Maryland Mw506Ae PDF Template

In the picture of intricate fiscal responsibilities that frame the real estate landscape, the Maryland Form MW506AE shines a spotlight on a crucial aspect for nonresident individuals and entities navigating the sale of real property within the state. As a prerequisite choreographed by the Comptorller of Maryland, this form embarks on its journey with a bold declaration: to carve a path for seeking a Certificate of Full or Partial Exemption from withholding requirements that otherwise grip the proceeds from such sales. Entrusted with the deadline of reception no less than 21 days prior to the property’s closing date, it embodies the essence of proactive fiscal management. Demarcating the boundaries for eligibility, it caters to a diverse clientele ranging from individuals to corporations, trusts, and partnerships, rendering it a linchpin in transactions that otherwise would be entangled in withholding norms. As the form unfolds, it prompts the elucidation of property and seller information, diligently weaving through the narrative of the property’s journey—from its acquisition to the imminent sale, peering through the lens of reasons eligible for exemption, and culminating in the precision of tax calculation to be withheld—if partial exemption is granted. Thus, navigating through this form is not merely an administrative exercise but a fervent stride towards harnessing an informed leverage within Maryland's real estate realm, projecting clarity and confidence for nonresident sellers on the precipice of transition.

Maryland Mw506Ae Sample

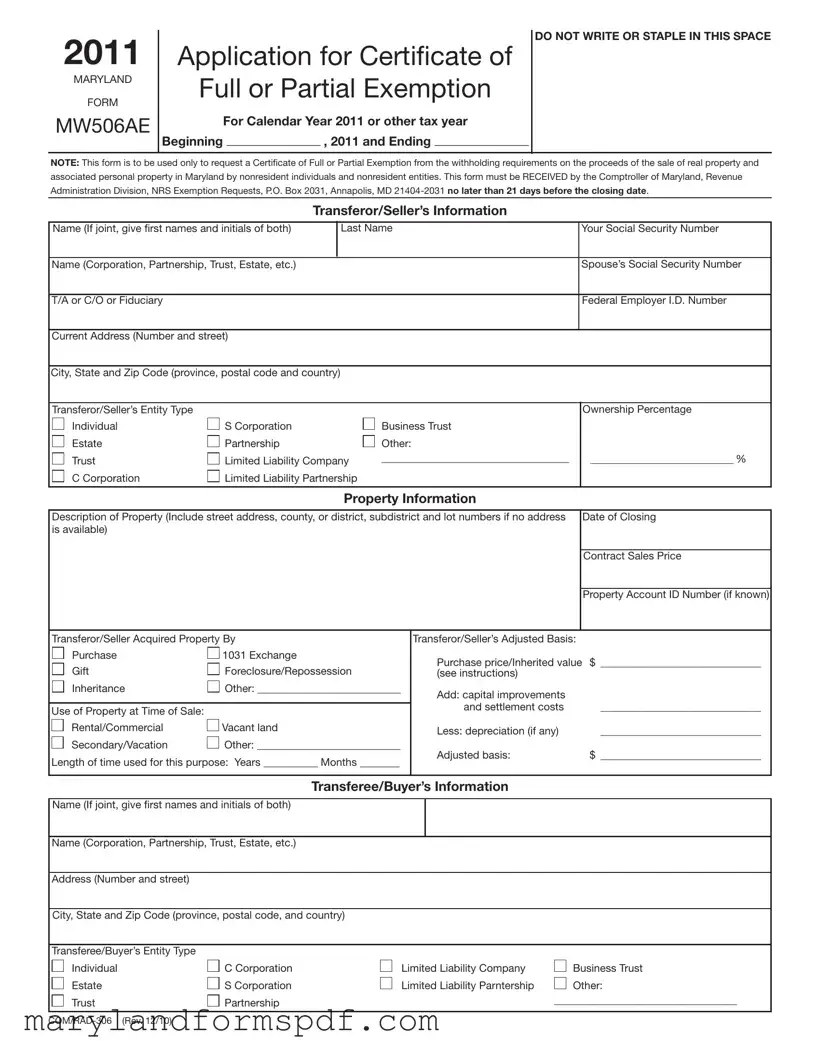

2011

MARYLAND

FORM

MW506AE

Application for Certificate of

Full or Partial Exemption

For Calendar Year 2011 or other tax year

Beginning ________________ , 2011 and Ending ________________

DO NOT WRITE OR STAPLE IN THIS SPACE

NOTE: This form is to be used only to request a Certificate of Full or Partial Exemption from the withholding requirements on the proceeds of the sale of real property and associated personal property in Maryland by nonresident individuals and nonresident entities. This form must be RECEIVED by the Comptroller of Maryland, Revenue Administration Division, NRS Exemption Requests, P.O. Box 2031, Annapolis, MD

