Maryland Tax 766 PDF Template

The comprehensive nature of the Maryland Tax 766 form stands as a pivotal resource for retirees navigating both federal and Maryland state income tax withholdings from their pension allowances. This document, essential for those receiving pension payments from the Maryland State Retirement and Pension System, mandates the submission of a unified form that catulates previous withholding elections in favor of current preferences. The form intricately outlines the procedures for electing to withhold federal income taxes, detailing the requisite designation of withholding allowances or the opting for additional amounts to be withheld, contingent on the retiree's financial scope and anticipated tax liabilities. Furthermore, the form extends its utility to Maryland state residents by offering options regarding the withholding of state income tax, thereby emphasizing the agency’s prohibition against dispensing tax preparation advice, while advocating for consultation with tax professionals or the relevant tax authorities. This strategic approach underscores the significance of informed decision-making in mitigating potential tax liabilities and underscores the importance of recurrent consultation with the provided instructions and tax publications to ensure compliance and optimal tax strategy implementation.

Maryland Tax 766 Sample

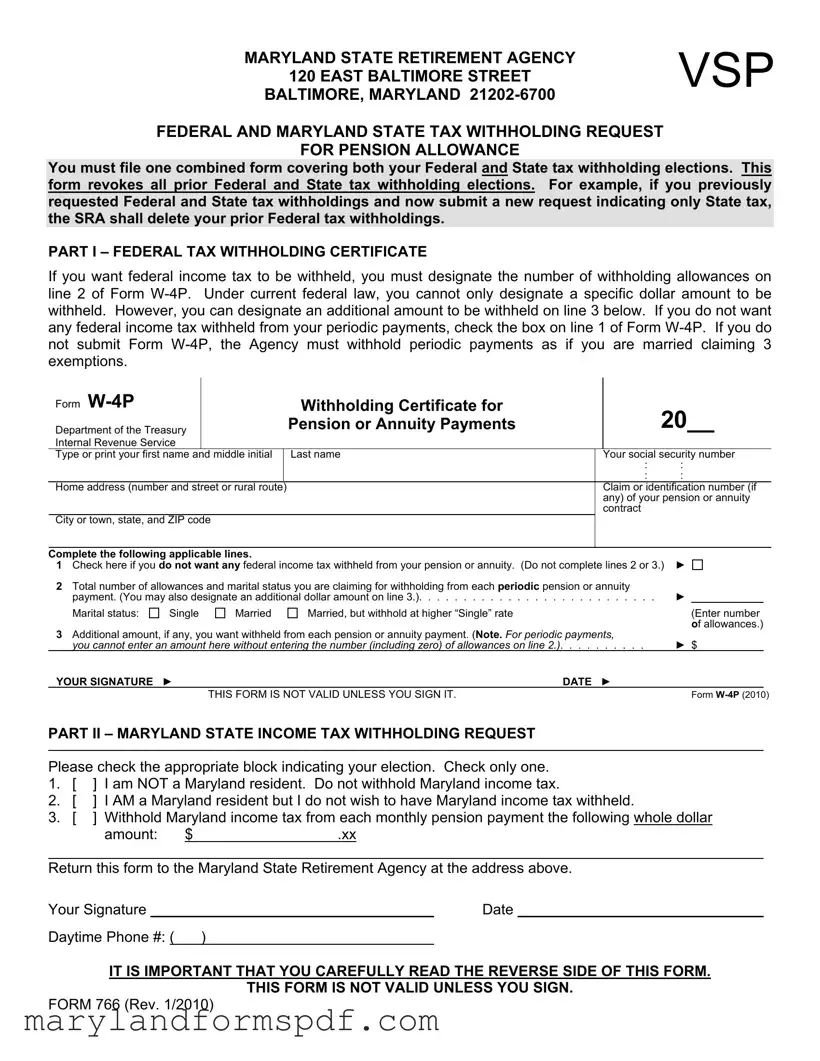

MARYLAND STATE RETIREMENT AGENCY |

VSP |

|

|

120 EAST BALTIMORE STREET |

|

BALTIMORE, MARYLAND |

|

FEDERAL AND MARYLAND STATE TAX WITHHOLDING REQUEST

FOR PENSION ALLOWANCE

You must file one combined form covering both your Federal and State tax withholding elections. This form revokes all prior Federal and State tax withholding elections. For example, if you previously requested Federal and State tax withholdings and now submit a new request indicating only State tax, the SRA shall delete your prior Federal tax withholdings.

