advised funds |

. . . . . . . . . . . . |

. . . . |

1a |

|

|

|

|

|

|

|

||

b Direct public support (not included on line 1a) |

. . . . |

1b |

|

|

|

|

|

|

|

|||

c Indirect public support (not included on line 1a) |

. . . . |

1c |

|

|

|

|

|

|

|

|||

d Government contributions (grants) (not included on line 1a) |

|

|

1d |

|

|

|

|

|

|

|

||

e Total (add lines 1a through 1d) (cash $ ______________ noncash $ _____________ |

|

|

|

|

1e |

|

||||||

2 Program service revenue including government fees and contracts |

. . . . . |

. . . . |

. . |

. . |

. . . . . . |

2 |

|

|

||||

3 Membership dues and assessments |

. . . . . . . . . . . . |

. . . . . |

. . . . |

. . |

. . . |

. . . . . |

3 |

|

|

|||

4 Interest on savings and temporary cash investments |

. . . . . . |

. . . . |

. . |

. . |

. . . . . . |

4 |

|

|

||||

5 Dividends and interest from securities |

. . . . . . . . . . . . |

. . . . . |

. . . . . |

. . |

. . |

. . . . . . |

5 |

|

|

|||

6 a |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Gross rents |

. . . . |

6a |

|

|

|

|

|

|

|

||

b Less: rental expenses |

. . . . . . . . . . . . |

. . . . |

6b |

|

|

|

|

|

|

|

||

c Net rental income or (loss). Subtract line 6b from line 6a |

. . . . . . . . . . . . |

. . . . . |

. . . . . |

. . |

. . |

. . . . . . |

6c |

|

||||

7 Other investment income (describe |

|

) |

7 |

|

|

|||||||

8a |

Gross amount from sales of assets other |

|

(A) Securities |

|

|

(B) Other |

|

|

|

|

||

|

than inventory |

|

|

8a |

|

|

|

|

|

|

|

|

b Less: costs or other basis and sales expenses |

|

|

8b |

|

|

|

|

|

|

|

||

c Gain or (loss) (attach schedule) |

|

|

8c |

|

|

|

|

|

|

|

||

d Net gain or (loss). Combine line 8c, columns (A) and (B) . . |

. . |

. . . . . . . . . . . . |

. . . . . |

. . . . . |

. . |

. . |

. . . . . |

8d |

|

|||

9 |

Special events and activities (attach schedule). If any amount is from gaming, check here |

|

|

|

|

|

|

|||||

a Gross revenue (not including $ ________________ of |

|

|

|

|

|

|

|

|

|

|

||

|

contributions reports on line 1b) |

. . . . . . . . . . |

9a |

|

|

|

|

|

|

|

||

b |

Less: direct expense other than fundraising expenses |

9b |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

||||

c |

Net income or (loss) from special events. Subtract line 9b from line 9a |

. . . . . |

. . . . . |

. . |

. . |

. . . . . . |

9c |

|

||||

10a |

. . . . . . .Gross sales of inventory, less returns and allowances |

. . . . . . . . . . |

10a |

|

|

|

|

|

|

|

||

b Less: costs of goods sold |

10b |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

||||||

c Gross profit or (loss) from sales of inventory (attach schedule). Subtract line |

10b from line 10a |

10c |

|

|||||||||

11 |

Other revenue (from Part VII, line 103) |

. . . . . . . . . . . . |

. . . . . |

. . . . . |

. . |

. . |

. . . . . . |

11 |

|

|

||

12 |

Total revenue. Add lines 1e, 2, 3, 4, 5, 6c, 7, 8d, 9c, 10c, and 11 |

. . . . . . |

. . . . |

. . |

. . |

. . . . . . |

12 |

|

|

|||

13 |

Program service (from line 44, column (B) |

. . . . . . |

. . . . |

. . |

. . . |

. . . . |

13 |

|

|

|||

14 |

Management and general (from line 44, column (C) |

. . . . . |

. . . . . |

. . |

. . |

. . . . . |

14 |

|

|

|||

15 |

Fundraising (from line 44, column (D) |

. . . . . . |

. . . . |

. . |

. . . |

. . . . |

15 |

|

|

|||

16 |

Payments to affiliates (attach schedule) |

. . . . . |

. . |

. . |

. . . . . |

16 |

|

|

||||

17 |

Total expenses. Add lines 16 and 44, column (A) |

|

|

|

|

|

|

17 |

|

|

||

18 |

Excess or (deficit) for the year. Subtract line 17 from line 12 |

. . . . . |

. . . . . |

. . |

. . |

. . . . . |

18 |

|

|

|||

19 |

Net assets or fund balances at beginning of year (from line 73, column (A) . |

. . . . . . |

. . . . |

. . |

. . . |

. . . . |

19 |

|

|

|||

20 |

Other changes in net assets or fund balance (attach explanation) |

. . . . . . |

. . . . |

. . |

. . . |

. . . . |

20 |

|

|

|||

21 |

Net assets or fund balances at end of year. Combine lines 18, 19, and 20 . . . . |