Transferor/Seller’s Information

Name (If joint, give first names and initials of both) |

|

Last Name |

|

|

|

|

Your Social Security Number |

||

|

|

|

|

|

|

|

|

|

|

Name (Corporation, Partnership, Trust, Estate, etc.) |

|

|

|

|

|

|

|

Spouse’s Social Security Number |

|

|

|

|

|

|

|

|

|

|

|

T/A or C/O or Fiduciary |

|

|

|

|

|

|

|

|

Federal Employer I.D. Number |

|

|

|

|

|

|

|

|

|

|

Current Address (Number and street) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

City, State and Zip Code (province, postal code and country) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Transferor/Seller’s Entity Type |

|

|

|

|

|

|

|

|

Ownership Percentage |

Individual |

S Corporation |

|

|

Business Trust |

|

|

|||

Estate |

Partnership |

|

|

Other: |

|

|

|||

Trust |

Limited Liability Company |

______________________________________ |

|

_____________________________ % |

|||||

C Corporation |

Limited Liability Partnership |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||

|

|

|

Property Information |

|

|

||||

|

|

|

|

|

|||||

Description of Property (Include street address, county, or district, subdistrict and lot numbers if no address |

|

Date of Closing |

|||||||

is available) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contract Sales Price |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Property Account ID Number (if known) |

|

|

|

|

|

|

|

|

||

Transferor/Seller Acquired Property By |

|

|

|

|

Transferor/Seller’s Adjusted Basis: |

||||

Purchase |

1031 Exchange |

|

|

|

|

|

Purchase price/Inherited value $ ______________________________ |

||

Gift |

Foreclosure/Repossession |

|

|

|

|||||

|

|

|

(see instructions) |

|

|

||||

Inheritance |

Other: _____________________________ |

|

|

Add: capital improvements |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and settlement costs |

______________________________ |

|

Use of Property at Time of Sale: |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

Rental/Commercial |

Vacant land |

|

|

|

|

|

Less: depreciation (if any) |

______________________________ |

|

|

|

|

|

|

|

|

|||

Secondary/Vacation |

Other: _____________________________ |

|

|

Adjusted basis: |

$ ______________________________ |

||||

Length of time used for this purpose: Years ___________ Months ________ |

|

|

|||||||

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|||

|

|

Transferee/Buyer’s Information |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

Name (If joint, give first names and initials of both) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (Corporation, Partnership, Trust, Estate, etc.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address (Number and street) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

City, State and Zip Code (province, postal code, and country) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Transferee/Buyer’s Entity Type |

|

|

|

|

|

|

|

|

|

Individual |

C Corporation |

|

|

|

Limited Liability Company |

Business Trust |

|||

Estate |

S Corporation |

|

|

|

Limited Liability Parntership |

Other: |

|||

Trust |

Partnership |

|

|

|

_____________________________________ |

||||

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

MARYLAND FORM |

Application for Certificate of Full or Partial Exemption |

2011 |

|

MW506AE |

|||

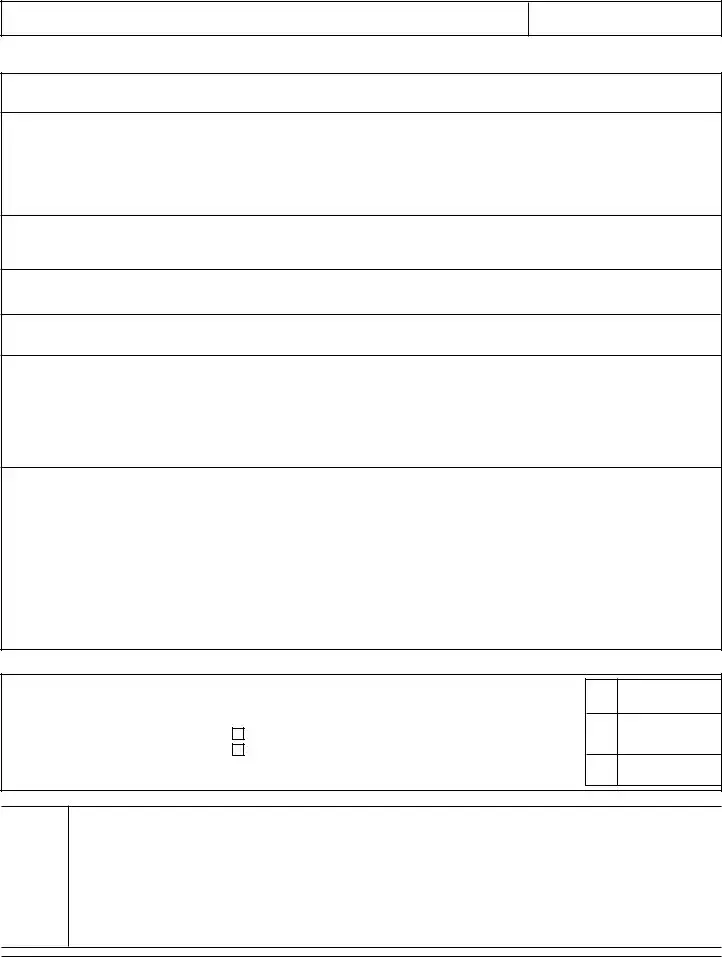

Page 2 |

Transferor/Seller’s Name

Your Social Security Number/FEIN

Reason for Full or Partial Exemption from Withholding

(Attach documentation and calculation)

1.☐ Transfer is of a principal residence as defined in IRC §121.