PART I – FEDERAL TAX WITHHOLDING CERTIFICATE

If you want federal income tax to be withheld, you must designate the number of withholding allowances on line 2 of Form

Form |

|

|

|

Withholding Certificate for |

|

20__ |

|

||

Department of the Treasury |

|

|

Pension or Annuity Payments |

|

|

||||

|

|

|

|

|

|

|

|

||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

Type or print your first name and middle initial |

|

Last name |

|

Your social security number |

|||||

|

|

|

|

|

: |

: |

|

|

|

|

|

|

|

|

: |

: |

|

|

|

Home address (number and street or rural route) |

|

|

Claim or identification number (if |

||||||

|

|

|

|

|

|

any) of your pension or annuity |

|||

|

|

|

|

|

|

contract |

|

|

|

City or town, state, and ZIP code |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|||

Complete the following applicable lines. |

|

|

|

► |

|||||

1 Check here if you do not want any federal income tax withheld from your pension or annuity. (Do not complete lines 2 or 3.) |

|||||||||

2 Total number of allowances and marital status you are claiming for withholding from each periodic pension or annuity |

► |

|

|

||||||

payment. (You may also designate an additional dollar amount on line 3.) |

|||||||||

Marital status: |

Single |

Married |

Married, but withhold at higher “Single” rate |

|

|

(Enter number |

|||

|

|

|

|

|

|

|

|

of allowances.) |

|

3 Additional amount, if any, you want withheld from each pension or annuity payment. (Note. For periodic payments, |

► $ |

||||||||

you cannot enter an amount here without entering the number (including zero) of allowances on line 2.). . . . |

. . . . . . |

||||||||

YOUR SIGNATURE |

► |

|

|

DATE |

► |

|

|

|

|

|

|

THIS FORM IS NOT VALID UNLESS YOU SIGN IT. |

|

|

|

Form |

|||

PART II – MARYLAND STATE INCOME TAX WITHHOLDING REQUEST

Please check the appropriate block indicating your election. Check only one.

1.[ ] I am NOT a Maryland resident. Do not withhold Maryland income tax.

2.[ ] I AM a Maryland resident but I do not wish to have Maryland income tax withheld.

3.[ ] Withhold Maryland income tax from each monthly pension payment the following whole dollar

amount: |

$ |

.xx |

Return this form to the Maryland State Retirement Agency at the address above.

Your Signature |

|

|

Date |

|

Daytime Phone #: ( |

) |

|

||

|

|

|

|

|

IT IS IMPORTANT THAT YOU CAREFULLY READ THE REVERSE SIDE OF THIS FORM.

THIS FORM IS NOT VALID UNLESS YOU SIGN.

FORM 766 (Rev. 1/2010)

2

Part I

FEDERAL INCOME TAX WITHHOLDING

The monthly retirement payments you receive from the Maryland State Retirement and Pension System may be subject to Federal income tax withholding. For further information, please refer to Internal Revenue Service Publication 575 regarding the taxability of pension and annuity income.

As a retiree, the following Federal income tax withholding alternatives are available to you:

1.You may elect not to have Federal income tax deducted from your monthly retirement payment, or

2.You may claim a certain number of exemptions and have the Maryland State Retirement and Pension System deduct the appropriate amount, if any, in accordance with the Federal income tax tables and you may designate an additional specific whole dollar amount to be withheld from your monthly retirement payment.

If you elect not to have Federal withholding apply to your monthly retirement payments, or if you do not have enough Federal income tax withheld, you may be responsible for payment of estimated tax. You may incur penalties under the Internal Revenue Service estimated tax rules if your withholding and estimated tax payment are not sufficient. New retirees, especially, should see IRS Publication 505.

Part II

MARYLAND STATE INCOME TAX WITHHOLDING

The monthly retirement payments you receive from the Maryland State Retirement and Pension System may be subject to Maryland income tax withholding.

As a retiree and a Maryland resident, the following Maryland income tax withholding alternatives are available to you:

1.You may elect not to have Maryland income tax deducted from your monthly retirement payment, or

2.You may designate a specific whole dollar amount to be withheld from your monthly retirement payment.

If you elect not to have Maryland withholding apply to your monthly retirement payments, or if you do not have enough Maryland income tax withheld, you may be responsible for payment of estimated tax.

An election of any one of the alternatives will remain in effect until you revoke it. You may revoke or change your election at any time by filing a new Federal and Maryland State Tax Withholding Request.