. . . . . |

. . . . . |

. . |

. . |

. . . . . |

21 |

|

|

|||

|

|

|

|

|

Page 2 |

PART II STATEMENT OF FUNCTIONAL EXPENSES |

|

|

|

|

|

|

|

|

|

|

|

Do not include amounts reported on lines |

(A) Total |

(B) Program |

(C) Management |

(D) |

|

6(b), 8(b), 9(b), 10(b), or 16 of Part 1. |

|

services |

and general |

Fundraising |

|

22 |

Grants and allocations (attach schedule) |

|

|

|

|

23 |

Specific assistance to individuals |

|

|

|

|

24 |

Benefits paid to or for members |

|

|

|

|

25 |

Compensation of officers, directors, etc |

|

|

|

|

26 |

Other salaries and wages |

|

|

|

|

27 |

Pension plan contributions |

|

|

|

|

28 |

Other employee benefits |

|

|

|

|

29 |

Payroll taxes |

|

|

|

|

30 |

Professional fundraising fees |

|

|

|

|

31 |

Accounting fees |

|

|

|

|

32 |

Legal fees |

|

|

|

|

33 |

Supplies |

|

|

|

|

34 |

Telephone |

|

|

|

|

35 |

Postage and shipping |

|

|

|

|

36 |

Occupancy |

|

|

|

|

37 |

Equipment rental and maintenance |

|

|

|

|

38 |

Printing and publications |

|

|

|

|

39 |

Travel |

|

|

|

|

40 |

Conferences, conventions and meetings |

|

|

|

|

41 |

Interest |

|

|

|

|

42 Depreciation, depletion, etc. (attach schedule) |

|

|

|

|

|

43 |

Other expenses (itemize): (a) |

|

|

|

|

|

(b) |

|

|

|

|

|

(c) |

|

|

|

|

|

(d) |

|

|

|

|

|

(e) |

|

|

|

|

|

(f) |

|

|

|

|

44 |

Total functional expenses (add lines 22 through 43) |

|

|

|

|

PART III STATEMENT OF PROGRAM SERVICES RENDERED |

|

|

|

||

List each program service title on lines (a) through (d); for each, identify the service output(s) or Product(s) and report the quantity provided. Enter the total expenses attributable to each program service and the amount of grants and allocations included in that total.

(a)__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

(Grants and allocations $ |

) |

(b)__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

(Grants and allocations $ |

) |

(c)__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

(Grants and allocations $ |

) |

(d)__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

|

(Grants and allocations $ |

) |

(e) Other program service activities (attach schedule) |

(Grants and allocations $ |

) |

(f) Total (add lines (a) through (3)) (should equal line 44(B)) |

|

|

|

|

|

|

|

|

|

|

Page 3 |

|

PART IV PROGRAM SERVICE REVENUE AND OTHER REVENUE (STATE NATURE) |

|

Program |

|

Other |

|||||

|

|

|

|

|

|

service revenue |

|

revenue |

|

(a) Fees from government agencies |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

. . . . . . . . . . . |

|

|

|

|

||

(b) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

. . . . . . . . . . . |

|

|

|

|

||

(c) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . |

|

|

|

|

|

(d) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . |

|

|

|

|

|

(e) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . |

|

|

|

|

|

(f) Total program service revenue (enter here and on line 2) |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . |

|

|

|

|

|||

(g) Total other revenue (enter here and on line 11) |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . |

|

|

|

|

|||

PART V BALANCE SHEETS |

If line 12, Part 1, and line 59 are $25,000 or less, you should complete only lines 59, 66, and 74 and, if you do not |

||||||||

Use fund accounting, line 73. If line 12 or line 59 is more than $25,000, complete the entire balance sheet. |