2.☐ Transfer is a

☐simultaneous without boot,

☐simultaneous with boot, or

☐delayed, with funds in escrow for acquiring replacement property.

3.☐ Transfer is pursuant to an installment sale under IRC §453 and the transferor/seller will receive less than the full purchase price during the taxable year.

4.☐ Transfer of inherited property is occurring within 6 months of date of death.

5.☐ Transferor/Seller is receiving zero proceeds from this transaction.

6.☐ Transfer is pursuant to a transaction under a specific section of the Internal Revenue Code or other code. Place code letter for your transaction in the box below. (See instructions for detailed descriptions):

☐

7. ☐ Other. Provide a brief explanation in the space provided:

Calculation of Tax to be Withheld

1. |

Enter the amount subject to tax witholding. Subtract adjusted basis from contract sales price |

|

2. |

Enter tax rate, whichever applies. |

|

|

a. If you are a business entity, enter 8.25% |

........................................................... ....................................... |

|

|

|

|

b. If you are an individual, enter 6.75% |

........................................................... |

|

|

|

3. |

Amount of tax to be withheld at closing. Line 1 multiplied by line 2. (This line MUST be completed.) |

|

1

2

3

Please

Sign

Here

Under the penalties of perjury, I declare that I have examined this application, including any schedules or statements attached, and to the best of my knowledge and belief, it is true, correct and complete. If prepared by a person other than taxpayer, the declaration is based on all information of which the preparer has any knowledge.

_____________________________________________ |

___________________________ |

___________________________ |

Signature |

Applicant’s phone number |

Date |

_____________________________________________ |

___________________________ |

___________________________ |

Signature |

Applicant’s phone number |

Date |

_____________________________________________ |

___________________________ |

___________________________ |

Signature |

Applicant’s phone number |

Date |

(Rev. 12/10)

MARYLAND FORM |

INSTRUCTIONS FOR APPLICATION FOR |

2011 |

|

MW506AE |

|||

CERTIFICATE OF FULL OR PARTIAL EXEMPTION |

|||

|

|

The Comptroller’s decision to issue or deny a certificate and the amount of tax is final and not subject to appeal.

GENERAL INSTRUCTIONS

Purpose of Form

Use Form MW506AE to apply for a Certificate of Full or Partial Exemption from the withholding requirements on the proceeds of the sale of real property and associated personal property in Maryland by nonresident individuals and nonresident entities. A nonresident entity is defined to mean an entity that: (1) is not formed under the laws of Maryland; and (2) is not qualified by or registered with the Department of Assessments and Taxation to do business in Maryland.

Who May File an Application

An individual, fiduciary, C corporation, S corporation, limited liability company, or partnership transferor/seller may file Form MW506AE. Unless the transferors/ sellers are a husband and wife filing a joint Maryland income tax return, a separate Form MW506AE is required for each transferor/seller.

IMPORTANT: The completed Form MW506AE must be received by the Comptroller of Maryland no later than 21 days before the closing date of the sale or transfer to ensure timely receipt of a Certificate of Full or Partial Exemption.

The Comptroller’s decision to issue or deny a Certificate of Full or Partial Exemption and the determination of the amount of tax to be withheld if a partial exemption is granted are final and not subject to appeal.

SPECIFIC INSTRUCTIONS

Enter the tax year of the transferor/ seller if other than a calendar year.

Transferor/Seller’s Information

Enter the name, address and identification number (Social Security number or federal employer identification number) of the transferor/ seller applying for the exemption.

If the transferor/seller was issued

an individual taxpayer identification number (ITIN) by the IRS, enter the ITIN.

Check the box indicating the transferor/seller’s entity type.

Enter the transferor/seller’s ownership percentage of the property.

Property Information

Enter the description of the property, including the street address(es) for the property as listed with the State Department of Assessments and Taxation (SDAT), including county. If the property does not have a street address, provide the full property account ID numbers used by SDAT to identify the property.

Enter the date of closing for the sale or transfer of the property.

Enter the contract sales price of the property being sold or transferred.

Enter the property account ID number, if known. If the property is made up of more than one parcel and has more than one property tax account number, include all applicable property account ID numbers.