The Maryland State Retirement Agency can not assist you in the preparation of tax returns. Please contact the Internal Revenue Service at

To receive additional copies of the Federal and Maryland State Tax Withholding Request form, or for other information concerning your retirement benefits, call

SEE REVERSE SIDE FOR FEDERAL AND MARYLAND STATE TAX WITHHOLDING REQUEST

FORM 766 (Rev. 1/2010)

Additional Instructions:

Section references are to the Internal Revenue Code. Agency refers to the Maryland State Retirement Agency.

When should I complete the form? Complete Form

Other income. If you have a large amount of income from other sources not subject to withholding (such as interest, dividends, or capital gains), consider making estimated tax payments using Form

Withholding From Pensions and Annuities

Generally, federal income tax withholding applies to the taxable part of payments made from pension,

Because your tax situation may change from year to year, you may want to refigure your withholding each year. You can change the amount to be withheld by using lines 2 and 3 of Form

Choosing not to have income tax withheld. You (or in the event of death, your beneficiary or estate) can choose not to have federal income tax withheld from your payments by using line 1 of Form

Caution. There are penalties for not paying enough federal income tax during the year, either through withholding or estimated tax payments. New retirees, especially, should see Pub. 505. It explains your estimated tax requirements and describes penalties in detail. You may be able to avoid quarterly estimated tax payments by having enough tax withheld from your pension or annuity using Form

Periodic payments. Withholding from periodic payments of a pension or annuity is figured in the same manner as withholding from wages. Periodic payments are made in installments at regular intervals over a period of more than 1 year. They may be paid annually, quarterly, monthly, etc.

If you want federal income tax to be withheld, you must designate the number of withholding allowances on line 2 of Form

3

designate an additional amount to be withheld on line 3. If you do not want any federal income tax withheld from your periodic payments, check the box on line 1 of Form

Caution. If you do not submit Form

If you submit a Form

taxpayer identification number (TIN), the payer must withhold as if you are single claiming zero withholding allowances even if you choose not to have federal income tax withheld.

There are some kinds of periodic payments for which you cannot use Form

For periodic payments, your Form

Changing Your “No Withholding” Choice

Periodic Payments. If you previously chose not to have federal income tax withheld and you now want withholding, complete another Form

Payments to Foreign Persons and

Payments Outside the United States

Unless you are a nonresident alien, withholding (in the manner described above) is required on any periodic or nonperiodic payments that are delivered to you outside the United States or its possessions. You cannot choose not to have federal income tax withheld on line 1 of Form

In the absence of a tax treaty exemption, nonresident aliens, nonresident alien beneficiaries, and foreign estates generally are subject to a 30% federal withholding tax under section 1441 on the taxable portion of a periodic or nonperiodic pension or annuity payment that is from U.S. sources. However, most tax treaties provide that private pensions and annuities are exempt from withholding and tax. Also, payments from certain pension plans are exempt from withholding even if no tax treaty applies. See Pub.

Statement of Federal Income Tax Withheld From Your Pension or Annuity

By January 31 of next year, your payer will furnish a statement to you on Form

File Breakdown

| Fact Name | Description |

|---|---|

| Purpose | The Maryland Tax 766 form is used for requesting both Federal and Maryland State tax withholdings from pension allowances. |

| Revocation of Prior Elections | Submitting a new Maryland Tax 766 form will override all previous Federal and State tax withholding elections. |

| Federal Tax Withholding Options | Retirees can either elect not to have Federal income tax withheld or specify the number of allowances for withholding. An additional whole dollar amount can also be designated for withholding. |

| Maryland State Tax Withholding Choices | Maryland residents can choose not to have State income tax withheld or specify a whole dollar amount to be withheld from their monthly pension payment. |

Steps to Filling Out Maryland Tax 766

Filling out the Maryland Tax 766 form is a crucial step for pensioners to ensure the correct amount of federal and state taxes is withheld from their pension allowances. It’s a process that requires careful attention to detail. Below, you will find straightforward steps to guide you through completing this form correctly.

- Begin by reading the instructions carefully on the form to understand what's needed for both the federal and state tax withholding parts.

- Under Part I – FEDERAL TAX WITHHOLDING, locate Form W-4P. If you choose not to have federal income tax withheld from your pension, tick the box on line 1. If you prefer to have tax withheld, complete line 2 by indicating your total number of allowances and marital status. Next, if you’d like an additional specific amount to be withheld from each payment, mention this dollar amount on line 3.