|||||||||

|

|

||||||||

Note: Columns (C) and (D) are optional. Columns (A) and (B) must be |

(A) Beginning of |

|

|

End of year |

|

|

|||

completed to the extent applicable. Where required, attach schedules should be |

(B) Total |

|

(C) Unrestricted/ |

|

(D) Restricted/ |

||||

year |

|

|

|||||||

for |

|

|

|

Expendable |

|

Nonexpendable |

|||

|

|

|

|

|

|||||

|

Assets |

|

|

|

|

|

|

|

|

45 |

Cash — |

|

|

|

|

|

|

||

46 |

Savings and temporary cash investments |

|

|

|

|

|

|

||

47 |

Accounts receivable _______ |

|

|

|

|

|

|

|

|

|

minus allowance for doubtful accounts ____________ |

|

|

|

|

|

|

||

48 |

Pledges receivable ________ |

|

|

|

|

|

|

|

|

|

minus allowance for doubtful accounts ____________ |

|

|

|

|

|

|

||

49 |

Grants receivable |

|

|

|

|

|

|

||

50 |

Receivable due from officers, directors, trustees and key |

|

|

|

|

|

|

||

|

employees (attach schedule) |

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

51 |

Other notes and loans receivable ____________ |

|

|

|

|

|

|

||

|

minus allowance for doubtful accounts ____________ |

|

|

|

|

|

|

||

52 |

Inventories for sale or use |

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

53 |

Prepaid expenses and deferred charges |

|

|

|

|

|

|

||

54 |

Investments — securities (attach schedule) |

|

|

|

|

|

|

||

55 |

Investments — land, buildings and equipment: basis ____ |

|

|

|

|

|

|

||

|

minus allowance for doubtful accounts ____________ |

|

|

|

|

|

|

||

56 |

Investments — other (attach schedule) |

|

|

|

|

|

|

||

57 |

Land, buildings and equipment: basis _________ |

|

|

|

|

|

|

||

|

minus accumulated depreciation ______ (attach schedule) |

|

|

|

|

|

|

||

58 |

Other assets _____________ |

|

|

|

|

|

|

|

|

59 |

Total assets (add lines 45 through 58) |

|

|

|

|

|

|

||

|

Liabilities |

|

|

|

|

|

|

|

|

60 |

Accounts payable and accrued expenses |

|

|

|

|

|

|

||

61 |

Grants payable |

|

|

|

|

|

|

||

62 |

Support and revenue designated for future periods |

|

|

|

|

|

|

||

|

(attach schedule) |

|

|

|

|

|

|

||

63 |

Loans from officers, directors, trustees, and key employees |

|

|

|

|

|

|

||

|

(attach schedule) |

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

64 |

Mortgages and other notes payable (attach schedule) |

|

|

|

|

|

|

||

65 |

Other liabilities ___________ |

|

|

|

|

|

|

|

|

66 |

Total liabilities (add lines 60 through 65) |

|

|

|

|

|

|

||

|

Fund Balances or Net Worth |

|

|

|

|

|

|

||

Organizations that use fund accounting, check here |

|

|

|

|

|

|

|||

and complete lines 67 through 70 and lines 74 and 75. |

|

|

|

|

|

|

|||

67 a. Current unrestricted fund |

|

|

|

|

|

|

|||

|

b. Current restricted fund |

. . . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

68 |

Land, buildings and equipment fund |

|

|

|

|

|

|

||

69 |

Endowment fund |

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

70 |

Other funds (Describe _________ ) |

|

|

|

|

|

|

||

Organizations that do not use fund accounting, check here |

|

|

|

|

|

|

|||

and complete lines 71 through 75. |

|

|

|

|

|

|

|

||

71 |

Capital stock or trust principal |

|

|

|

|

|

|

||

72 |

|

|

|

|

|

|

|||

73 |

Retained earnings or accumulated income |

|

|

|

|

|

|

||

74 |

Total fund balances or new worth |

|

|

|

|

|

|

||

75 |

Total liabilities and fund balances/net worth |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

Page 4 |

|

|

PART VI LIST OF OFFICERS, DIRECTORS & TRUSTEES (LIST OFFICER, DIRECTOR & TRUSTEE WHETHER |

|||||||

|

COMPENSATED OR NOT) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NAME AND ADDRESS |