Check the box that describes the transferor/seller’s acquisition of the property. Check the box that describes the transferor/seller’s use of the property at the time of the current sale, and enter the length of time

the property has been used for this purpose.

Complete the transferor/seller’s adjusted basis section by entering the purchase price when the transferor/ seller acquired the property, adding the cost of capital improvements (including acquisition costs such as commissions and state transfer taxes), and subtracting depreciation, if applicable. If inherited property, use the Date of Death value of the property.

Transferee/Buyer’s Information

Enter the name and address.

Check the box indicating the transferee/buyer’s entity type.

Attach schedule if there are multiple transferees/buyers.

Reason for Full or Partial Exemption from Withholding

Check the box in the “Reason for Exemption” column that indicates the reason you are requesting a full or partial exemption from the income tax withholding requirements.

Specific Line Instructions for Reason for Full or Partial Exemption

Line 1. Transfer is of your principal residence as defined in §121 of the Internal Revenue Code, which means it has been your principal residence for two of the last five years.

Required Documentation: Copy of contract of sale or copy of estimated

Line 2. Transfer is a

Required documentation: Letter signed by the qualified intermediary, or by the person authorized to sign on behalf of a business entity acting as the qualified intermediary, which states the name(s) of the transferor(s), the property description, that the individual or business will be acting as the qualified intermediary for

the transferor(s) as part of a §1031 exchange of the property, whether there will be any boot, and if so, the amount of boot. The amount of any boot must be stated on the application as the taxable amount.

Line 3. Transfer is pursuant to an installment sale under §453 of the Internal Revenue Code.

Required documentation: Copy of contract of sale or copy of

Line 4. Transfer of inherited property is occurring within 6 months of date of death.

Required Documentation: Provide a copy of the death certificate and a copy of the estimated HUD-

1 settlement sheet from the title company.

Line 5. Transferor/seller is receiving zero proceeds from this transaction.

Required Documentation: A copy of a letter from the transferor/seller to the title company advising they are to receive zero proceeds from the sale and advising to whom the proceeds are to go; a copy of the acknowledgment letter from the title company to the transferor/seller.

Line 6. Transfer is one of the following transactions. Please note the code letter and record it in the box on page 2 of Form MW506AE.

a. Transfer is to a corporation con- trolled by the transferor for purposes of §351 of the Internal Revenue Code.

Required documentation: Copy of the agreement of sale; Certificate of Good Standing of transferee is- sued by the state in which transferee is incorporated; notarized affidavit executed on behalf of transferee by its President and its Treasurer stating that immediately after the exchange the transferor(s) will own stock in the transferee possessing at least eighty percent (80%) of the total combined voting power of all classes of trans- feree’s stock entitled to vote and at least eighty percent (80%) of the total number of shares of all other classes of stock of the transferee; and an apprais- al establishing the fair market value,

at the time of the exchange, of any

property other than stock in the trans- feree which is part of the consideration for the exchange. The fair market value of any such other property and/or any money which is part of the con- sideration for the exchange must be stated on the application as the taxable amount.

b. Transfer is pursuant to a

Required documentation: Copy of agreement governing the transfer between transferor and transferee; Cer- tificates of Good Standing of transferor and transferee issued by the state(s) in which transferor and transferee are incorporated; copy of the plan or reor- ganization showing that transferor and transferee are parties to the reorgani- zation; and an appraisal establishing the fair market value, at the time of the exchange, of any property other than stock or securities in the transferee which is part of the consideration for the exchange and will not be distribut- ed by the transferor in pursuance of the plan of reorganization. The fair market value of any such other property and/or any money which is part of the con- sideration for the exchange must be stated on the application as the taxable amount.

c. Transfer is by a

Required documentation: Copy of determination by the Internal Revenue Service that transferor is a

d. Transfer is to a partnership in exchange for an interest in the part- nership such that no gain or loss is recognized under §721 of the Internal Revenue Code.

Required documentation: Copy of agreement governing transfer between transferor and transferee; copy of the partnership agreement of the trans- feree.

e. Transfer is by a partnership to a partner of the partnership in accor- dance with §731 of the Internal Rev- enue Code.

Required documentation: Copy of agreement governing transfer between transferor and transferee; copy of the partnership agreement of the transferor.

f. Transfer is treated as a transfer by a real estate investment trust for pur- poses of §857 of the Internal Revenue Code.

Required documentation: Copy of agreement governing transfer between transferor and transferee; certified copy of Articles of Incorporation of trans- feror; Certificate of Good Standing of transferor issued by the state in which transferor is incorporated.

g. Transfer is pursuant to a condem- nation and conversion into a similar property for purposes of §1033 of the Internal Revenue Code.