- In the section provided, type or print your name, social security number, home address, and any claim or identification number related to your pension or annuity contract, along with your city, state, and ZIP code.

- Ensure you sign and date Form W-4P. Remember, your signature is essential for the form to be valid.

- Proceed to Part II – MARYLAND STATE INCOME TAX WITHHOLDING REQUEST. Here, you will indicate your residency status and whether you wish to have Maryland income tax withheld from your monthly pension payment.

- If you decide against having Maryland income tax withheld, tick the appropriate box to indicate this choice. Conversely, if you choose to have state tax withheld, specify the whole dollar amount to be deducted from each payment.

- Again, ensure you sign and date the form, including your daytime phone number. Like the federal section, this part won't be considered valid without your signature.

- Double-check all entered information to ensure accuracy and completeness.

- Finally, return the completed form to the Maryland State Retirement Agency at the address provided at the top of the form.

Upon submitting this form, you have effectively communicated your preferences for both federal and state tax withholdings regarding your pension allowance. It’s important to note that these elections will remain in effect until you decide to change or revoke them by submitting a new form. Remember, if at any point you are unsure about how to fill out this form or if your circumstances change, seeking advice from a tax professional or contacting the appropriate agencies directly can provide clarification and assist you in making informed decisions about your tax withholding preferences.

More About Maryland Tax 766

What is the Form 766 used for in Maryland?

Form 766 is a document that enables retirees of the Maryland State Retirement and Pension System to request how they would like their federal and Maryland state income taxes to be withheld from their pension allowance. It offers individuals the choice to determine the amount of tax withheld from their pension or to not have withholding at all. This form essentially combines the requests for both federal and state tax withholdings into one document, simplifying the process for retirees.

How can you change your tax withholding preferences using Form 766?

To change your tax withholding preferences for your pension, you must submit a new Form 766 to the Maryland State Retirement Agency. This form allows you to specify your desired federal and state income tax withholdings. Whether you're adjusting the number of allowances, changing the additional amount to be withheld, or choosing not to have any taxes withheld, submitting this updated form will revoke any previous withholding elections and implement your new preferences.

Are there penalties for not having enough tax withheld?

Yes, there can be penalties for not having enough federal or state income tax withheld from your pension payments. If you do not have sufficient tax withheld, or if you do not make estimated tax payments as needed, you might be liable for underpayment penalties under the Internal Revenue Service's estimated tax rules. Individuals, particularly new retirees, are encouraged to review their withholding choices and adjust them as necessary to avoid such penalties.

Who should retirees contact for assistance with their tax returns or withholding decisions?

While the Maryland State Retirement Agency cannot assist with the preparation of tax returns or provide tax advice, retirees looking for assistance have several resources available. For federal tax issues, contacting the Internal Revenue Service (IRS) at 1-800-829-1040 is recommended. For state tax inquiries, the Comptroller’s Taxpayer Service Information Line at 410-260-7980 (in Central Maryland) or 1-800-638-2937 is a helpful resource. Additionally, consulting a tax consultant for personal advice and guidance is also an option.

When should a retiree submit the Form 766 to change their withholding preference?

Retirees are advised to submit the Form 766 to the Maryland State Retirement Agency as soon as they decide to change their tax withholding preferences. This proactive approach ensures that the desired adjustments to federal and state income tax withholdings will be reflected in their pension payments promptly. To minimize discrepancies in tax withholding and to address any tax-related changes in their life situations, submitting this form timely is crucial.

Common mistakes

When completing the Maryland Tax 766 form, individuals often make mistakes that can lead to delays or errors in their tax withholding. To ensure accuracy and compliance, here are nine common mistakes to avoid:

- Failing to revoke prior Federal and State tax withholding elections by not submitting a new form when changes are desired. This can result in incorrect withholding amounts.

- Omitting the number of allowances on line 2 of Form W-4P for Federal tax, which is essential if tax withholding is wanted. This oversight can lead to the default withholding status, potentially leading to under or over-withholding.

- Not checking the box on line 1 of Form W-4P if they do not want any federal income tax withheld. This mistake can result in unwanted tax withholdings from pension payments.

- Neglecting to designate an additional dollar amount for withholding on line 3 when adjustments to the standard withholding are necessary for meeting tax obligations.

- Forgetting to sign the Form 766, rendering it invalid and causing delays in processing the withholding request. The signature is a critical component that verifies the taxpayer's intent and authorization.

In addition to these errors, here are four more mistakes specifically related to the Maryland State Income Tax Withholding Request:

- Selecting the incorrect status for Maryland residency or tax withholding, which can lead to improper withholding amounts or failure to withhold taxes.