TITLE & AVERAGE |

COMPENSATION |

|

|

EMPLOYEE |

||

|

|

HOURS PER WEEK |

(if any) |

|

|

BENEFITS |

||

|

|

DEVOTED TO |

|

|

|

|

|

|

|

|

POSITION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

PART VII COMPENSATION OF FIVE HIGHEST PAID PERSONS FOR PROFESSIONAL SERVICES |

|

|

|||||

|

|

|

|

|

|

|

||

|

NAME AND ADDRESS OF PERSONS PAID MORE THAN $30,000 |

|

TYPE OF SERVICE |

|

COMPENSATION |

|||

|

|

|

|

|

|

|

PAID |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL NUMBER OF OTHERS RECEIVING OVER $30,000 for professional services . . . . . . . . . . . . . . _____________________

76 Have any changes been made in the organizing or governing documents? Yes ____ No ____

If yes, attach a copy of the changes.

77 Is the organization related (other than by association with a statewide or nationwide organization) through common membership, governing bodies, trustees, officers, etc., to any other exempt or nonexempt organization? Yes ____ No ____

78 Did your organization receive donated services or the use of materials, equipment or facilities at no charge or at substantially less than fair rental value? Yes ____ No ____

79 The financial books are in the care of _________________________________________________________________________

Located at ______________________________________________________________________________________________

Telephone number ________________________________________________________________________________________

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

UNDER THE PENALTIES OF PERJURY, I DECLARE THAT I HAVE EXAMINED THIS REPORT, INCLUDING ACCOMPANYING STATEMENTS AND TO THE BEST OF MY KNOWLEDGE AND BELIEF IT IS TRUE, CORRECT AND COMPLETE.

Name of Officer __________________________________________________ Date ________________ Title ____________

Signature of Officer _____________________________________________________________________________________

File Breakdown

| Fact | Detail |

|---|---|

| Governing Law | The Maryland COF-85 form is governed by Maryland state law, specifically under the jurisdiction of the Secretary of State, emphasizing its state-specific nature and requirements. |

| Purpose | Designed for organizations not filing Form 990 with the IRS, it serves as a financial reporting tool, ensuring transparency and accountability for entities operating within Maryland. |

| Main Components | The form includes detailed sections on revenue, expenses, changes in net assets or fund balances, functional expenses, program services, balance sheets, and lists of officers, directors, and trustees, offering a comprehensive financial overview of an organization. |

| Completion Requirements | Organizations are mandated to provide a thorough fiscal report, including contributions, program service revenue, assets, liabilities, and fund balances, making it essential for financial disclosure and regulatory compliance within Maryland. |

Steps to Filling Out Maryland Cof 85

Completing the Maryland COF-85 form involves a careful step-by-step process aimed at providing a clear financial picture of organizations that do not file Form 990. This form, crafted by the Secretary of State of Maryland, gathers comprehensive data regarding a nonprofit's revenue streams, expenses, net assets, and funding sources, amongst other details. Those tasked with filling it out must report both monetary and non-monetary contributions, as well as summarize the fiscal responsibilities undertaken in its operations. Below lies a structured guide designed to assist in the accurate completion of the form, ensuring all relevant aspects are duly addressed to meet compliance obligations.

- Start by entering the name and address of the organization at the top of the form.

- Input the city, state, and zip code for the location of the organization.

- Specify the fiscal year ending date to indicate the reporting period.

- In Part I, detail the organization’s revenues:

- Report all contributions, including gifts, grants, and similar amounts received, itemized by source under lines 1a through 1e.

- Enter program service revenue, membership dues, and assessment figures in lines 2 and 3.

- Fill in investment returns, including interest and dividends, under lines 4 and 5.

- Complete the rental income section by reporting gross rents and subtracting expenses to calculate net rental income on line 6.

- List other sources of income, such as special event net income, sale of inventory profits, and miscellaneous revenue under lines 7 through 11.

- Sum up the total revenue on line 12.

- Under the expenses section, lines 13 through 17, provide figures related to program services, management and general expenses, and fundraising costs, then calculate the total expenses.

- Calculate the excess or deficit for the year on line 18 by subtracting total expenses from total revenue.

- Update net assets or fund balances at the beginning and end of the year on lines 19 and 21, including any other changes in net assets (line 20).

- In Part II, list down functional expenses regarding grants, assistance, benefits, compensation, and other operational costs from lines 22 through 44.

- Detail each program service rendered along with the expenses and grants allocated to them in Part III.

- For Part IV, enumerate sources of program service revenue and other revenue, specifying the nature of the income.