Required documentation: Copy of agreement governing transfer between transferor and government body or authority condemning the property; notarized affidavit executed by trans- feror stating that transferor will identify and purchase replacement property within the time limits required by §1033 of the Internal Revenue Code, or copy of contract of sale if transferor has already identified replacement property. If proceeds from condemnation exceed price of replacement property, the ex- cess must be stated on the application as the taxable amount.

h. Transfer is between spouses or in- cident to divorce for purposes of §1041 of the Internal Revenue Code.

Required documentation: Copy of marriage license or divorce decree; copy of deed which will be recorded to accomplish the transfer; if incident to divorce, copy of section of court order or separation agreement governing transfer of the property.

i. Transfer is treated as a transfer by an S corporation for purposes of §1368 of the Internal Revenue.

Line 7. Other. The transfer is otherwise fully or partially exempt from the recognition of gain in accordance with provided explanation.

Required documentation: Attach any and all documents necessary to show that the transfer is fully or partially exempt from tax. This may include a copy of contract of sale or copy of estimated

Calculation of Tax to be Withheld

Complete this section if you are requesting a partial exemption. This section must be completed or the application for partial exemption will be denied.

Signature(s)

Form MW506AE must be signed by an individual (both taxpayer and spouse, if filing a joint Maryland income tax return), or a responsible corporate officer.

Please include a daytime telephone number where you can be reached between 8:00 AM and 5:00 PM.

Your signature(s) signifies that your application, including all attachments, is, to the best of your knowledge and belief, true, correct and complete, under the penalties of perjury.

If a power of attorney is necessary, complete federal Form 2848 and attach to your application.

Where to File

Mail the completed form and all attachments to:

Comptroller of Maryland

Revenue Administration Division

Attn: NRS Exemption Requests

P.O. Box 2031

Annapolis, MD

Additional Information

For additional information visit www.marylandtaxes.com,

File Breakdown

| Fact Number | Description |

|---|---|

| 1 | The Form MW506AE is specifically designed for nonresident individuals and entities selling real estate and associated personal property in Maryland to apply for either a full or partial exemption from Maryland's withholding requirements on the sale's proceeds. |

| 2 | This application must be received by the Comptroller of Maryland's Revenue Administration Division at least 21 days before the real estate closing date. |

| 3 | Eligibility for filing Form MW506AE extends to a variety of entities, including individuals, fiduciaries, C corporations, S corporations, limited liability companies, and partnerships. |

| 4 | The form allows for claiming exemption based on several circumstances, including the sale of a principal residence, a 1031 exchange, installment sales under IRC §453, transfer of inherited property, and several other specific conditions detailed within the Internal Revenue Code. |

| 5 | Documentation must accompany requests for exemption, which may include items like copies of the sale contract, death certificates, IRS determinations, partnership agreements, among others, depending on the exemption's basis. |

| 6 | For partial exemptions, the form requires detailed calculations of the tax to be withheld, based on the contract sales price less the seller's adjusted basis and applicable tax rates for businesses or individuals. |

| 7 | Decisions made by the Comptroller regarding the issuance or denial of the exemption certificate and the determination of the withholding amount are final and not subject to appeal. |

| 8 | Completed forms along with necessary attachments should be mailed to the Comptroller of Maryland, highlighting the specific division handling NRS Exemption Requests, ensuring compliance with the deadline set for submission prior to the property's closing date. |

| 9 | For assistance or additional information regarding the Form MW506AE, contacts include Maryland's taxpayer service numbers and their website, equipped to handle inquiries about exemptions for nonresident sales of real property. |

Steps to Filling Out Maryland Mw506Ae

When preparing to sell real property in Maryland as a nonresident, it is essential to be well-informed about the specific requirements to ensure a smooth transaction. One of these requirements is the Maryland Form MW506AE, a vital document for those seeking an exemption from the withholding requirements on the sale's proceeds. Given the complexity of tax regulations, it's crucial to approach this form carefully to ensure accurate reporting and compliance. Below, you will find a simplified guide, step by step, on how to fill out this form. This guide is designed to ease the process, making sure you meet your obligations without undue stress.

- Start by identifying the tax year for which you're applying for the exemption. If it's not for the calendar year 2011, specify the applicable tax year at the top of the form.

- Under Transferor/Seller’s Information, provide the name(s), Social Security Number(s), or Federal Employer ID Number as applicable. Include your current address, city, state, zip code, and, if relevant, the country’s postal code.

- Select your entity type (e.g., Individual, S Corporation, Partnership, etc.) and specify your ownership percentage in the provided space.

- In the Property Information section, describe the property thoroughly, including its street address, county, and any identifying numbers if the address is not available. Indicate the date of closing and the contract sales price along with the property account ID number if known.

- Detail how you acquired the property (purchase, gift, inheritance, etc.) and describe its use at the time of sale (e.g., rental/commercial, secondary/vacation home). Include both the duration of use and the property’s adjusted basis, factoring in any improvements and subtracting any depreciation.