- Entering an incorrect whole dollar amount for Maryland income tax withholding, potentially resulting in underpayment or overpayment of state taxes.

- Overlooking the importance of reading the reverse side of the Form 766, which contains vital information on withholding options, rights, and responsibilities.

- Not updating the form upon changes in residency status or financial situation, which may necessitate different withholding amounts to avoid tax surprises.

To prevent these common errors, careful review, and accurate completion of the Maryland Tax 766 form are crucial. Additionally, consulting the form’s instructions or seeking advice from a tax professional can provide further clarity and ensure that both Federal and State taxes are correctly withheld according to the retiree's current needs and preferences.

Documents used along the form

When individuals retire, navigating through the various forms and documents necessary for managing their retirement income and taxes can be a complex task. The Maryland Tax 766 form, dedicated to Federal and Maryland State Tax Withholding Request for Pension Allowance, serves as a critical tool for retirees to specify their preferences for how much tax should be withheld from their pension payments. However, this form does not exist in isolation. Several other documents often accompany the Maryland Tax 766 form, each playing a unique role in ensuring retirees' financial and tax affairs are orderly and compliant with both federal and state requirements.

- Form W-4P: Withholding Certificate for Pension or Annuity Payments, enabling recipients to request the amount of federal income tax to be withheld from their pension or annuity payments.

- Form 1040-ES: Estimated Tax for Individuals, used by taxpayers to calculate and pay estimated quarterly taxes. This is especially relevant if the retiree has significant non-withholding income.

- Form 1099-R: Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, showcasing the amount of distributions and taxes withheld during the year.

- Form 1042-S: Foreign Person's U.S. Source Income Subject to Withholding, applicable for nonresident aliens receiving retirement distributions from U.S. sources, detailing income and withheld taxes.

- Form W-8BEN: Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding, used by foreign individuals to claim tax treaty benefits and reduce withholding tax.

- IRS Publication 575: Pension and Annuity Income, providing comprehensive information on how pension and annuity income is taxed federally.

- IRS Publication 505: Tax Withholding and Estimated Tax, offering guidance on adjusting withholding on pensions and how to handle estimated taxes.

- IRS Publication 919: How Do I Adjust My Tax Withholding, assisting individuals in determining the correct amount of tax withholding to avoid unexpected tax bills or penalties.

Together, these documents form a framework to support retirees in managing their tax obligations effectively. Understanding and correctly utilizing these forms and publications can lead to a smoother transition into retirement, ensuring that retirees can enjoy their golden years without undue stress over tax-related issues. It's always recommended for retirees or their advisors to consult with tax professionals or financial advisors to tailor their tax and income strategies to their specific situations.

Similar forms

The Maryland Tax 766 form is primarily used to manage tax withholdings for pension payments and is designed to handle both federal and state tax elections in one document. This particular approach aligns it with several other tax documents, albeit those may serve broader purposes or specific niches. Understanding these similarities helps in grasping the form's functionality and how it integrates into wider tax management practices for retirees.

First, it shares a close resemblance with the Form W-4P, or the Withholding Certificate for Pension or Annuity Payments. Just like the Maryland Tax 766 form, Form W-4P is used by individuals receiving pension, annuities, or other retirement payments to determine the amount of federal income tax to be withheld. While the Maryland Tax 766 form extends this functionality to include state tax elections for Maryland specifically, Form W-4P exclusively addresses federal tax withholdings. Both forms allow retirees to tailor their tax withholdings to their personal financial situations, potentially averting the need to pay estimated taxes.

Similarly, the Maryland Tax 766 form has elements in common with the Form 1040-ES, the Estimated Tax for Individuals form. Although Form 1040-ES is not used exclusively by retirees and is designed for a wide array of taxpayers to estimate and pay taxes on income not subject to withholding, the underlying principle is comparable. Both the 1040-ES and the Maryland Tax 766 form play crucial roles in tax planning and management, particularly for individuals with complex tax situations or multiple income sources. The key difference lies in the proactive nature of estimating and paying taxes with Form 1040-ES versus adjusting withholdings directly from pension payments with the Maryland Tax 766.

In essence, while the Maryland Tax 766 form is distinctly designed for Maryland retirees to manage their state and federal pension withholdings, its function parallels that of both Form W-4P and Form 1040-ES in facilitating individualized tax management. By allowing adjustments to withholdings or making estimated payments, these forms collectively support taxpayers in achieving a favorable tax outcome, avoiding underpayment penalties, and ensuring compliance with tax obligations.