- Complete the balance sheet section in Part V as applicable, based on the organization's total assets and liabilities.

- List the current officers, directors, and trustees, including their compensation and hours devoted to the position, in Part VI.

- If applicable, identify the five highest-paid individuals for professional services exceeding $30,000 in Part VII.

- Answer the organizational and operational questions listed in questions 76 through 78 and provide contact information for the individual responsible for the financial books.

- Finally, the form must be signed and dated by an authorized officer who declares under penalty of perjury that the information provided is true, correct, and complete. Include the officer’s name, title, and signature at the designated area.

Once every section of the Maryland COF-85 form has been meticulously filled out, the organization is closer to fulfilling its reporting obligations. Ensuring accuracy in this document is crucial for compliance with state regulations and contributes to maintaining transparency regarding the organization's financial health and operational efficacy.

More About Maryland Cof 85

What is the Maryland COF-85 Form?

The Maryland COF-85 Form is a financial document required by the Secretary of State for organizations that are not filing Form 990. This includes detailed information on an organization's revenue, expenses, and changes in net assets or fund balances for a specific fiscal year. The form ensures transparency and accountability, providing critical data on the financial health and operations of non-profit and non-filing entities in Maryland.

Who needs to file the Maryland COF-85 Form?

Organizations not required to file Form 990 with the Internal Revenue Service (IRS) but operating within Maryland need to complete the COF-85 Form. This might include smaller non-profits, certain faith-based organizations, and other entities exempt from standard IRS reporting requirements. It's essential for relevant organizations to verify their filing obligations to remain in compliance with state regulations.

What information must be provided on the COF-85 Form?

- Basic organization details such as name and address.

- Revenue details, including contributions, program service revenue, membership dues, and investment income.

- Expenses broken down by program services, management, and fundraising.

- Changes in net assets or fund balances.

- Statement of functional expenses, including grants and allocations, benefits to members, and compensation details.

- Program service revenue details and balance sheet information for assets, liabilities, and net worth.

How is the COF-85 Form submitted?

Once completed, the COF-85 Form should be submitted to the Secretary of State's office located in the State House, Annapolis, MD. The form can be mailed directly to the office. It is crucial to ensure that the form is signed and dated under the penalties of perjury to validate the information provided is true and correct.

What are the consequences of not filing the COF-85 Form?

Failure to file the COF-85 Form can result in penalties and could potentially jeopardize an organization's standing with the State of Maryland. Non-compliance might lead to a loss of certain exemptions or benefits and could expose the organization to legal or financial liabilities. Timely and accurate filing is essential to maintain an organization's integrity and public trust.

Can the COF-85 Form be amended if errors are found after submission?

Yes, if an organization discovers errors or omissions in their COF-85 Form after submission, they can file an amended form. It is important to contact the Secretary of State's office for guidance on the correct procedures for amending previously submitted information. Prompt action to correct mistakes demonstrates an organization's commitment to transparency and compliance.

Common mistakes

When completing the Maryland COF-85 form, individuals commonly make several mistakes. These errors can lead to delays in processing or incorrect financial reporting. Recognizing and avoiding these mistakes ensures accurate and timely submission of the form.

- Not double-checking for arithmetic errors: In sections dealing with financial calculations, it's easy to make simple math mistakes. Always recheck your amounts and totals.

- Leaving sections blank: Every question on the form should be answered, even if the response is "0" or "N/A" (not applicable). Blank sections can lead to misunderstandings regarding incomplete information.

- Incomplete address or organizational details: Ensure that the address, name of the organization, and other identifying details are fully and accurately provided. Omitting parts of this information can obscure the organization's identity.

- Failure to attach required schedules: Certain sections of the form ask for schedules or additional documentation. Failing to attach these documents can result in an incomplete submission.

- Incorrect fiscal year information: The fiscal year ending date must match the organization's records. Inconsistencies here can create confusion and inaccuracies in financial reporting.

- Misclassifying revenue and expenses: It's important to correctly categorize each type of revenue and expense in the provided sections to ensure accurate financial statements.

- Not reporting noncash contributions correctly: Organizations often overlook or incorrectly report the value of noncash contributions. These should be carefully estimated and correctly entered.

- Forgetting to sign and date the form: An unsigned or undated form is considered incomplete and cannot be processed.

- Ignoring updates or changes to the form instructions: The COF-85 form and its instructions may update over time. Not following the latest guidelines can result in incorrect submissions.