- For the Transferee/Buyer's Information, fill in the names, address, and entity type. Attach an additional schedule if there are multiple transferees/buyers.

- Select the reason for your request for a Full or Partial Exemption from Withholding, checking the box that applies to your situation and providing any required documentation and calculations as noted in the form instructions.

- In the section on Calculation of Tax to be Withheld, enter the amount subject to tax withholding, apply the correct tax rate (8.25% for business entities, 6.75% for individuals), and calculate the total tax to be withheld. This section is mandatory for partial exemption requests.

- Complete the form with your signature, date, and telephone number where you can be reached. If the form is prepared by someone other than the taxpayer, they must also sign, certifying their basis of knowledge.

After completing the form, review it to ensure all information is accurate and that all necessary documentation is attached. Mail the completed form and attachments to the specified address in Annapolis, at least 21 days before the property closing date to meet Maryland's requirement. This proactive step is crucial for enabling a smoother transaction, potentially sparing you from unnecessary delays or complications. Remember, compliance with state tax requirements not only protects you legally but also contributes to a more transparent and smooth property transfer process.

More About Maryland Mw506Ae

What is the Maryland Form MW506AE?

The Maryland Form MW506AE, also known as the Application for Certificate of Full or Partial Exemption, is a document specifically designed for nonresident individuals and entities to request an exemption from withholding requirements on the proceeds from the sale of real estate and associated personal property in Maryland. Whether you're selling a piece of property in 2011 or another specified tax year, this form plays a crucial role in potentially lowering your tax obligations related to the sale. It's essential for the form to be submitted to the Maryland Comptroller, Revenue Administration Division, no later than 21 days before the property sale's closing date.

Who needs to file the Maryland Form MW506AE?

Both nonresident individuals and nonresident entities that are selling real estate and associated personal property in Maryland need to file Form MW506AE if they seek full or partial exemption from the state's withholding requirements. The term nonresident entities refer to organizations not formed under the laws of Maryland or those not qualified by or registered with the Department of Assessments and Taxation to conduct business within the state. Separate forms are required for each seller involved unless filing jointly as a married couple.

What documentation is required for filing Form MW506AE?

The documentation required alongside your Form MW506AE depends largely on the basis of your exemption claim. Below are examples of scenarios and their requisite documents:

- Principal Residence: Copies of the sale contract or the estimated HUD-1 settlement sheet, along with receipts for capital improvements and a copy of the HUD-1 settlement sheet from the property purchase.

- Tax-free Exchanges: A letter from the qualified intermediary highlighting the exchange details and, if applicable, the amount of boot received.

- Installment Sales: Copies of the sale contract, HUD-1 settlement sheet, and the promissory note to the seller.

- Inherited Property: A copy of the death certificate and the estimated HUD-1 settlement sheet.

It's important to attach all necessary documentation to ensure the application is processed smoothly and to avoid any delays.

Where and how do you file Form MW506AE?

Filing Form MW506AE requires mailing the completed form along with any required documentation to the Comptroller of Maryland, Revenue Administration Division, specifically to the NRS Exemption Requests section at P.O. Box 2031, Annapolis, MD 21404-2031. Before mailing, ensure that all parts of the form are correctly filled out, and that the application is signed. The signature verifies that the information provided is accurate and truthful, under penalty of perjury. For convenience and further clarification, you may visit the official Maryland taxes website or contact them via email or phone for additional guidance.

Common mistakes

When filling out the Maryland MW506AE form, people often make several mistakes. Here is a list of common errors:

- Not submitting the form to the Comptroller of Maryland, Revenue Administration Division, NRS Exemption Requests, at least 21 days before the closing date.

- Incorrectly entering the Social Security Number or Federal Employer Identification Number, which can lead to processing delays.

- Failing to clearly identify the type of transferor/seller's entity, such as an individual, S Corporation, or partnership.

- Omitting or inaccurately detailing the description of the property, including street address, county, district, subdistrict, and lot numbers.

- Not providing the correct property information, such as the date of closing, contract sales price, and property account ID number.

- Miscalculating the adjusted basis by forgetting to add capital improvements and settlement costs or subtracting depreciation where applicable.

- Choosing the wrong reason for Full or Partial Exemption from Withholding without attaching the required documentation and calculation.

- Leaving the calculation of tax to be withheld section incomplete or making errors in the computation if requesting a partial exemption.

- Forgetting to sign the form or include a daytime telephone number. This oversight can cause significant delays in processing.

These mistakes can lead to the delay or denial of the Certificate of Full or Partial Exemption. Therefore, it's crucial to review the form thoroughly before submission.