Dos and Don'ts

When filling out the Maryland Tax Form 766, it’s crucial to approach the task with care and attention to ensure accuracy and compliance with both federal and state tax laws. Here are some key dos and don’ts to keep in mind:

Do:- Review the instructions on both sides of the form carefully before you start filling it out. They provide important details about how to complete the form correctly.

- Decide on your federal and state tax withholding needs before you fill out the form. This decision will impact how much tax is withheld from your pension allowance.

- Use accurate personal information, including your social security number and home address. Mistakes can lead to processing delays or issues with your tax withholding.

- Sign and date the form before submission. An unsigned form is not valid and will not be processed.

- Consult with a tax advisor if you're unsure about how to complete the form or about your specific tax situation. Making informed choices can help avoid unexpected tax liabilities.

- Leave sections blank that apply to you. If you're requesting federal tax withholding, for example, you must complete the relevant sections of the form.

- Ignore marital status and allowances when filling out your withholding preferences. These factors play a critical role in determining the amount of tax withheld.

- Enter incorrect numbers of allowances or an incorrect additional amount to be withheld. Errors can lead to too much or too little tax being withheld from your pension.

- Forget to revoke previous elections if you're making new withholding requests. Submitting this form will replace all prior withholding elections.

- Disregard the need to reevaluate your tax situation annually. Your financial situation can change, and it may be beneficial to adjust your tax withholding accordingly.

Misconceptions

Understanding the Maryland Tax Form 766 can be tricky, with various misconceptions floating around that can confuse retirees or those new to using the form. Let's clear up some of these misunderstandings:

Only Maryland residents need to fill out the Form 766. This is incorrect. Even if you're not a Maryland resident, you need to indicate your non-residency status on the form to ensure Maryland state income tax is not withheld from your retirement pension.

You must choose between federal or state tax withholding on Form 766. This is a misconception. The Form 766 allows you to request both federal and Maryland state tax withholdings simultaneously. Updating your preferences on this form affects both federal and state withholdings accordingly.

If you don't fill out Form 766, no taxes will be withheld from your pension. This is not true. If you do not submit Form W-4P included in Form 766, the default withholding status is as if you are married, claiming three allowances. This means taxes will indeed be withheld from your pension unless you specifically opt out.

You can only change your withholding once a year. Many believe that once you submit Form 766, your decision is locked in for the year. However, you have the flexibility to update your withholding preferences at any time by submitting a new Form 766.

Form 766 is only for those receiving monthly payments. While it's true that the form primarily pertains to monthly pension payments, it's essential for all retirees receiving pension distributions to consider their tax withholding preferences and use Form 766 to make any necessary requests.

It's crucial for retirees to have a clear understanding of Form 766 to make informed decisions regarding their tax withholdings. Misconceptions can lead to unexpected tax liabilities or withholdings that don't align with your financial planning. When in doubt, consult with a tax advisor or the relevant authorities to ensure your withholdings are set up according to your personal needs and circumstances.

Key takeaways

Filling out the Maryland Tax Form 766 is critical for retirees looking to manage their federal and state income tax withholding from their pension allowance efficiently. Here are four key takeaways to ensure you're on the right track:

- It's important to specify your tax withholding preferences for both federal and Maryland state taxes on one combined form. This action will override any prior tax withholding elections you've made.

- For federal tax withholding, you cannot specify a dollar amount but can indicate your marital status and the number of allowances on Form W-4P, allowing for an additional amount to be specified if desired.

- If you're a Maryland resident, you have the option to either have Maryland state income tax withheld from your monthly pension by specifying a dollar amount or opt not to have any state tax withheld. Your decision should be clearly indicated in the Maryland State Income Tax Withholding Request section.

- Changes to your withholding preferences can be made anytime by submitting a new Maryland Tax Form 766. This flexibility allows you to adjust your withholdings as your financial situation changes or to correct any previous election errors.

Understanding these aspects ensures that retirees can better manage their tax liabilities and avoid potential underpayment penalties. It's also advisable to consult tax publications or a tax consultant for personalized advice, given the complexity of tax laws and individual financial situations.

Common PDF Templates

Sales and Use Tax Md - A crucial reference for Maryland businesses to navigate the end-of-business sales and use tax formalities efficiently.

Md Tax Forms - A detailed worksheet included to help taxpayers accurately forecast their 2012 income and tax obligations.