Ensuring all parts of the COF-85 form are completed accurately and attaching all required documentation will aid in the smooth processing of the form. Taking the time to review the form for errors before submission is crucial.

Documents used along the form

When filling out or filing the Maryland COF-85 form, understanding related documents can streamline the process and ensure that organizations comply with requirements fully. The Maryland COF-85 form is a comprehensive financial report for organizations not filing Form 990 with the IRS. This necessitates various supplemental forms and documents that support and verify the financial data presented. The significance of each auxiliary document is to provide clarity, detail, and adherence to regulatory standards. Examination of these related documents reveals an in-depth look into an organization's fiscal operations, enhancing transparency and accountability.

- Form 990: Though not used with COF-85 for organizations exempt from it, understanding the Form 990 and its variants can provide helpful context for how similar information might be structured and reported.

- IRS Determination Letter: This document confirms the organization's tax-exempt status, crucial for justifying exemptions when not filing Form 990.

- Articles of Incorporation: This foundational document establishes the organization's existence and contains critical details about its purpose, structure, and governance, which can be relevant for financial reporting.

- Bylaws of the Organization: Bylaws outline the rules under which the organization operates, including financial management practices that can be relevant to COF-85.

- Financial Statements and Records: Detailed financial statements such as balance sheets, income statements, and cash flow statements support the figures reported in COF-85.

- Schedule of Activities: A document detailing the organization's programs and activities can support the revenue and expense allocations on COIF-85.

- List of Officers, Directors, and Trustees: This list complements the COF-85's section on governance and compensation, providing detailed information about the individuals in charge and their compensation if any.

Together, these documents form a comprehensive profile of an organization's financial and operational practices over the fiscal year. They not only support the COF-85 form's data but also ensure that organizations maintain a clear record for internal audits and external reviews. Whether for internal governance, tax reporting, or regulatory compliance, each document serves an essential role in painting a complete picture of the organization's fiscal health and operational integrity.

Similar forms

The Maryland COF-85 form, required for certain organizations not filing form 990, shares similarities with several documents that are pivotal for financial and operational transparency within nonprofit and other organizational structures. Each comparable form possesses distinctive features that cater to the varied reporting needs and regulatory obligations of organizations within diverse legal and operational frameworks. Understanding these similarities enhances comprehension of the Maryland COF-85 form's role and its interconnections with broader financial reporting practices.

IRS Form 990 is a comprehensive financial report that nonprofit organizations must file annually with the Internal Revenue Service (IRS) in the United States. It details the organization's mission, programs, and finances. The Maryland COF-85 form is akin to the IRS Form 990 in several ways. Both solicit detailed information on revenue, expenses, and net assets or fund balances, aiming to provide a clear picture of the organization's financial health. However, Maryland's COF-85 form is tailored for organizations not required to file Form 990, offering a simplified mechanism to fulfill state-level reporting obligations without the broader scope of the IRS's requirements.

Form 990-EZ, considered a shorter version of the IRS Form 990, is designed for smaller organizations with gross receipts of less than $200,000 and total assets less than $500,000. Like the Maryland COF-85, Form 990-EZ aims to collect essential financial data but is less detailed than the standard Form 990, reducing the reporting burden on smaller entities. Both forms include sections on revenue, expenses, and changes in net assets, making the 990-EZ a closer match to the COF-85 for smaller organizations not covered by the full Form 990 mandates.

Form 990-PF is another document similar to the Maryland COF-85 form, tailored specifically for private foundations in the U.S. This form requires detailed financial reporting, including grants given, expenses, revenues, and changes in net assets. The resemblance between Form 990-PF and the Maryland COF-85 lies in their shared goal of ensuring transparency about financial activities. However, the COF-85 is distinct in its applicability to a broader range of organizations not filing Form 990, thereby serving a wider audience with its reporting requirements.

Dos and Don'ts

Filling out the Maryland COF-85 form is an important task that can have significant implications for an organization. When preparing this document, there are several things you should do and avoid to ensure accuracy and compliance. Here's a straightforward list of dos and don'ts:

- Do thoroughly review all instructions related to the form before beginning to fill it out.

- Don't rush through the form. Take your time to accurately report your organization's financial data.

- Do ensure all financial amounts reported are accurate and match your organization's financial statements.

- Don't leave any required fields blank. If a question does not apply, note it as "N/A" (not applicable).