Documents used along the form

When dealing with real estate transactions in Maryland, specifically regarding the sale of real property by nonresident individuals or entities, the Maryland MW506AE form plays a critical role in requesting Certificates of Full or Partial Exemption from withholding requirements. However, this form is just one piece of a broader set of documents often required in such transactions. Understanding each document's purpose and how they interrelate can streamline the process and ensure compliance with state laws and regulations.

- Uniform Residential Loan Application: Used by borrowers to apply for a mortgage, detailing financial status, employment history, and property details.

- Hud-1 Settlement Statement: A comprehensive itemization of all the costs associated with closing a residential real estate transaction, used for comparing with the Good Faith Estimate.

- Deed of Trust or Mortgage: A legal document between the borrower and the lender securing the loan with the property being purchased.

- Title Insurance Policy: Protects the buyer and the lender from any losses due to disputes over the property's title.

- Property Tax Records: Documents showing the property's tax history, which can be essential for understanding any outstanding obligations.

- Homeowners' Association (HOA) Documents: For properties in HOA-managed communities, these documents outline the rules, fees, and regulations of the association.

- Home Inspection Reports: Provide detailed information on the condition of the property, identifying any potential issues before the sale.

- Proof of Homeowners' Insurance: Required by lenders to ensure the property is covered against damages from insured events.

- IRS Form 1099-S: For reporting the proceeds from real estate transactions to the IRS, potentially necessary for tax purposes.

Each document serves a unique purpose in the context of real estate transactions, providing assurances, financial details, or legal protection to the parties involved. By familiarizing themselves with these documents, parties in a Maryland real estate transaction can ensure a smoother process and adherence to legal and financial requirements, enhancing the transparency and security of the transaction.

Similar forms

The Maryland MW506AE form is similar to other documents used in the real estate and tax spaces, specifically for declaring exemptions or calculating taxes due on the transfer of property. These can include forms and applications related to nonresident taxes, real estate sales, and property transfers. More details about these documents reveal the distinct but connected purposes they serve.

One such document is the Federal Form 8288-B, Application for Withholding Certificate for Dispositions by Foreign Persons of U.S. Real Property Interests. Both the Maryland MW506AE and Form 8288-B serve to request exemption or reduced withholding on real estate transactions. However, while the Maryland form is state-specific, targeting nonresident individuals and entities selling property within Maryland, Form 8288-B applies to foreign persons disposing of U.S. real property interests on a nationwide basis. The similarity lies in their function to navigate withholding requirements, but they cater to different jurisdictions and demographics.

Another similar document is the Nonresident Real Property Estimated Income Tax Payment Form used in various states, such as New York's IT-2663. Like the Maryland MW506AE, this form applies to nonresident entities involved in real estate transactions. It is designed to calculate and remit estimated income tax on the sale of real property located within the state. Both forms address the concept of withholding income tax from nonresidents to ensure tax compliance. However, Maryland's MW506AE specifically focuses on granting full or partial exemptions, whereas forms like IT-2663 primarily concentrate on estimating and collecting tax due upfront.

Lastly, the Capital Gains Tax Return forms, which vary by state, share a purpose with the Maryland MW506AE in terms of addressing the tax implications of transferring property. While capital gains forms are broader in scope, covering various types of capital assets beyond real estate, the MW506AE is specialized for real estate transactions by nonresidents in Maryland. Both sets of forms deal with assessing tax liability from the appreciation of assets, but the MW506AE is unique in its focus on the exemption aspect for nonresidents.

Dos and Don'ts

When filling out the Maryland MW506AE form, it's essential to pay attention to detail and follow specific guidelines to ensure successful submission. Here are things you should and shouldn't do:

Do:- Submit the form on time: Ensure that the completed form is received by the Comptroller of Maryland no later than 21 days before the closing date.

- Fill out all sections accurately: Provide complete and accurate information in every section to avoid delays or denial of your application.

- Attach required documentation: Depending on your reason for exemption, attach all necessary documents, such as a copy of the contract of sale or a death certificate for inherited property.

- Check entity type and ownership percentage: Clearly indicate your entity type and accurately state your ownership percentage of the property.

- Sign the form: Ensure that all required parties sign the form to certify that the information is true, correct, and complete under the penalties of perjury.

- Include a daytime phone number: Provide a contact number where you can be reached between 8:00 AM and 5:00 PM for any questions regarding your application.

- Submit incomplete forms: Failing to fill out all required fields can result in your application being delayed or denied.

- Forget to attach documentation: Omitting necessary documents based on your exemption reason can lead to application rejection.

- Ignore specific line instructions: Each reason for exemption requires specific documentation. Ensure you follow these instructions carefully.

- Miss the submission deadline: Sending the form later than 21 days before the closing date may prevent timely receipt of your Certificate of Full or Partial Exemption.

- Miscalculate tax: If requesting a partial exemption, carefully complete the tax calculation section to avoid errors.