- Do use the exact name of your organization and address as registered with the state or IRS.

- Don't guess on numbers or dates. Verify all information with your financial records.

- Do attach all required schedules and additional information as instructed by the form.

- Don't sign the form without reviewing it for completeness and accuracy.

- Do have an authorized officer of the organization sign and date the form as required.

These tips can help ensure that the process of completing the COF-85 form for your organization goes smoothly and reduces the risk of errors that could potentially delay its processing or impact your organization’s compliance status.

Misconceptions

Understanding financial reporting forms is crucial for organizations to accurately present their financial standings and adhere to regulations. Among these, the Maryland COF-85 form, a financial document required by the Secretary of State for certain organizations not filing Form 990, is often misunderstood. Clarifying common misconceptions can aid organizations in completing this form correctly and ensure compliance.

Misconception 1: The form is only for non-profit organizations. While primarily designed for non-profits, the COF-85 form may be required from any organization not filing Form 990 with the IRS, depending on specific state requirements.

Misconception 2: All sections of the form must be completed by all organizations. The sections required vary based on the organization's revenue and activities. For instance, organizations with revenues under a certain threshold may not need to complete the entire balance sheet.

Misconception 3: The form is a substitute for Form 990. COF-85 is a state requirement and does not replace the federal obligations of filing Form 990 for organizations that are required to do so.

Misconception 4: Submission of this form grants tax-exempt status. Completing and submitting COF-85 is a reporting requirement, not a process for obtaining tax exemption.

Misconception 5: The form requires detailed personal information about donors. The form focuses on financial information and does not require detailed personal information about individual donors.

Misconception 6: Government grants should not be reported. Government contributions (grants) are distinctly identified in the form and must be reported accurately.

Misconception 7: Only cash contributions are to be reported. The form requires reporting both cash and non-cash contributions, emphasizing the importance of accurately reporting all forms of received support.

Misconception 8: Organizations can estimate financial figures. All figures reported must be accurate and substantiated by financial records, as the form is a legal document submitted under the penalties of perjury.

Misconception 9: There is no need to keep records once the form is filed. Organizations should maintain detailed records to support the information reported on the COF-85 form, in case of audit or review.

Misconception 10: Any officer can sign the form. The form must be signed by an authorized officer of the organization who has reviewed the complete document, ensuring its accuracy and completeness.

Dispelling these misconceptions ensures organizations can accurately complete and submit the Maryland COF-85 form, aiding in regulatory compliance and fostering transparency in financial reporting.

Key takeaways

Filling out and using the Maryland COF-85 form is essential for organizations that do not file Form 990. Here are eight key takeaways to ensure accurate and compliant submissions:

- The form is specifically designed by the Secretary of State in Annapolis, MD, for organizations not filing Form 990, underscoring the need for an alternative financial reporting tool.

- It requires detailed information about the organization, including its name, address, and financial data for the specified fiscal year, highlighting the importance of precise record-keeping.

- Part I of the form focuses on revenue, expenses, and changes in net assets or fund balances, necessitating a comprehensive understanding of the organization's financial activities.

- Contributions, gifts, grants, and similar amounts received are broken down into several categories (direct public support, indirect public support, government contributions, etc.), which necessitates careful categorization of income sources.

- Program service revenue, membership dues, interest on investments, and other income streams are separately listed, requiring organizations to accurately track and report diverse revenue sources.

- The form also details functional expenses, such as compensation, benefits, and operational expenses, reinforcing the need for diligent financial management.

- Organizations must list program services rendered, including specific activities and their corresponding financial data, emphasizing the link between missions, programs, and finances.

- Officers, directors, and trustees, including details about their compensation and hours devoted to the position, must be disclosed, ensuring transparency in organizational governance.

Accurately completing the Maryland COF-85 form is crucial for maintaining compliance with state requirements. By providing a detailed snapshot of an organization's financial health and activities, it not only helps in meeting legal obligations but also assists in financial planning and management. Organizations are advised to consult with professionals or refer to detailed instructions provided by the Secretary of State to ensure completeness and accuracy of the form.

Common PDF Templates

Maryland 502 Form - Nonresidents can claim credits like the earned income credit and poverty level credit through this form.

Maryland Confidential Morbidity Report - Includes options for reporting pertinent clinical information and additional comments for clarity.

How Many Hours Can I Work at 16 - Clarifies the work permit process for minors in Maryland, underlining the tripartite agreement necessary for lawful employment.