- Use the form for other purposes: The MW506AE form is specifically for requesting an exemption from withholding on the sale of property by nonresidents. It should not be used for other filings or purposes.

Misconceptions

Misconceptions about the Maryland MW506AE form can range from its purpose to the details required for its successful submission. Here are nine common misconceptions and clarifications to help understand this form better.

- Only for individuals: Some people believe the Maryland MW506AE form is exclusively for individual use. However, it's also applicable to nonresident entities, such as corporations, partnerships, and trusts, seeking a full or partial exemption from withholding requirements on real property sales.

- Limited to residential properties: There's a misconception that this form applies only to residential property transactions. In reality, the exemption can apply to both residential and commercial properties, including associated personal property, sold by nonresidents of Maryland.

- Automatic approval: A common misunderstanding is that submitting Form MW506AE guarantees an approval for exemption. Approval is at the discretion of the Comptroller of Maryland based on the documentation and rationale provided by the applicant.

- Exemption reasons: It's often mistakenly thought that exemptions are only based on the property being a principal residence. There are multiple reasons for an exemption, including tax-free exchanges, installment sales, and transfers of inherited property within 6 months of the date of death.

- Last-minute submission: Some believe that the form can be submitted close to or at the time of closing. However, it must be received by the Comptroller no later than 21 days before the closing date to ensure timely processing.

- Electronic submission: There's a misconception that the MW506AE form can be submitted electronically. As of the last update, the form needs to be mailed to the specific address provided by the Comptroller of Maryland.

- Tax consultation not necessary: While it might seem straightforward, the process of applying for an exemption might require advice from a tax professional to ensure the proper documentation and rationale are provided, especially considering the finality of the Comptroller's decision.

- Single form for joint sellers: A common mistake is thinking that a single form suffices for properties owned jointly by individuals other than married couples filing jointly. Each nonresident individual or entity must file a separate MW506AE form.

- Specific to 2011: While the document mentioned relates to the year 2011, the requirement for the MW506AE form persists beyond that year. The form is updated annually, reflecting the need for nonresident individuals and entities to apply for exemptions for any year they engage in relevant transactions.

Understanding these misconceptions and clarifications helps in accurately completing and submitting the Maryland MW506AE form, ensuring compliance with the state's requirements for property sales by nonresidents.

Key takeaways

When engaging with the Maryland MW506AE form, an application crucial for entities and individuals not residing in Maryland that are involved in the sale of real property and associated personal property within the state, it is essential to be well-versed in the nuances of its requirements. The following key takeaways are designed to provide clarity and aid in the seamless completion and utilization of this form:

- The purpose of the MW506AE form is to apply for either a full or partial exemption from the withholding requirements typically imposed on the sale proceeds of real property and associated personal property by non-resident individuals and entities in Maryland. It highlights the state's effort to regulate and ensure tax compliance on real estate transactions involving non-residents.

- This form mandates submission to the Comptroller of Maryland, specifically to the Revenue Administration Division, and requires adherence to a strict deadline—being no later than 21 days before the scheduled closing date of the property sale. Highlighting the importance of planning and timely submission is crucial to avoid potential complications or delays in the transaction.

- Eligibility to file the MW506AE form extends to a broad category of sellers including individuals, fiduciaries, C corporations, S corporations, limited liability companies, and partnerships. However, distinctive filing requirements are specified for each transferor/seller, emphasizing a need for tailored advice based on the entity type involved in the property transaction.

- Comprehensive documentation is required to support the claim for a full or partial exemption. This necessitates a thorough compilation of relevant documents such as contracts of sale, settlement sheets, proof of residency status, and specific documents outlined for distinct exemption reasons. The meticulous gathering of necessary documentation reinforces the objective of substantiating the eligibility for the claimed exemption.

- The MW506AE form also mandates detailed information relating to the property sale including description, acquisition details, and calculation of the adjusted basis. This portion of the application not only serves the purpose of tax computation but aligns with the state's aim to maintain an accurate record of real estate transactions involving non-residents. Furthermore, it underscores the importance of detailed record-keeping by the seller for potential audit and verification purposes.

In summary, the Maryland MW506AE form is a crucial document for non-residents engaged in property sales within the state, designed to streamline the tax exemption process while ensuring compliance with Maryland’s tax requirements. A comprehensive understanding and adherence to its requirements can facilitate a smoother transaction process and potentially mitigate tax burdens associated with the sale of property for eligible individuals and entities.

Common PDF Templates

Ccs Redetermination - The acceptance letter checkbox clarifies the stage in the application process, ensuring candidates are ready to advance their education.

How Many Hours Can I Work at 16 - Facilitates lawful youth employment in Maryland, specifying the need for employer consent and parental or guardian signature.

How Much Back Child Support Is a Felony in Maryland - Ensures compliance with Maryland's electronic filing system in counties where this is mandated, for orders and protective measures.